Introduction

Home Healthcare Statistics: Home healthcare has become essential to the healthcare system, highlighting a notable shift towards patient-focused and cost-efficient care delivery models. This sector includes diverse medical and support services provided directly in patients’ homes to enhance health outcomes while ensuring greater comfort and convenience.

Key drivers such as the aging global population, rising incidence of chronic illnesses, and advancements in remote patient monitoring technologies have significantly fueled the expansion of home healthcare demand worldwide. Examining relevant statistics in this field offers crucial insights into market size, demographic changes, service usage, and spending patterns.

Information is vital for healthcare providers, policymakers, and investors seeking to make well-informed decisions. This introduction paves the way for an in-depth analysis of current data and emerging trends that define the evolving home healthcare market.

Editor’s Choice

- Home healthcare continues to play a pivotal role in the U.S. healthcare system by delivering essential medical care directly to patients in their own homes.

- As of 2022, the nation supported around 33,200 home healthcare agencies, backed by a robust workforce of over 1.5 million professionals, including registered nurses, home health aides, and therapists.

- Annually, nearly 12 million individuals across the United States rely on home healthcare services, with old aged 65 and above comprising the vast majority, approximately 86% of this patient population.

- The primary health issues necessitating these services include cardiovascular diseases, diabetes, chronic obstructive pulmonary disease (COPD), and Alzheimer’s disease, all of which require ongoing, specialized care.

- Medicare is the principal financier of home healthcare, covering nearly 42% of all home visits nationwide.

- Research has demonstrated that effective home healthcare interventions can lower hospital readmission rates by up to 25% for patients suffering from chronic conditions such as heart failure and pneumonia. This reduction improves patient well-being, helps alleviate the burden on hospital systems, and reduces healthcare costs overall.

(Source: Bureau of Labor Statistics, CMS, Home Health Care News, NAHC, JAMA, Kaiser Family Foundation, Market.us)

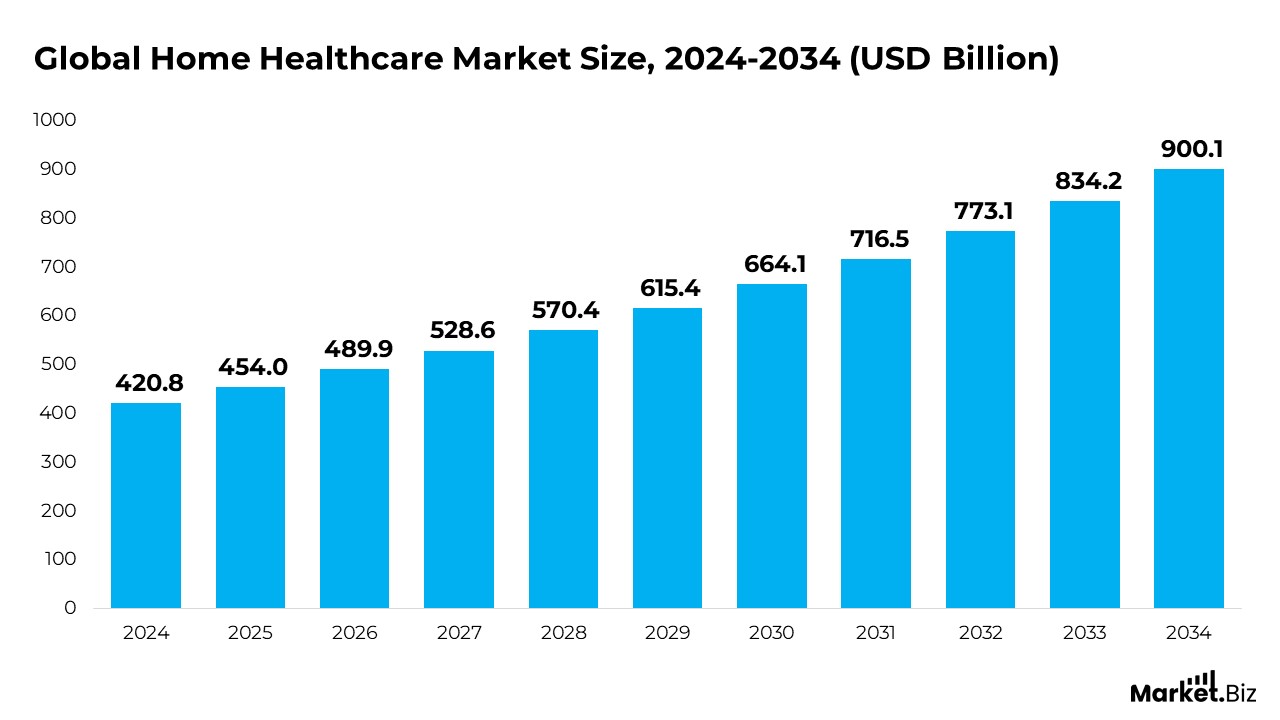

Home Healthcare Market Size

- As per Market.us, the global market for home healthcare is anticipated to expand from $489.9 billion in 2025 to $773.1 billion by 2032, reflecting a compound annual growth rate (CAGR) of 7.9% from 2024 to 2034.

- The home healthcare market is experiencing substantial growth, driven by heightened awareness of chronic diseases such as diabetes, a rapidly expanding older population, and the increasing incorporation of artificial intelligence technologies into home-based care solutions.

- In 2023, the services segment emerged as the dominant contributor, capturing a market share of 57.4%. This leadership is attributed to the growing demand for customized care in patients’ homes. As the number of older individuals rises, there is a clear preference for receiving care at home, especially for managing chronic illnesses and post-surgical rehabilitation. Consequently, services such as skilled nursing, physical therapy, and occupational therapy are witnessing heightened demand.

- Among medical conditions, cardiovascular disorders and hypertension commanded a significant 38.6% market share. The global rise in chronic diseases like hypertension, heart disease, and stroke i

- s fueling patient interest in home-based monitoring and care solutions to manage these conditions better.

- Regionally, North America led the market in 2023, holding the largest revenue share of 40.2%. This dominance is supported by the widespread adoption of remote patient monitoring technologies and a growing preference for home care services among the population.

- Meanwhile, the Asia Pacific region is projected to register the fastest growth rate during the forecast period. This expansion is propelled by an aging demographic and improved access to healthcare services. Notably, China’s senior population, those aged 60 and above, reached approximately 297 million as of January 2024, representing 21.1% of the total population, with forecasts estimating this number will surpass 500 million by 2050.

(Source: Market.us)

General Statistics of Home Healthcare

The demographic landscape is undergoing a profound shift as populations around the world age rapidly, leading to increased demand for home healthcare services. This evolution is particularly significant in low- and middle-income countries where most older adults will reside by mid-century.

Concurrently, the United States is witnessing considerable growth in home healthcare spending and workforce, driven by patient preferences and advancements in care delivery models such as telehealth.

Developments

- By 2050, an estimated 80% of the global older population will live in low- and middle-income nations, reflecting a major demographic transition.

- In 2020, individuals aged 60 and above surpassed the number of children aged five or younger worldwide, marking a demographic milestone.

- Between 2015 and 2050, the share of people aged 60 years or older globally is expected to nearly double, rising from 12% to 22% of the total population.

- By 2020, one out of every six people globally was 60 or above, underscoring the expanding senior demographic.

- The worldwide population of old aged 60+ is projected to grow from 1 billion in 2020 to 1.4 billion shortly.

- Looking ahead to 2050, the number of older adults globally will double again, reaching approximately 2.1 billion.

- In the United States, spending on home healthcare reached roughly US$113.8 billion in 2022, highlighting its growing economic significance.

Moreover

- Employment for home healthcare and personal care aides in the U.S. is projected to increase by 34% between 2019 and 2029, a rate considerably faster than the overall job market average, according to the U.S. Bureau of Labor Statistics.

- Around 4.5 million individuals in the U.S. annually receive home healthcare services, demonstrating the sector’s broad reach.

- Nearly 90% of Americans aged 65 and older prefer to remain in their homes as they age rather than transition to nursing homes or assisted living facilities.

- Home healthcare has been shown to reduce hospital readmission rates by 25% compared to conventional care settings, illustrating its effectiveness in managing patient health.

- The COVID-19 pandemic accelerated telehealth adoption in home care, with telehealth visits surging by 154% in March 2020 compared to the previous year.

- Approximately 82% of home healthcare agencies operate for-profit, reflecting the market’s business-driven nature.

- In 2022, nearly 4.9 million patients began and completed home healthcare episodes, indicating the sector’s dynamic patient turnover.

(Source: World Health Organization, Centers for Disease Control and Prevention, McKinsey, Market.us)

Demographic Profile and Service Usage Patterns in Home Healthcare

- Women made up approximately 65% of the individuals receiving home healthcare support.

- A significant portion, 71% of patients, were 65 or older, reflecting the aging population’s reliance on in-home medical care.

- Nearly 58% of home healthcare recipients were single, widowed, or otherwise unmarried.

- Most patients, around 94%, resided in either private homes or shared living spaces rather than institutional settings.

- Family support was common, with 63% of patients living alongside relatives.

- 75% of home healthcare patients utilized skilled nursing and medical care services, making it the most commonly used service type.

- Personal care services, such as assistance with bathing or dressing, were accessed by 44% of individuals.

- Treatments, including physical or speech therapy, were used by about 37% of patients.

- Additional services such as medication administration, counseling, occupational therapy, continuous care, and social work were less commonly employed but still contributed to holistic patient management.

(Source: National Institute of Health, Market.us)

Understanding Patient Preferences in Home Healthcare

Patient preferences are essential in guiding the delivery of home healthcare services, emphasizing the need for autonomy, comfort, and personalized care. Key insights include:

- Over 90% of older adults prefer to age in their homes instead of moving to institutional care settings.

- Approximately 52% of home care recipients value having a consistent caregiver for each visit to build trust and continuity.

- Patients choose home care mainly to maintain independence and control their daily routines.

- About 85% of older people receiving home care feel safer and more comfortable living in their residences.

- Most patients favor receiving medical treatments at home rather than in hospitals or nursing facilities whenever possible.

- Individuals receiving home healthcare report higher satisfaction with their overall quality of life than those in institutional care settings.

- More than 80% of family caregivers confirm that home care providers respect and incorporate their loved one’s daily routines and preferences into care plans.

(Source: Home Care Pulse, National Council on Aging, Home Instead Senior Care, Journal of General Internal Medicine, American Academy of Home Care Medicine, Family Caregiver Alliance, American Association of Retired Persons)

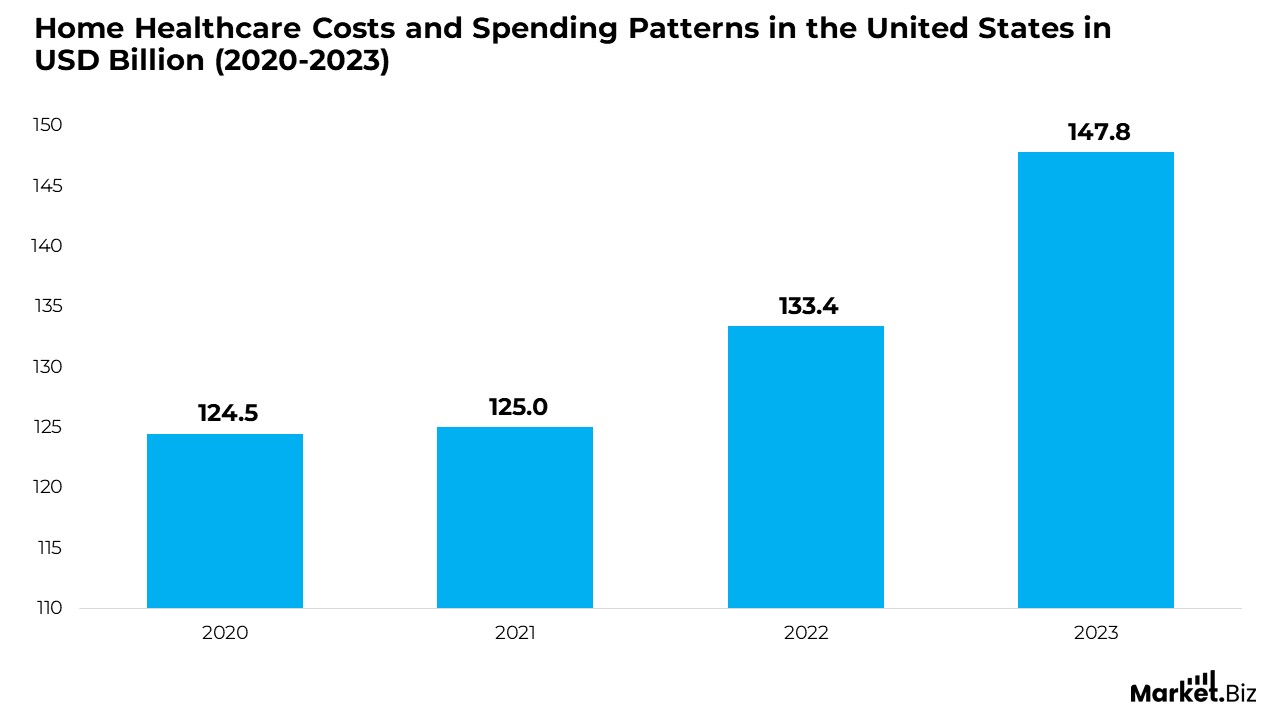

Home Healthcare Costs and Spending Patterns in the United States

Frequently Reported Admission Diagnoses in Home Healthcare Patients

- Heart disease is the leading admission diagnosis, affecting 11% of individuals entering home healthcare programs.

- Diabetes accounts for 8% of initial diagnoses among home healthcare patients.

- Cerebrovascular conditions, including stroke-related disorders, represent 7% of admissions.

- Chronic obstructive pulmonary disease (COPD) is identified in 5% of patients upon admission.

- Cancer diagnoses (malignant neoplasms) also comprise 5% of home healthcare admissions.

- Congestive heart failure is the admission diagnosis for 4% of patients receiving home care.

- Osteoarthritis and related musculoskeletal disorders account for 4% of admissions.

- Fractures, often due to falls or injury, are reported as the primary diagnosis in 4% of cases.

- Hypertension is the admission diagnosis for 3% of home healthcare patients.

(Source: National Institute of Health, Market.us)

Technology Trends and Adoption in Home Healthcare

Advancements in technology have profoundly transformed the home healthcare landscape, enhancing patient care delivery, improving outcomes, and driving operational efficiencies. These innovations, from telehealth to artificial intelligence, reshape how care is accessed and managed outside traditional clinical settings.

Growth of Remote Patient Monitoring (RPM)

- Approximately 23.4 million patients in the U.S. engaged with remote patient monitoring tools and services in 2022, with projections estimating this figure will rise to 30 million by 2024.

- According to research published in the Journal of Medical Internet Research, RPM usage within home healthcare rose by 44% between 2015 and 2022.

- A survey from HIMSS revealed that 76% of healthcare organizations across the U.S. have implemented some form of remote patient monitoring.

- Evidence shows that RPM can reduce hospital readmissions by 50% for heart failure patients and lower annual healthcare costs by over $5,000 per patient managing chronic conditions.

Telehealth Expansion

- Telehealth claim lines in the United States surged by 47% between 2019 and 2022, reflecting rapid adoption and growing patient acceptance.

- Medicare telehealth visits escalated dramatically from roughly 14,000 weekly pre-pandemic to over 1.7 million per week by April 2020.

Electronic Health Records (EHR) Integration

- The adoption of electronic health record systems by home

- healthcare agencies nearly doubled from 42.6% in 2011 to 85.5% in 2021.

- Nearly 89% of home health and hospice providers report that EHR implementation has significantly improved operational efficiency.

Mobile Health Applications (mHealth)

- As of 2021, the global availability of mobile health apps reached approximately 340,000.

- Around 75% of patients believe that mobile health applications aid in more effective management of their healthcare needs, with 76% specifically using these apps to manage chronic diseases.

Artificial Intelligence (AI) Applications in Home Care

- AI algorithms have demonstrated an 84% sensitivity in predicting hospitalizations for chronic obstructive pulmonary disease patients, with a specificity of 64%.

- Industry analyses estimate that AI-driven healthcare analytics could cut hospital stays by 20% and reduce readmission rates by up to 25%.

- In dermatology, AI outperformed human specialists by achieving a 95% accuracy rate in skin cancer detection compared to 86.6% accuracy among dermatologists.

(Source: National Institute of Health, JMIR, Accenture, Market.us)

Key Challenges Facing the Home Care Sector

- A critical shortage of home care workers continues to pose a major obstacle to the industry’s growth and service delivery.

- The demand for caregiving is set to surge, with the population of older adults requiring assistance expected to double by 2040, while the supply of available caregivers is projected to grow by a mere 1%.

- Home care providers must contend with increasingly complex regulations and intricate reimbursement frameworks, adding layers of administrative burden.

- Additionally, traditional home care agencies face mounting competition from innovative technology-driven care solutions that are reshaping the market landscape.

(Source: Parx)

Recent Developments

Funding Activities and Strategic Investments

- HomeHealth secured $50 million in Series A financing, led by Healthcare Investment Group, to broaden its home healthcare service portfolio and upgrade technology infrastructure, aiming to boost patient enrollment by 50% within the coming year.

- CarePlus raised $30 million in seed capital from Tech Investors ABC to innovate home healthcare solutions and build strategic partnerships with medical organizations, targeting a 40% revenue increase in the next fiscal period.

Influence of Aging Demographics

- The growing older population continues to fuel demand for home healthcare, with forecasts predicting a substantial rise in older needing assistance with everyday tasks and medical support.

- Agencies expanded specialized services tailored to geriatric needs, including dementia management, palliative care, and recovery programs post-hospital discharge.

Adoption of Telehealth Solutions

- Home healthcare providers incorporated telehealth capabilities into their service mix, enabling virtual patient consultations, remote health monitoring, and streamlined care coordination for homebound individuals.

- Telemedicine platforms enhanced their offerings by adding home healthcare consultations and follow-ups, improving accessibility for patients managing chronic diseases or facing mobility challenges.

Regulatory Enhancements and Support

- Policymakers introduced measures to strengthen home healthcare delivery, such as reimbursement adjustments, licensing reforms, and quality assurance programs focused on patient safety and service standards.

- Increased government funding was directed toward home and community-based care initiatives, including Medicaid HCBS waivers, to encourage aging in place and enhance community support frameworks.

Focus on Patient Experience and Outcomes

- Home healthcare providers utilized patient feedback and outcome metrics to evaluate service quality, adopting initiatives to enhance communication, care coordination, and continuity for patients and their caregivers.

Conclusion

Home healthcare has become a cornerstone of modern care delivery, offering patients the flexibility and comfort of receiving medical support in their homes. An aging population fuels its growing importance, the rising burden of chronic diseases, and the shift toward personalized, value-based care.

While the sector holds immense potential to improve health outcomes and reduce strain on hospital systems, it also faces persistent challenges, including workforce shortages, regulatory hurdles, and increasing competition from tech-enabled care models. Moving forward, the sustainability and effectiveness of home healthcare will depend on strategic investments in workforce development, innovation, and policy reforms that support accessible and high-quality care at home.

FAQ’s

Home healthcare encompasses a variety of medical and supportive services delivered directly to a patient’s residence. These services range from skilled nursing and therapy sessions to assistance with daily activities aimed at helping individuals recover from health conditions or manage ongoing illnesses in a familiar setting.

This form of care is particularly beneficial for older adults, individuals living with chronic conditions, patients recovering from surgeries, and those in need of extended rehabilitation outside a hospital environment.

The rising need for affordable and patient-focused care, combined with a growing older population and a surge in chronic diseases, has elevated the role of home healthcare in modern medical systems.

The industry is grappling with several issues, including a limited supply of trained caregivers, evolving regulatory demands, reimbursement complexities, and increased pressure from tech-based care alternatives.

By providing consistent monitoring, early detection of complications, and comprehensive chronic disease management, home healthcare plays a key role in minimizing the need for hospital readmissions.

Digital tools such as remote monitoring systems, virtual care platforms, AI-powered applications, and electronic health records make home-based care more responsive, accurate, and tailored to individual needs.