Introduction

Telecom cloud statistics present a concise, data-focused view of how cloud computing is transforming the global telecommunications industry by enabling operators to shift from legacy, hardware-centric infrastructure to scalable, software-defined, and automated cloud environments.

These statistics track adoption across public, private, and hybrid cloud models in network operations, IT systems, customer platforms, and emerging 5G and edge computing use cases, highlighting trends in workload migration, virtualization, and cloud spending.

They also illustrate how cloud adoption supports capabilities such as network function virtualization, cloud-native 5G cores, AI-driven network optimization, and real-time analytics, offering insight into operator investment priorities, modernization progress, and evolving competitive dynamics across regions.

Editor’s Choice

- Global investment in cloud computing continues to surge, with total spending expected to reach $679 billion in 2024, underscoring the cloud’s role in enterprise decision-making.

- The volume of digital information is expanding rapidly, with total global data projected to reach 200 zettabytes by 2025, intensifying reliance on cloud infrastructure.

- The cloud computing market is on a strong growth trajectory, with the overall market value forecast to reach $947.3 billion by 2026.

- Public cloud adoption is nearly universal, as 96% of organizations now use at least one public cloud service.

- Amazon Web Services maintains its leadership position in the public cloud market, holding a 32% share, ahead of other major providers.

- Private cloud environments remain widely used, with 84% of companies operating private cloud infrastructure alongside other deployment models.

- Cost control is the most significant challenge for cloud decision makers, with 82% citing cloud spend management as their primary concern.

- Security outcomes following cloud adoption are largely positive, as 94% of organizations report improved security after moving workloads to the cloud.

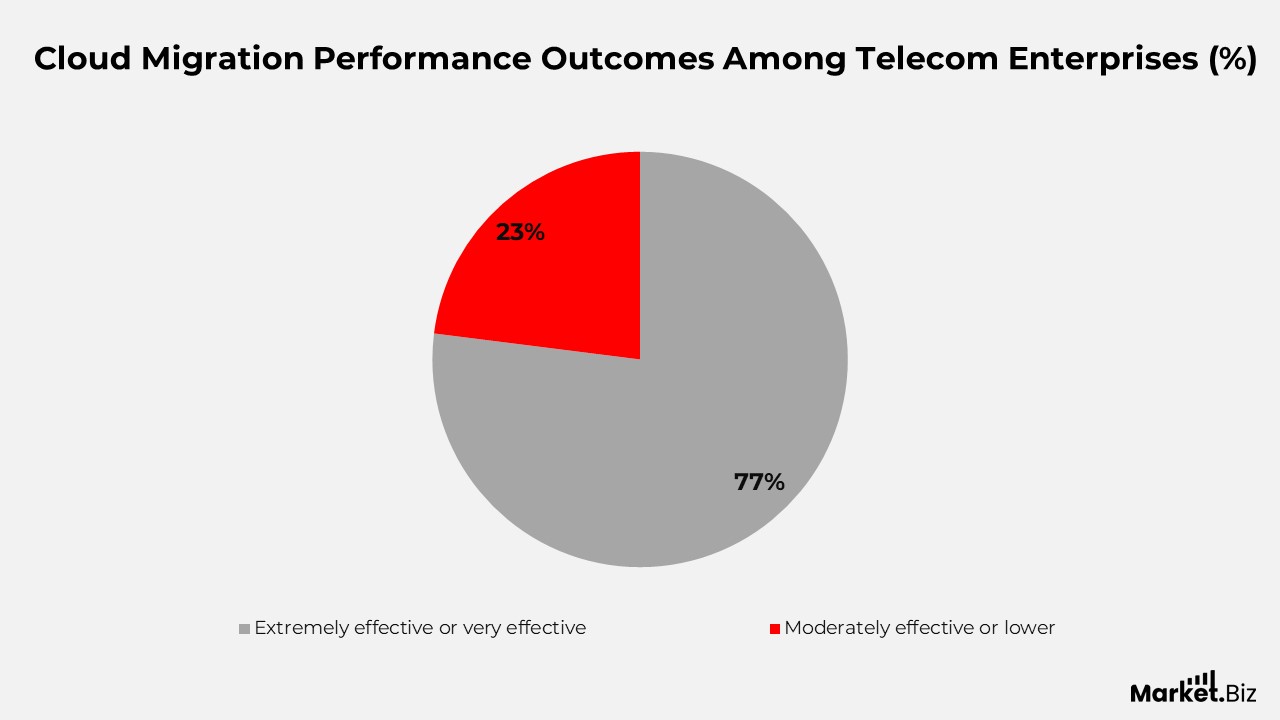

Cloud Migration Performance Outcomes Among Telecom Enterprises

- A strong majority of organizations report positive outcomes from cloud migration, with 77% rating their initiatives as extremely effective or very effective.

- Only 23% of respondents indicate moderate effectiveness or below, suggesting limited dissatisfaction with cloud migration results.

- The high effectiveness rating reflects alignment between cloud migration objectives and realized operational or business benefits.

(Sources: Infosys Knowledge Institute)

Primary Drivers of Cloud Adoption

- Business growth objectives strongly influence cloud adoption, with 17 points each allocated to enabling new revenue streams or products and replacing or modernizing legacy systems.

- Access to advanced technology and software development capabilities is a major motivator, accounting for 16 points in decision-making.

- Integration of business subsidiaries and acquisitions also plays a significant role, contributing 16 points toward cloud migration priorities.

- Industry-specific capabilities drive adoption decisions, with 13 points reflecting the need for sector-focused solutions.

- Collaboration and connectivity goals remain relevant, as connecting to external data sources, collaboration tools, and partners accounts for 10 points.

- Cost optimization is a secondary factor, with cost reduction receiving 6 points.

- Environmental considerations currently carry limited weight, as reducing greenhouse gas emissions accounts for only 3 points.

(Sources: Infosys Knowledge Institute)

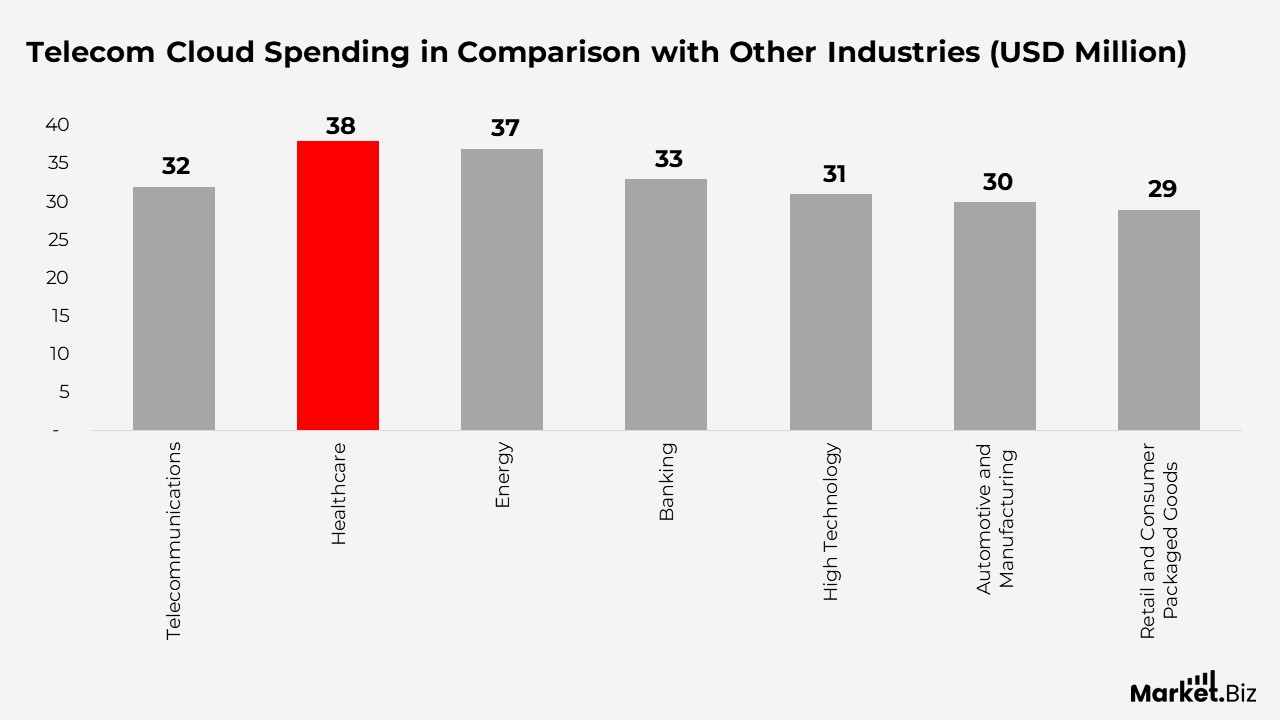

Telecom Cloud Spending in Comparison with Other Industries Statistics

- Telecommunications companies report an average cloud spend of $32 million, placing the sector in the middle of the industry comparison.

- Healthcare leads overall cloud investment, with average spending of $38 million, driven by data-intensive and digital care workloads.

- Energy organizations follow closely, allocating around $37 million to cloud platforms for analytics and operational optimization.

- Banking institutions maintain strong cloud adoption, with average spending of $33 million to support digital services and compliance requirements.

- High technology firms record average cloud spending of $31 million, reflecting ongoing needs for scalable development and infrastructure.

- Automotive and manufacturing companies show moderate cloud investment levels, with average spend of $30 million.

- Retail and consumer packaged goods companies report the lowest cloud spending among the compared sectors, averaging $29 million.

(Sources: Infosys Knowledge Institute)

Cloud Investment Momentum Accelerates Across Telecom

- Cloud spending increased over the past year for a clear majority of telecom companies, with 66% reporting higher spend, closely aligned with the 68% increase seen across all industries.

- A significant portion of telecom firms maintained stable cloud budgets, as 32% indicated their spending stayed about the same, compared with 29% across all sectors.

- Only a small share of organizations reduced cloud spending in the previous year, with just 2% of telecom companies and 3% across all industries reporting a decline.

(Sources: Infosys Knowledge Institute)

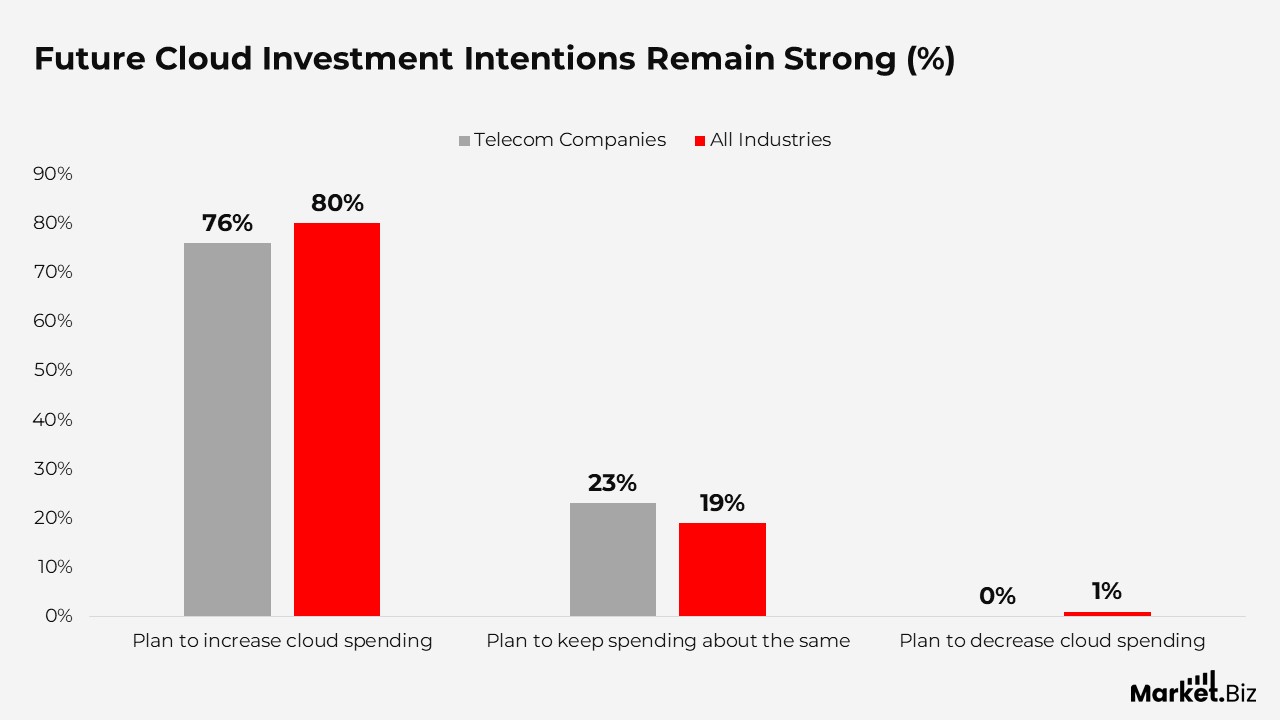

Future Cloud Investment Intentions Remain Strong

- Looking ahead, cloud spending is expected to rise further, with 76% of telecom companies planning to increase cloud investment in the coming year.

- Growth expectations are even stronger across the broader market, as 80% of organizations across all industries anticipate higher cloud spending.

- Budget stability is expected among a smaller group, with 23% of telecom firms planning to keep cloud spend at similar levels, compared with 19% across all industries.

- Planned reductions in cloud spending remain minimal, with 0% of telecom companies and only 1% of organizations overall expecting to decrease cloud budgets.

(Sources: Infosys Knowledge Institute)

Cloud Utilization Lags Behind Commitments in Telecom

- Telecom companies have, on average, consumed 48% of the cloud capacity they have already contracted.

- Just over half of committed cloud resources remain unused, with 52% still unutilized across telecom organizations.

(Sources: Infosys Knowledge Institute)

Enterprise Cloud Adoption

- Cloud adoption was limited before 2009, with annual uptake remaining between 1% and 2% as enterprises were still in early evaluation stages.

- Adoption momentum increased from 2010, with 11% of companies starting cloud use in 2010 and 10% in 2011, signaling broader enterprise acceptance.

- The most active phase of cloud migration occurred between 2012 and 2014, with 14% adoption in 2012, peaking at 16% in 2013, and sustaining 14% in 2014.

- This period is widely regarded as the prime era of cloud migration, reflecting growing platform maturity and organizational confidence.

- Post-2015, the pace of new cloud adoption declined, with 10% in 2015 and falling to 6% or lower from 2016 onward.

- By 2020 and beyond, first-time cloud adoption became minimal, dropping to 2% in 2020 and stabilizing near 1% annually between 2021 and 2022, indicating a mature cloud adoption landscape.

(Sources: Infosys Knowledge Institute)

Telecom Cloud Vendor Usage Patterns Statistics

- Single-vendor cloud strategies are uncommon in telecom, with only 8% of companies relying on just one cloud provider.

- Two-vendor setups are also limited, as 14% of telecom organizations report using only two cloud vendors.

- The most common approach is a three-vendor strategy, adopted by 34% of telecom companies, reflecting a clear shift toward diversified cloud ecosystems.

- Four cloud vendors are used by 27% of organizations, reinforcing the growing preference for multi-cloud flexibility and risk distribution.

- A smaller but notable share of telecom firms operate highly complex environments, with 13% using five cloud vendors.

- Usage of more than five vendors remains rare, accounting for just 3%, indicating practical limits to cloud portfolio expansion.

(Sources: Infosys Knowledge Institute)

Cost Complexity in Telecom Cloud Environments Statistics

- Cloud executives in the telecom sector show the lowest confidence in their ability to manage cloud costs effectively across core cost control activities.

- Just 53% of telecom organizations report having a clear and comprehensive view of their cloud-related costs, indicating gaps in cost visibility.

- Active cost optimization remains limited, with only 46% of respondents stating that their organizations consistently optimize cloud spending.

- Predicting future cloud costs is equally challenging, as just 46% of telecom companies feel confident in their ability to forecast upcoming cloud expenses.

- These findings highlight growing cost complexity as cloud environments scale, underscoring the need for stronger governance, monitoring, and financial management practices.

(Sources: Infosys Knowledge Institute)

Respondent Distribution Reflects Diverse Industry Input

- Automotive and manufacturing recorded the highest number of survey participants, with 412 respondents contributing insights.

- Healthcare followed closely, with 403 respondents, reflecting strong engagement from healthcare organizations.

- Telecommunications also showed substantial representation, with 401 respondents included in the survey.

- Retail and consumer packaged goods accounted for 400 respondents, indicating balanced participation levels.

- Banking was similarly well represented, with 399 respondents providing input.

- Energy and utilities had a moderate level of participation, with 305 respondents.

- High technology recorded the lowest respondent count among the listed industries, with 203 participants.

(Sources: Infosys Knowledge Institute)

Firmographic Breakdown of Survey Respondents

Company Revenue Profile

- The largest share of respondents came from enterprises with annual revenues above $5 billion, totaling 664 participants.

- Companies in the $3 billion to $5 billion revenue bracket were represented by 590 respondents, indicating strong participation from large organizations.

- Firms generating between $1 billion and $3 billion in annual revenue accounted for 512 respondents.

- Mid-sized organizations with revenues ranging from $500 million to $900 million contributed 526 respondents.

- Smaller companies with revenues below $500 million had comparatively lower representation, with 231 respondents.

Job Level Distribution

- Executive-level leaders, including vice presidents and senior executives, formed the largest respondent group, with 1,127 participants.

- Mid-level management accounted for 847 respondents, providing insights from operational and functional leadership roles.

- C-level executives contributed 549 responses, ensuring that strategic and top-level perspectives were reflected in the survey.

Company Age Distribution

- Organizations founded between 1990 and 1999 formed the largest respondent group, with 1,035 participants.

- Companies established between 2000 and 2009 also showed strong representation, accounting for 907 respondents.

- Firms founded in the period from 2010 to the present contributed 339 respondents, reflecting participation from newer organizations.

- Companies established between 1980 and 1989 were represented by 153 respondents.

- The smallest share of respondents came from organizations founded before 1980, totaling 89 participants.

Cloud Role Responsibilities

- Strategic cloud decision-makers who define the vision and direction for cloud initiatives accounted for 738 respondents.

- Evaluation-focused roles responsible for planning, designing, and assessing cloud initiatives formed the largest cloud role group, with 834 respondents.

- Implementation-focused respondents involved in executing cloud initiatives contributed 525 responses.

- Operational roles managing cloud environments accounted for 426 respondents, highlighting ongoing management responsibilities within cloud programs.

(Sources: Infosys Knowledge Institute)

Public Cloud Adoption and Usage

- Public cloud adoption is nearly universal, with 96% of organizations using at least one public cloud platform.

- On average, companies deploy around 50% of their workloads in public cloud environments.

- Organizations typically rely on multiple providers, with an average of 2.2 public clouds in use.

- Data storage continues to shift outward, as 48% of enterprise data is now stored in public cloud infrastructure.

Private Cloud Adoption and Industry Trends

- Private cloud usage remains strong, with 84% of organizations operating at least one private cloud environment.

- Companies run an average of 32% of their workloads on private cloud infrastructure.

- The private cloud market is expanding rapidly, with revenue expected to reach $528.36 billion by 2029.

- Telecommunications leads private cloud adoption, with 64% of telecom organizations using private cloud systems, making it the only sector where private cloud use exceeds public cloud reliance.

Hybrid Cloud Adoption

- Hybrid cloud architectures, which combine public cloud, private cloud, and on-premises systems, are becoming mainstream across enterprises.

- Nearly 80% of organizations use multiple public clouds, while 60% report operating more than one private cloud.

- Further, among companies generating over $500 million in annual revenue, 56% have adopted a hybrid cloud strategy.

- A majority of IT leaders, around 70%, believe successful digital transformation is difficult without a strong hybrid cloud foundation.

Telecom Cloud Service Delivery Models Statistics

- All major cloud delivery models continue to expand, with infrastructure-as-a-service driving broader adoption of platform and software services.

- End-user spending on IaaS is projected to grow by 26.6% in 2024 as enterprises migrate and modernize applications.

- PaaS spending is expected to increase by 21.5% in 2024, reflecting growing demand for development and integration platforms.

- SaaS spending growth is forecast at 15.9%, rising from $205,221 million in 2022 to $243,991 million in 2024.

Industry Cloud Platforms

- Industry-specific cloud platforms are emerging as a major growth driver by combining IaaS, PaaS, and SaaS into tailored solutions.

- Further, the adoption of generative AI is accelerating this trend due to the need for industry-level customization.

- By 2027, more than 70% of enterprises are expected to use industry cloud platforms, compared with less than 15% in 2023.

Cloud Data Storage Trends

- Cloud storage is becoming the primary data repository, with 50% of global data expected to be stored in the cloud by 2025, up from 25% in 2015.

- Total global data creation is projected to reach 200 zettabytes by 2025, driven by digital services and connected devices.

- The global smartphone base is expected to reach 7,743.6 billion devices by 2028, further accelerating data generation and cloud storage demand.

Insights of Cloud Security

- Security remains a major concern, with 95% of organizations expressing worry about cloud security risks.

- Moreover, the average cost of a data breach reached $4.5 million in 2023, reinforcing the financial impact of security failures.

- Misconfiguration is the leading cause of cloud security incidents, accounting for 68% of reported issues.

- Other major threats include unauthorized access (58%), insecure interfaces (52%), and account hijacking (50%).

- Further, despite these risks, 94% of organizations report improved security after moving to the cloud.

- Compliance is also simplified, as 91% of companies say cloud adoption helps meet government and regulatory requirements.

Cloud Gaming Market Trends

- Cloud gaming adoption is accelerating due to improved connectivity and increased investment in streaming platforms.

- Moreover, the global cloud gaming market is expected to grow from $2.38 billion in 2022 to $8.17 billion by 2025.

- Worldwide, an estimated 293 million users currently participate in cloud gaming, highlighting strong consumer uptake.

(Sources: Spacelift, Statista)

Conclusion

Telecom cloud statistics show that cloud computing has become a foundational element of telecom operations rather than a transitional technology. The findings point to consistent growth in cloud investment, widespread adoption of multi-cloud environments, and increasing reliance on cloud-native platforms to enhance flexibility and accelerate service innovation.

At the same time, the data reveals ongoing challenges related to cost management, utilization efficiency, and governance, particularly as cloud footprints expand. Taken together, these trends suggest that telecom operators are firmly committed to cloud-led transformation, with the next phase focused on improving financial discipline, operational control, and the alignment of cloud usage with long-term business objectives.

FAQ’s

Telecom cloud statistics offer a quantitative view of how telecom operators are adopting, deploying, and managing cloud technologies across their networks and IT environments. They highlight trends in usage, investment patterns, deployment models, and operational performance.

The move toward cloud is driven by the need to modernize legacy infrastructure, support virtualized and software-based networks, enable 5G capabilities, and improve agility in launching and scaling digital services.

Most telecom operators rely on a combination of public, private, and hybrid cloud environments. Multi-cloud approaches are increasingly preferred to enhance flexibility, manage vendor dependency, and meet performance and regulatory requirements.

Telecom operators often face difficulties related to cost transparency, underutilized cloud capacity, forecasting future spend, and maintaining effective governance as cloud environments grow in complexity.

Current trends indicate that cloud will remain a central component of telecom operations, with future efforts focused on optimizing usage, improving financial control, strengthening security, and aligning cloud initiatives with long-term business goals.