Introduction

Cyber Insurance Statistics: As businesses encounter escalating challenges from data breaches, ransomware attacks, and various forms of cybercrime, cyber insurance has become an essential tool for managing these risks. The rapid growth of the digital economy and the increasing dependence on online operations have made cyber insurance a key strategy for organizations to protect themselves from the financial impact of cyber incidents.

In recent years, the demand for cyber insurance has grown significantly, fueled by a greater awareness of cyber threats and the need for all-encompassing coverage. The rise in cyberattacks and stricter data protection regulations has played a major role in this trend.

Cyber insurance offers protection against a broad spectrum of cyber risks, such as security breaches, data loss, business interruptions, and reputational harm, helping companies secure their operations and maintain financial stability.

Editor’s Choice

- 24% of senior technology leaders in the US evaluate cyber threat exposure every month.

- 72% of senior technology leaders express some level of confidence in their present cyber risk coverage.

- 78% of IT or security teams manage their organization’s cyber insurance.

- 52% of senior technology leaders are responsible for leading the cyber insurance selection process.

- 82% consider financial protection as the key factor when assessing the value of cyber risk insurance.

- Senior technology leaders show a near 20% divide in their familiarity with liability coverage.

- Only 25% of technology leaders report that their current policy terms are very clear.

- For 39%, disaster recovery support is deemed a critical aspect.

- 100% of senior technology leaders would make revisions to their policies following a cyber incident.

- 24% of senior technology leaders claim that their cyber insurance policy has no impact on their cybersecurity planning.

- For 29% of technology leaders, disaster recovery plans are only somewhat aligned with policy requirements.

- 19% feel that their organization is only slightly prepared for a cybersecurity audit.

- The top concern when filing a claim for 52% of senior technology leaders is general issues.

- Only 19% are very satisfied with their insurer’s support and communication.

- The Southern US is home to 72% of senior technology leaders.

General Cyber Insurance Statistics

- 66% of US adults are familiar with cyber insurance, according to a survey by Security.org.

- The main reasons for not having cyber insurance are the concerns about high costs (34%) and the need for more research (40%).

- In cyber insurance claims due to data breaches, 71% of the loss is covered by the policy, with 44% from insurer payments and 27% from insured payments (including retention).

- The average cost breakdown for a data breach includes 18% for defense, 13% for legal and cybersecurity experts, 21% for forensic costs, and 14% for credit and theft monitoring services.

- In 2% of cyber insurance claims, the total cost of a breach exceeded $100 million.

- Common reasons for coverage not being triggered include the use of unapproved vendors and activities without insurer consent.

- In the 2022 Coalition cyber insurance claims report, the ransomware model matured, with the average demand on customers rising by 20% and claim severity increasing by 10%.

- Small businesses saw a 40% rise in ransomware attacks and a 56% increase in fund transfer fraud incidents.

- Losses from fund transfer fraud grew by 69% from 2020 to 2021, with 68% of companies with revenues between $25 million – $100 million seeing increased frequency.

Detailed Stats

- For healthcare-related claims, the main causes are:

- Malicious data breaches: 18%

- Accidental data breaches: 29%

- Ransomware: 8%

- Stolen or lost devices: 16%

- In the IT and Communications sector, the primary causes of claims are:

- Malicious data breaches: 24%

- Accidental data breaches: 18%

- Ransomware: 11%

- Social engineering: 10%

- For the insurance sector, major loss triggers are:

- Malicious data breaches: 39%

- Accidental data breaches: 35%

- Ransomware: 4%

- Social engineering: 7%

- Retail and wholesale businesses saw claims due to:

- Malicious data breaches: 30%

- Social engineering: 11%

- Accidental data breaches: 8%

- Manufacturing companies experienced claims from:

- Malicious data breaches: 22%

- Social engineering: 30%

- Ransomware: 9%

(Source: Statista, ASTRA IT, Inc.)

Types of Cyber Insurance Claims

- Ransomware attacks

- Business email compromise

- Malware attacks

- Supply chain attacks

- Phishing attacks

(Source: NetDiligence)

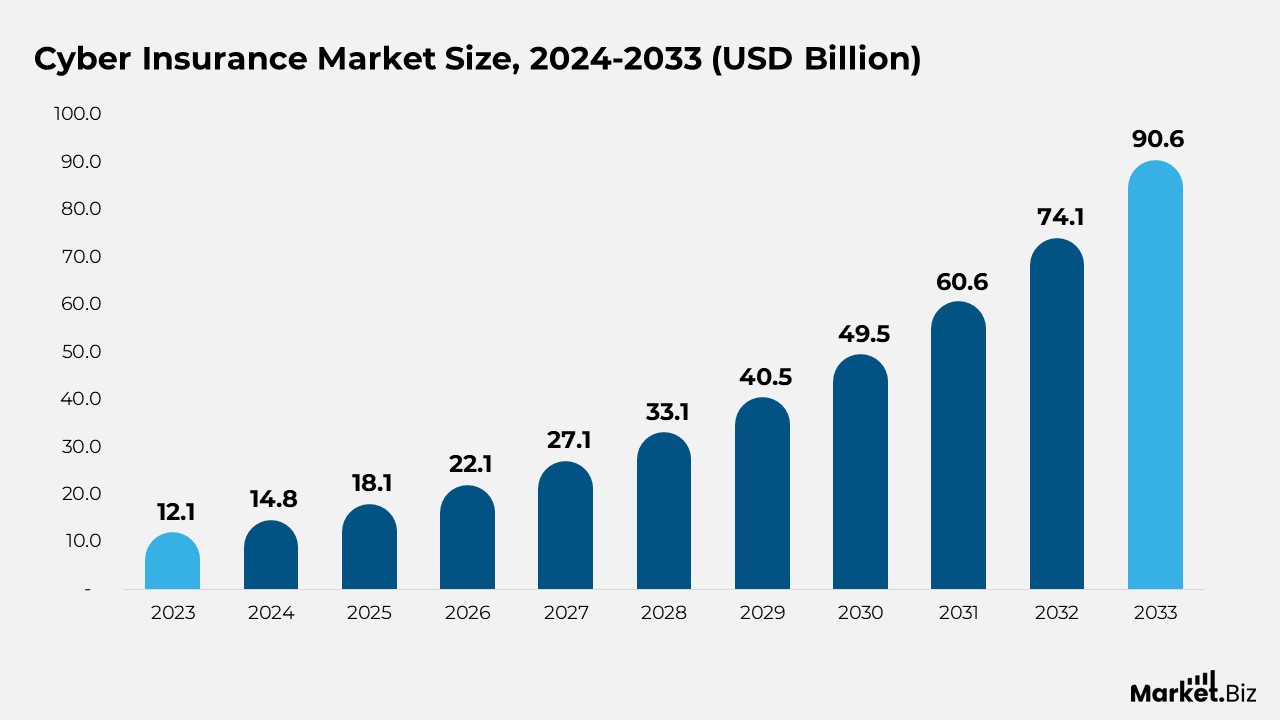

Cyber Insurance Market Size

- According to Market.us, the cyber insurance market is expected to rise from $14.8 billion in 2024 to $90.6 billion by 2033, representing a compound annual growth rate (CAGR) of 22.3% from 2024 to 2033.

- The growth of the cyber insurance market is fueled by increasing awareness of cyber risks among businesses, driving

- organizations to adopt proactive risk management strategies.

- In 2023, the Standalone segment dominated the Cyber Insurance Market, holding 68.2% of the market share due to its specialized coverage.

- In 2023, the Third-Party Coverage segment led the market with 62.1% share, as it provides essential liability protection for businesses.

- In 2023, the Large Enterprises segment captured 72.4% of the market share, driven by the high cyber risk exposure of larger organizations.

- In 2023, the BFSI sector held 28.3% of the market share due to the high sensitivity of financial data and severe cyber threats.

- In 2023, North America led the cyber insurance market with a 37.6% share and USD 4.5 billion in revenue, driven by a high prevalence of cyberattacks and a concentration of tech and financial giants.

(Source: Market.us)

Experience with Cyber Insurance

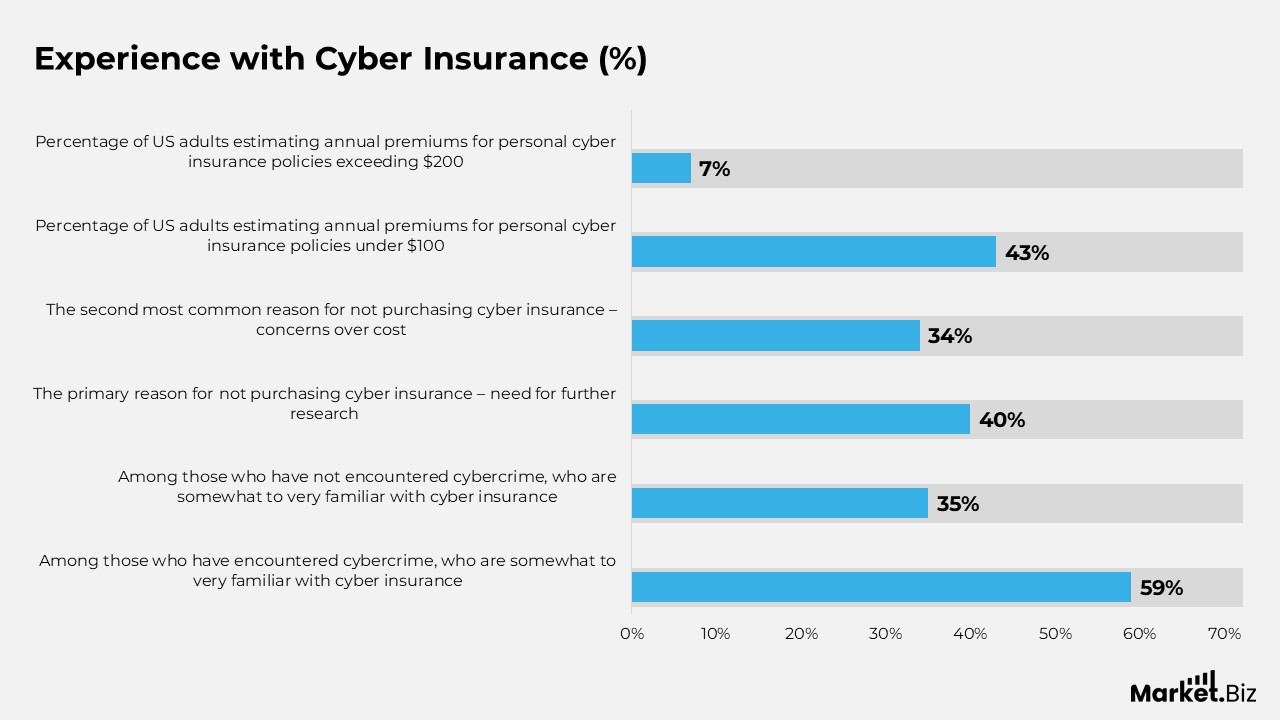

- 66% of US adults are aware of cyber insurance in general.

- Among those who have encountered cybercrime, 59% report being somewhat to very familiar with cyber insurance, compared to 35% of those who have not experienced cybercrime.

- The primary reason individuals haven’t purchased cyber insurance is the need for further research, cited by 40%, followed by concerns over cost at 34%.

- 43% of US adults estimate that the annual premiums for personal cyber insurance policies providing up to $25,000 in coverage cost less than $100, while only 7% believe the premiums exceed $200.

(Source: Statista, Centerfield Media Company, Security.org)

Year-on-Year Trends in Cyberattack Incidents

- Social engineering attacks (phishing, vishing, pharming, etc.) rose significantly from 114,702 in 2019 to 341,342 in 2020, marking a 197.60% increase.

- Credit card fraud increased by 22.50%, from 14,378 cases in 2019 to 17,614 in 2020.

- Investment scams saw a notable rise of 119.80%, going from 3,999 in 2019 to 8,788 in 2020.

- Malware incidents decreased by 40%, dropping from 2,373 in 2019 to 1,423 in 2020.

- Identity theft cases surged by 169.90%, growing from 16,053 in 2019 to 43,330 in 2020.

- Ransomware attacks increased by 20.90%, rising from 2,047 in 2019 to 2,474 in 2020.

- Denial of service (including TDoS) attacks grew by 49.20%, increasing from 1,353 in 2019 to 2,018 in 2020.

(Source: Security.org, Statista)

Cyber Insurance Claims Statistics

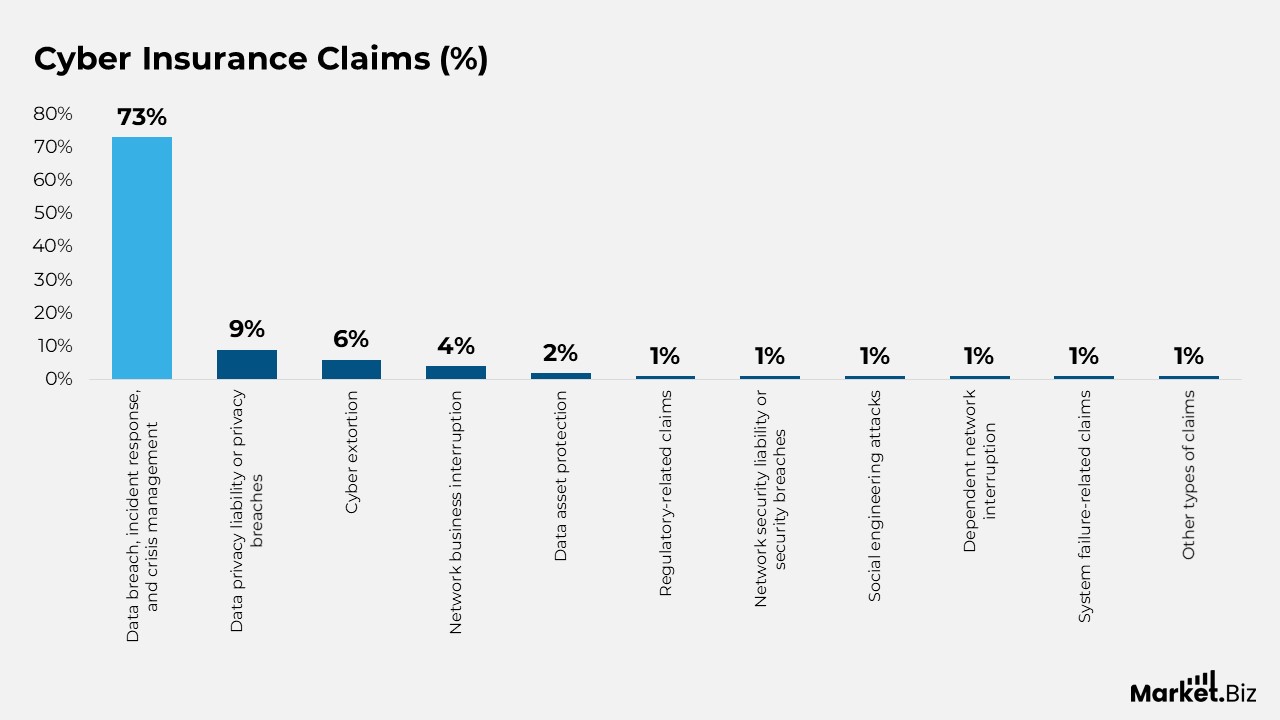

- Data breach, incident response, and crisis management claims represent 73% of the total claims.

- Claims related to data privacy liability or privacy breaches account for 9% of the claims.

- Cyber extortion claims make up 6% of the overall claims.

- Network business interruption claims contribute 4% to the total claims.

- Data asset protection claims account for 2% of all claims.

- Regulatory-related claims represent 1% of the total claims.

- Claims arising from network security liability or security breaches contribute 1% to the total.

- Social engineering attacks comprise 1% of the overall claims.

- Dependent network interruption claims make up 1% of the total claims.

- System failure-related claims account for 1% of the claims.

- Other types of claims contribute 1% of the total claims.

(Source: Security.org, DemandSage)

Causes of Data Breaches

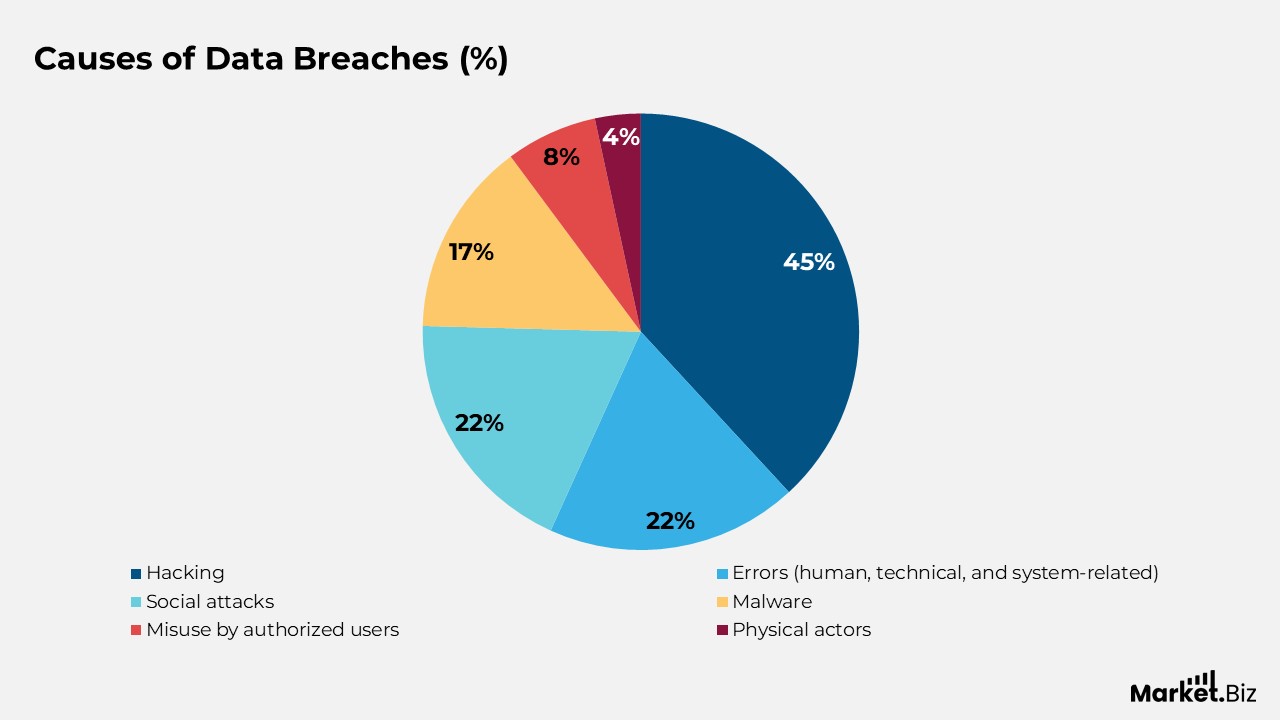

- 45% of the breaches were attributed to hacking.

- 22% of breaches resulted from errors, including human, technical, and system-related issues.

- Social attacks caused 22% of breaches.

- 17% of breaches occurred due to malware.

- 8% of breaches were linked to misuse by authorized users.

- Physical actors caused 4% of breaches.

(Source: Security.org, Statista)

Cybercrime by the Numbers

- In 2020, 1 in 6 businesses impacted by cyberattacks were victims of ransomware, with nearly half of them paying the ransom.

- The FBI’s Internet Crime Complaint Center (IC3) reported a 69% increase in cybercrime reports in 2020 compared to the previous year. On average, the FBI received 2,000 cybercrime reports per day in 2020.

- During 2020, data breaches compromised over 37 billion personal records, with 82% of those breaches resulting from just five incidents.

- In 2020, 49 million victims of identity fraud collectively lost $56 billion, averaging $1,100 per victim.

- Among individuals somewhat familiar with cyber insurance, 70% had experienced a cyberattack, followed by 69% who had encountered identity theft, 64% affected by cyberbullying, and 69% who had fallen victim to cyber extortion.

(Source: Security.org, DemandSage)

Causes of Cyber Insurance Claims

Phishing

- Phishing has remained a prevalent form of cybercrime for three consecutive years.

- In 2021, there were 323,972 reported phishing victims.

- On average, phishing victims lost the least amount of money, with an average loss of $136 per victim, compared to other attacks like investment fraud.

- The most impersonated brands in phishing attacks were Google and Amazon, accounting for 13% of cases, followed by WhatsApp and Facebook at 9%, and Apple and Netflix at 2%.

Scams

- In 2022, there were 1,153 cyber insurance claims related to business email compromise (BEC) scams.

- 57% of these BEC attacks occurred in 2020 and 2021.

- Business email compromise accounted for approximately 10% of the total incident cost in cyber insurance claims in 2022.

- Over 450 COVID-19-related financial support scams were reported in 2020.

Credit Fraud

- The years 2021-2022 were marked by notable incidents of credit fraud, bank fraud (39%), (-1%), and identity theft (7%), with a significant rise in fraudsters using stolen information to open bank accounts in victims’ names, increasing by 64% in 2021.

- 389,845 cases of credit fraud were reported in 2021, showing a slight decrease compared to 2020.

- Aside from the surge in wire transfer frauds in 2020, the average amount involved in wire fraud transfers remained between $166,000 and $211,000, with incident costs ranging from $188,000 to $392,000.

- In 2021, nearly 1.6 million identity theft cases were reported, with the most prevalent type being government document or benefits fraud.

- Identity fraud caused a loss of over $56 billion in 2021 alone.

Malware

- Ransomware and malware attacks are increasingly targeting businesses, with over 4,500 victims reported in 2021.

- Between 2019 and 2021, 55% of 1,500 claims were attributed to ransomware.

- In 2022, there were 2,123 ransomware-related claims, with 45% of these incidents occurring in 2020 and 2021.

- Ransomware emerged as the leading cause of loss for small and medium-sized enterprises (SMEs), accounting for 51% of the total incident cost, followed by hacking, which contributed to 18% of the costs.

(Source: Security.org, DemandSage)

Conclusion

The increasing awareness and significance of cyber insurance are evident as both businesses and individuals become more attuned to the risks posed by cyber threats. Moreover, a large portion of the US population is aware of cyber insurance, but challenges such as the need for more research and concerns about affordability still hinder broader adoption.

Examining cyber insurance claims reveals that malicious data breaches, ransomware, and social engineering are the leading causes of claims across multiple sectors, with healthcare, IT, communications, and retail experiencing varied loss triggers. Further, the rise of ransomware has notably intensified, leading to a significant increase in attacks and related costs, particularly impacting small businesses.

Further, as the cyber threat landscape evolves, the demand for comprehensive, accessible cyber insurance solutions will remain crucial to managing potential losses and safeguarding sensitive data.

FAQ’s

Cyber insurance is a policy designed to protect businesses and individuals from the financial risks associated with cyber threats such as data breaches, cyberattacks, and other online security incidents. It typically covers costs like data recovery, legal expenses, and liability claims.

With the increasing complexity and frequency of cyber threats, cyber insurance acts as a financial safeguard, assisting businesses in recovering from cyberattacks. It helps cover legal fees, reputation management, and operational disruptions, making it an essential tool for businesses of all sizes.

Cyber insurance generally covers incidents such as data breaches, cyber extortion (including ransomware attacks), business interruptions resulting from cyber events, legal expenses, public relations support, and costs for notifying individuals affected by a breach.

The primary advantages of cyber insurance include financial protection from cyberattacks, coverage for legal and compliance costs, support for recovery efforts, and assistance in managing reputational harm following a data breach.

Common exclusions in cyber insurance policies can include losses due to social engineering attacks (e.g., phishing), employee negligence, attacks from hostile governments, and incidents that occurred before the policy’s activation. The specific terms of coverage vary depending on the provider.