Introduction

Digital twin statistics provide quantitative insights into the adoption, deployment, and performance of virtual replicas of physical assets, processes, and systems across industries. These statistics track key indicators, including adoption rates, investment trends, operational efficiency gains, cost optimisation, predictive maintenance accuracy, and lifecycle management improvements.

As organizations increasingly adopt data-driven and simulation-based decision-making, digital twin metrics reflect the integration of IoT, real-time data analytics, artificial intelligence, and cloud platforms.

Across sectors including manufacturing, healthcare, energy, and smart infrastructure, digital twin statistics help benchmark deployment maturity, regional adoption patterns, and high-impact use cases, offering a clear view of the technology’s scalability, effectiveness, and long-term value in global digital transformation efforts.

Editor’s Choice

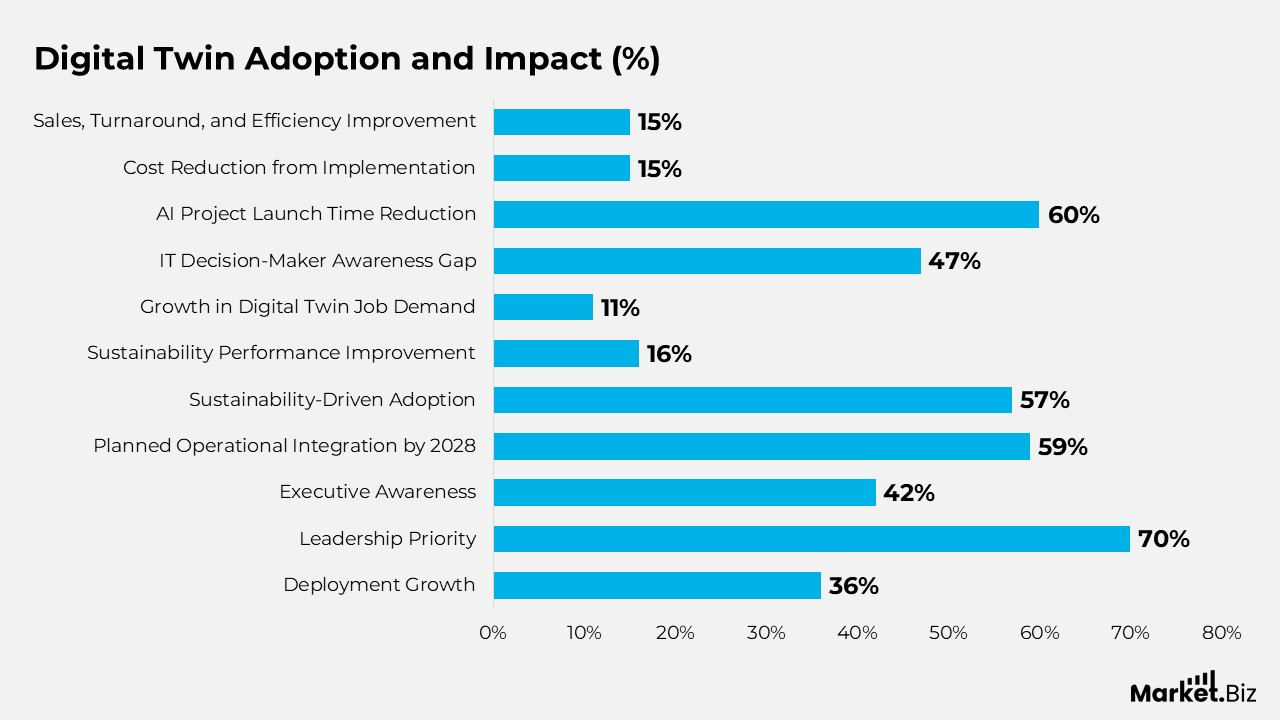

- Enterprise commitment is strengthening, as nearly 70% of technology leaders and industry stakeholders actively prioritize or fund digital twin initiatives across core operations.

- Strategic maturity is improving, with 73% of organizations now holding a long-term digital twin strategy, up from 57% just two years earlier.

- Sustainability has emerged as a primary driver, with 57% of organisations investing in digital twins to achieve average sustainability performance improvements of 16%.

- Operational impact is measurable, as digital twins deliver 15% gains in sales, turnaround time, and efficiency, while system and asset performance improvements exceed 25%.

- Time and cost efficiencies remain a key advantage, with digital twins reducing AI-enabled project launch timelines by up to 60% and lowering implementation costs by around 15%.

- Sector-specific outcomes highlight strong value creation, including up to 20% reductions in unplanned downtime in oil and gas, 30% improvements in traffic flow in smart cities, and 35% gains in building operations and maintenance efficiency.

- Despite rapid growth, awareness gaps persist: 47% of IT decision-makers remain unfamiliar with digital twins, underscoring the continued need for education and skills development.

(Source: Capgemini, McKinsey, Astute Analytica, IoT Analytics, World Economic Forum)

Digital Twin Adoption and Impact Statistics

- Digital twin deployments are projected to expand at an average growth rate of 36% over the next five years, reflecting rapid enterprise-scale adoption.

- Around 70% of technology leaders in large organizations actively prioritize and fund digital twin initiatives within their digital transformation strategies.

- Nearly 42% of senior executives already recognize the value of digital twins, while 59% plan to integrate them into core operations by 2028.

- Stakeholders across healthcare, agriculture, urban planning, aerospace, marine engineering, and Earth systems increasingly acknowledge digital twins as high-value analytical tools.

- Sustainability drives adoption, with 57% of organizations citing environmental performance improvement as a primary reason for investing in digital twins.

- Organizations leveraging digital twins report an average 16% improvement in sustainability-related performance metrics.

- Demand for digital twin expertise continues to rise, with job postings mentioning “digital twin” increasing by 11% compared to two years earlier.

- Awareness gaps persist, as 47% of IT decision-makers still remain unfamiliar with digital twin concepts.

- Digital twins significantly accelerate innovation cycles, cutting AI-enabled project launch times by up to 60% and reducing implementation costs by around 15%.

- Enterprises using digital twins achieve measurable business gains, including 15% improvements in sales, turnaround time, and operational efficiency, as well as increases in system performance exceeding 25%.

(Source: Capgemini, McKinsey, Nature Computational Science, IoT Analytics)

Digital Twin in Aerospace and Defence

- Around 24% of aerospace and defence organizations currently prioritize digital twins to optimize full product lifecycle operations, while another 50% plan adoption within the next 1–2 years.

- Sustainability optimisation remains an emerging use case, with 19% already using digital twins and an additional 55% planning to implement them within 1–2 years.

- The share of organizations with a long-term digital twin strategy rose to 73% in 2023, up from 57% in 2021, highlighting growing strategic maturity.

- Nearly 78% of organisations cite rapid technological advancement as the primary driver of their investment in digital twins.

- Aerospace and defence companies are allocating about 2.7% of annual revenue to digital twin initiatives, representing a 40% year-over-year increase.

- Digital twins add value early in development, with 75% of organizations reporting benefits from the initial design phase.

- Operational reliability improves significantly, as 81% view digital twins as critical for enhancing system and equipment availability.

- Digital twin-enabled CFD modelling helped the U.S. Air Force save approximately €7.47 million by reducing wind-tunnel testing for the F-22 program.

- The U.S. Navy shortened large aircraft program development timelines by 25% through digital twins and related digital engineering tools.

(Source: Capgemini, Forrester Consulting, ResearchGate)

Digital Twin in Manufacturing

- About 29% of manufacturing companies worldwide have already implemented digital twin strategies, either fully or partially.

- Future adoption intent remains strong, with 65% of manufacturing technology decision-makers planning to use digital twins to optimise operations.

- Sustainability-driven use cases are gaining traction, with 67% planning to prioritize digital twin technologies to optimize full product lifecycle sustainability.

(Source: IoT Analytics, Forrester Consulting)

Digital Twin in Buildings and Construction

- Digital twin adoption can reduce building-related carbon emissions by up to 50%, supporting sustainability and climate targets.

- Operational and maintenance efficiency improves by around 35% when digital twins are integrated into building management systems.

- In the US, buildings account for over 30% of total greenhouse gas emissions, and digital twins combined with AI help predict maintenance needs, manage risks, test scenarios, and automate ESG reporting.

(Source: Astute Analytica, EY, World Economic Forum)

Digital Twin in the Oil and Gas Industry

- Companies deploying digital twins have reduced unplanned operational shutdowns by up to 20%, translating into potential savings of around €3.03 million per month per rig, or nearly €36.41 million annually.

- Close to 70% of key industry stakeholders consider digital twins critical to core operations, while approximately 27% have already implemented the technology.

- By the end of 2022, more than 43% of oil and gas companies had either adopted digital twins for predictive analysis or were prepared for near-term deployment.

(Source: Astute Analytica)

Digital Twin in Smart Cities

- The use of digital twins for advanced urban planning is expected to generate approximately €259.26 billion in cost savings for cities globally by 2030.

- Large-scale commercial facilities have demonstrated tangible efficiency gains, with digital twin-enabled energy management covering nearly 42 million square feet and delivering a 30% reduction in HVAC energy consumption.

- City-level implementations show strong operational impact, where digital twins using data from over 500 sources have improved traffic flow by up to 30%, reducing congestion, delays, and energy use.

- Academic and institutional campuses have also benefited, achieving 31% energy savings and cutting carbon emissions by 9.6 kilotons through digital-twin-based optimisation.

(Source: World Economic Forum, Capgemini)

Corporate Timelines for Sustainability and Digital Twin Initiatives

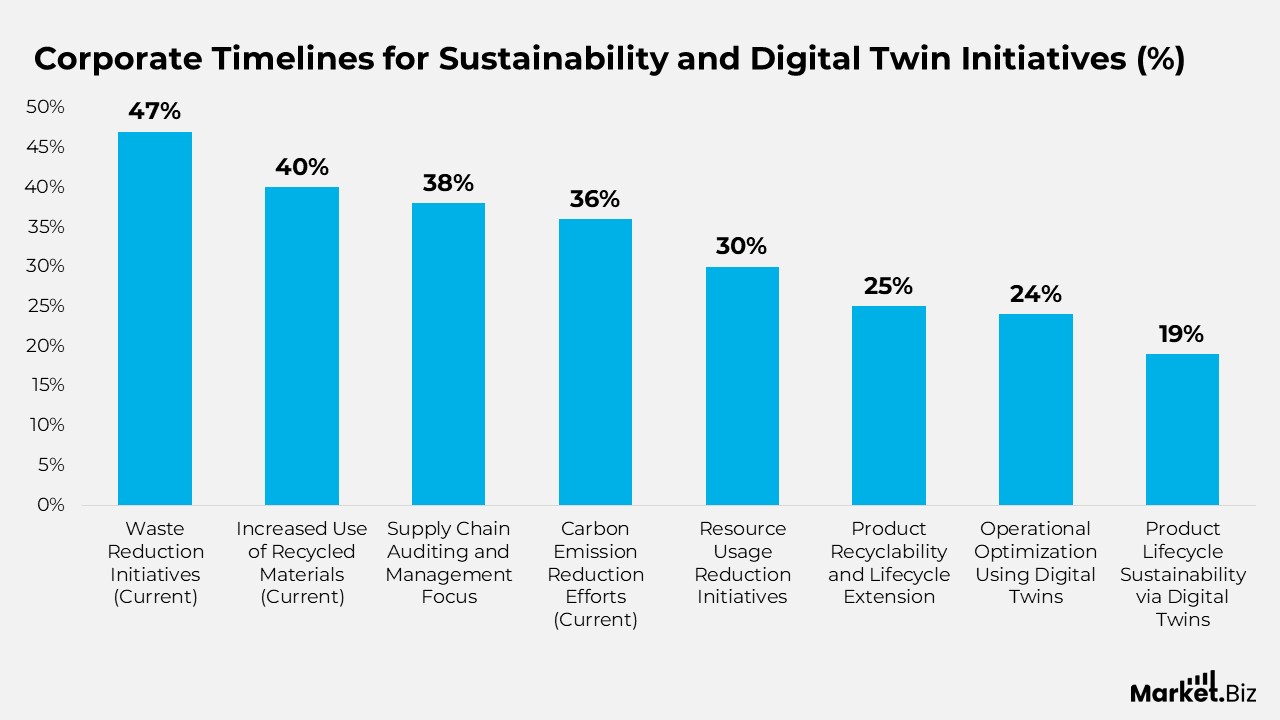

- 47% of companies are already prioritizing initiatives to reduce waste production today, indicating immediate action toward operational efficiency.

- 40% have begun focusing on increasing the use of recycled materials, while others are planning near-term adoption to support circular economy goals.

- 38% currently emphasize improving supply chain auditing and management, reflecting growing accountability across sourcing networks.

- 36% are actively working to reduce carbon emissions, with a significant share planning further action over the next 1–2 years.

- 30% of organizations are taking steps today to use fewer resources, aligning cost optimization with sustainability objectives.

- 25% are already making end products easier to recycle or extending product lifespan, showing early-stage design-for-sustainability efforts.

- 24% are currently using technologies such as digital twins to optimize operations, while 50% plan to prioritize this within 1–2 years and 25% within 3–5 years.

- 19% are actively applying digital twin technologies to optimize full product lifecycle sustainability, with 55% planning adoption in 1–2 years and 23% targeting 3–5 years.

(Source: Forrester Consulting, Hexagon)

Adoption of Standard Solutions for Product Design Deliverables by Organizational Maturity

- In mechanical hardware design, 25% of the least progressive organizations rely on standard solutions, compared with 47% among moderately progressive firms and a significantly higher 66% among the most progressive organizations.

- For electrical distribution systems, the use of standard solutions remains relatively balanced, with 36% adoption in the least progressive companies, 37% in the moderately progressive ones, and 30% in the most progressive group.

- In electronics and circuit board development, adoption of standard solutions rises with maturity, from 25% in the least progressive organisations to 46% in moderately progressive and 48% in most progressive organisations.

- Onboard or embedded software shows a significant maturity gap, with only 14% of the least progressive firms using standard solutions, compared with 52% of moderately progressive and 45% of most progressive organisations.

- Off-product data transfer technologies, such as IoT, demonstrate the strongest maturity correlation, with adoption rising from 50% in the least progressive organisations to 71% in moderately progressive organisations and peaking at 86% among the most progressive firms.

(Source: Siemens)

Advanced Solutions Adoption for Product Design Deliverables

- In mechanical hardware management, advanced solutions are absent among the least progressive organizations at 0%, rise sharply to 45% in moderately progressive firms, and reach 76% among the most progressive organisations.

- Electrical distribution systems show strong maturity-linked adoption, with 28% usage in the least progressive companies, increasing to 64% in the moderately progressive group and matching 76% in the most progressive group.

- For electronics and circuit board management, adoption of advanced solutions increases steadily from 30% in the least progressive organisations to 50% in moderately progressive organisations and 67% in the most progressive firms.

- Onboard or embedded software management is demonstrating widening adoption with maturity, moving from 13% in the least progressive organisations to 47% in the moderately progressive segment and 63% in the most progressive segment.

- Off-product data transfer technologies, such as IoT, show the strongest maturity effect, with 0% adoption among the least progressive organisations, rising to 63% among moderately progressive organisations, and peaking at 87% among the most progressive organisations.

(Source: Siemens)

Standardized Product Design Process Adoption by Organizational Maturity

- In concept design and early development, 65% of the least progressive organizations follow standardized processes, increasing to 77% among moderately progressive firms and reaching 98% in the most progressive group.

- System and architectural design standardization shows steady growth with maturity, rising from 57% in the least progressive organizations to 79% in moderately progressive and 96% in the most progressive companies.

- Detailed design processes demonstrate similar momentum, with 55% adoption in the least progressive organisations, 76% in moderately progressive organisations, and 89% in the most progressive firms.

- Prototyping and testing activities increasingly rely on standards, with adoption rising from 52% in the least progressive organizations to 78% in moderately progressive and 96% in the most progressive segment.

- Design review and release stages show strong standardization at higher maturity levels, increasing from 52% in the least progressive organizations to 80% in moderately progressive and 91% in the most progressive group.

- Change management processes exhibit the widest maturity gap, with 43% adoption in the least progressive organizations, rising to 67% in moderately progressive and reaching 96% among the most progressive organizations.

(Source: Siemens)

Standard Solution Usage in Product Design Execution

- During concept design and early development, only 9% of the least progressive organizations use standard solutions, compared with 27% among moderately progressive firms and 50% among the most progressive organizations.

- System design and architecture development shows a clear maturity gradient, with 14% adoption in the least progressive organizations, rising to 29% in moderately progressive and 42% in the most progressive group.

- In detailed design activities, the use of standard solutions increases from 16% in the least progressive organisations to 26% in the moderately progressive segment and peaks at 52% in the most progressive segment.

- Prototyping and testing demonstrate a growing reliance on standard solutions, moving from 15% adoption in the least progressive organisations to 33% in moderately progressive and 51% in the most progressive firms.

- Design review and release processes remain less standardized among the least progressive organizations at 10%, but adoption rises to 21% in moderately progressive organisations and reaches 50% among the most progressive group.

- Change management reflects similar patterns, with 9% adoption in least progressive organizations, increasing to 26% in moderately progressive and 40% in the most progressive organizations.

(Source: Siemens)

Advanced Solution Adoption in Production Engineering Deliverables

- In manufacturing tooling, advanced solution usage remains limited among the least progressive organizations at 12%, rises to 53% in moderately progressive firms, and reaches 88% in the most progressive organizations.

- NC machining shows a similar maturity-driven pattern, with 9% adoption in the least progressive organisations, rising sharply to 52% in moderately progressive organisations and peaking at 88% among the most progressive firms.

- Manufacturing cells demonstrate uneven adoption: 41% in the least progressive organisations, 31% in moderately progressive, and 83% in the most progressive segment.

- Production line deliverables increasingly rely on advanced solutions, moving from 33% adoption in the least progressive organizations to 55% in moderately progressive and 80% in the most progressive group.

- Manufacturing facilities show growing digital maturity, with advanced solution usage rising from 27% in the least progressive organizations to 54% in moderately progressive and 72% among the most progressive firms.

- Production transfer of data, including IIoT, shows strong maturity alignment, increasing from 38% adoption in the least progressive organisations to 66% in moderately progressive organisations and reaching 82% in the most progressive organisations.

(Source: Siemens)

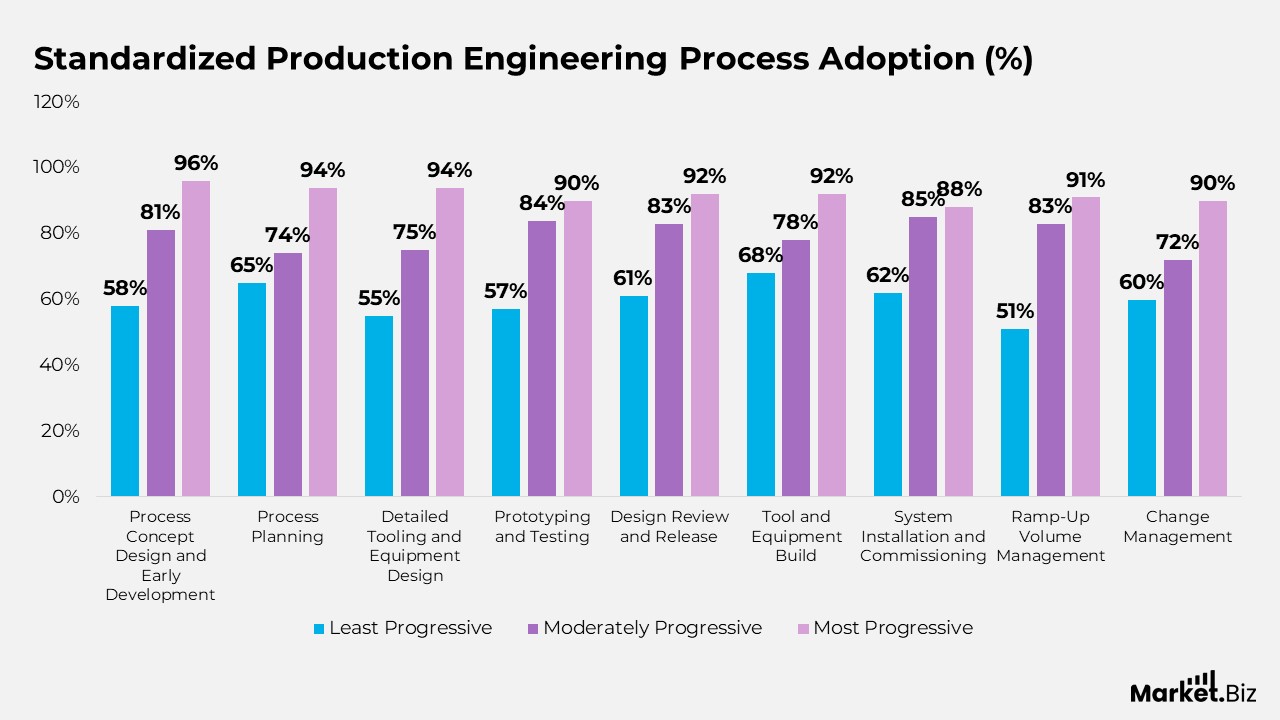

Standardized Production Engineering Process Adoption

- process concept design and early development, standardized execution is followed by 58% of the least progressive organizations, increases to 81% among moderately progressive firms, and reaches 96% in the most progressive group.

- Process planning shows a strong maturity effect, with 65% adoption in the least progressive organizations, 74% in moderately progressive, and 94% among the most progressive companies.

- Detailed tooling and equipment design relies on standards in 55% of the least progressive organizations, rising to 75% in moderately progressive and 94% in the most progressive segment.

- Prototyping and testing processes demonstrate increasing standardization, moving from 57% in least progressive organizations to 84% in moderately progressive and 90% in the most progressive group.

- The process, tool, and equipment design review and release stages show high maturity alignment, increasing from 61% in the least progressive organisations to 83% in moderately progressive organisations and 92% in the most progressive firms.

- Tool and equipment build activities follow standardized methods in 68% of the least progressive organizations, 78% in moderately progressive, and 92% in the most progressive segment.

- System installation and commissioning processes show rising consistency, with 62% adoption in the least progressive organizations, 85% in moderately progressive, and 88% among the most progressive companies.

- Ramp-up volume management reflects strong maturity-driven execution, increasing from 51% in the least progressive organizations to 83% in moderately progressive and 91% in the most progressive group.

- Change management processes display a clear maturity gap, with 60% adoption in least progressive organizations, rising to 72% in moderately progressive and reaching 90% among the most progressive organizations.

(Source: Siemens)

Standard Solution Adoption Across Production Engineering Execution

- In process concept design and early development, standardized solution usage remains limited at 7% among the least progressive organisations, increases to 30% in moderately progressive firms, and reaches 47% among the most progressive organisations.

- Process planning follows a similar maturity-driven pattern, with 12% adoption in the least progressive organizations, rising to 22% in moderately progressive and 40% in the most progressive group.

- Detailed tooling and equipment design shows stronger uptake with maturity, moving from 16% adoption in the least progressive organizations to 39% in moderately progressive and 49% among the most progressive firms.

- Prototyping and testing increasingly rely on standard solutions, rising from 6% in the least progressive organizations to 33% in the moderately progressive and 50% in the most progressive segment.

- Process, tool, and equipment design review and release demonstrate expanding standardization, increasing from 13% adoption in least progressive organizations to 35% in moderately progressive and 51% in the most progressive group.

- Tool and equipment build activities show steady growth in standardized execution, moving from 16% in the least progressive organizations to 34% in moderately progressive and 50% among the most progressive firms.

- System installation and commissioning show clear maturity alignment, with 20% adoption in the least progressive organizations, rising to 29% in moderately progressive and 49% in the most progressive segment.

- Ramp-up to volume activities display strong reliance on standard solutions at higher maturity levels, increasing from 17% in the least progressive organizations to 41% in moderately progressive and 53% among the most progressive companies.

- Change management reflects uneven adoption, with 11% usage in least progressive organizations, 36% in moderately progressive organizations, and 30% in the most progressive group.

(Source: Siemens)

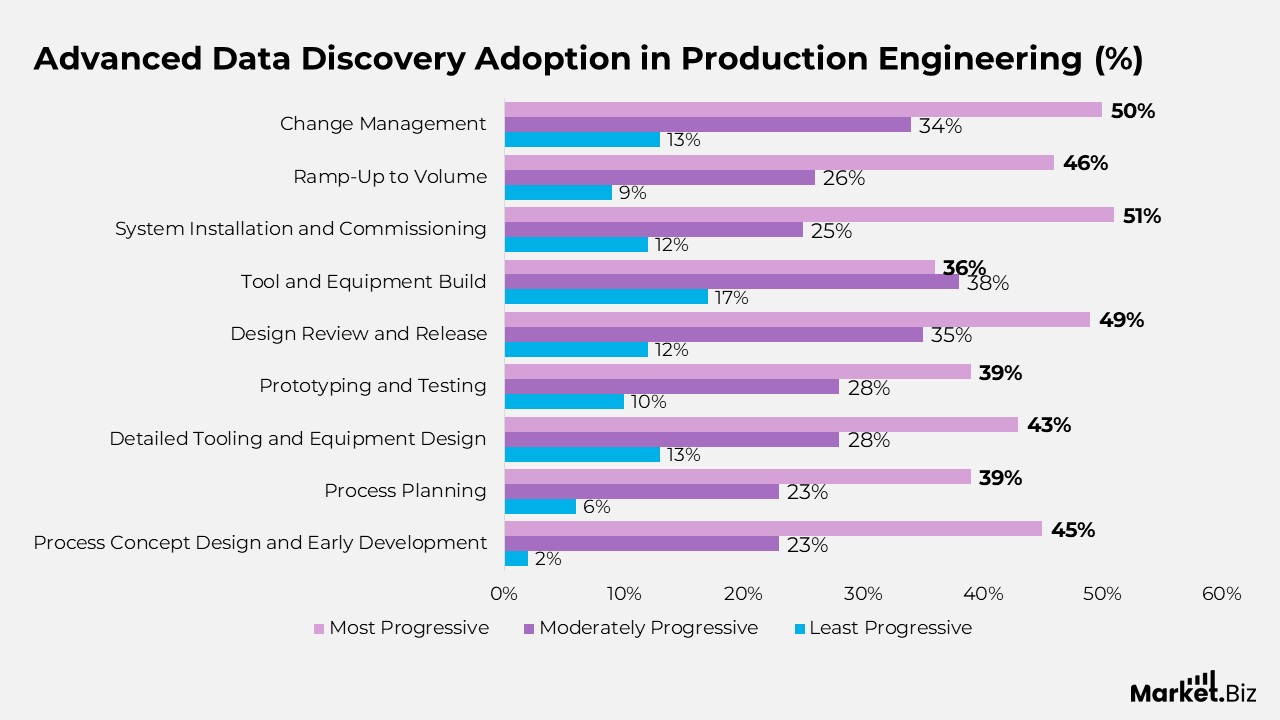

Advanced Data Discovery Adoption in Production Engineering

- During process concept design and early development, advanced data discovery tools are used by only 2% of the least progressive organizations, rising to 23% in moderately progressive firms and reaching 45% among the most progressive organizations.

- Process planning activities show gradual maturity-driven adoption, increasing from 6% in the least progressive organizations to 23% in moderately progressive and 39% in the most progressive group.

- In detailed tooling and equipment design, usage of advanced solutions grows from 13% in least progressive organizations to 28% in moderately progressive and 43% among the most progressive firms.

- Prototyping and testing stages increasingly rely on advanced data tools, moving from 10% adoption in least progressive organizations to 28% in moderately progressive and 39% in the most progressive segment.

- Process, tool, and equipment design review and release demonstrate strong maturity alignment, increasing from 12% in the least progressive organizations to 35% in moderately progressive and 49% in the most progressive group.

- Tool and equipment build activities show moderate growth in advanced solution usage, rising from 17% in least progressive organizations to 38% in moderately progressive and 36% among the most progressive firms.

- System installation and commissioning exhibit one of the strongest maturity gaps, with 12% adoption in the least progressive organizations, 25% in moderately progressive, and 51% in the most progressive segment.

- Ramp-up to volume processes shows expanding reliance on advanced data discovery tools, increasing from 9% in the least progressive organizations to 26% in moderately progressive and 46% among the most progressive companies.

- Change management reflects accelerating adoption, rising from 13% in the least progressive organisations to 34% in moderately progressive organisations and reaching 50% in the most progressive group.

(Source: Siemens)

Conclusion

Digital twin statistics demonstrate that the technology has moved beyond early experimentation and is becoming a critical pillar of enterprise digital transformation. Accelerating adoption rates, increasing budget allocations, and expanding industry use cases demonstrate that organisations increasingly depend on digital twins to improve operational efficiency, optimise asset lifecycles, and advance sustainability goals.

Quantifiable outcomes such as reduced downtime, faster development timelines, cost efficiencies, and enhanced system performance highlight the tangible value being realized. Strong results across manufacturing, aerospace and defence, oil and gas, buildings, and smart city applications further validate its scalability and cross-sector relevance.

However, persistent gaps in awareness and maturity indicate that the market remains in a growth and learning phase. Overall, the data confirms that organizations adopting digital twins strategically and early are securing meaningful performance advantages and strengthening their long-term data-driven capabilities.

FAQ’s

Digital twin statistics aim to explain how the technology is being adopted, scaled, and valued across industries by using measurable indicators related to growth, usage, and performance impact.

They illustrate the progression of organizations from basic digital modeling to advanced, real-time virtual replicas integrated with analytics, AI, and connected systems.

These statistics offer a macro-level view of how digital twins influence operational models, investment priorities, and long-term digital transformation strategies.

Because digital twins rely on data-driven simulations and monitoring, their effectiveness is commonly evaluated through metrics such as efficiency, reliability, and process optimization.

They highlight the role of digital twins in optimizing energy use, reducing waste, improving lifecycle efficiency, and supporting environmentally responsible decision-making.