Introduction

eSIM statistics offer a clear snapshot of how embedded subscriber identity module technology is transforming global connectivity by eliminating physical SIM cards and enabling remote, software-driven network activation. The figures indicate growing Adoption across smartphones, wearables, connected vehicles, and large-scale IoT implementations, supported by the need for seamless operator switching, compact device design, and easier connectivity management.

These statistical patterns also reveal variations in Adoption across regions and industries, shaped by factors such as network maturity, regulatory frameworks, and the pace of digital transformation. Collectively, eSIM statistics help measure the shift toward more flexible, efficient, and globally interoperable connectivity models for both consumer and enterprise use cases.

Editor’s Choice

- The number of eSIM-enabled consumer device models expanded nearly tenfold between 2018 and 2023, underscoring the rapid ecosystem maturation.

- Smartphones emerged as the dominant driver of eSIM adoption, with their share of eSIM-enabled consumer devices rising from 29% to 60% over the same period.

- Commercial eSIM smartphone services expanded globally, from 24 countries in 2018 to 120 by 2023.

- The global installed base of eSIM smartphone connections more than quadrupled from 2022 to 2024, reflecting accelerated mainstream Adoption.

- Despite the shift to eSIM-only smartphones, particularly in the US, postpaid and prepaid churn rates remained largely stable within narrow historical ranges.

- Long-term projections indicate eSIM is expected to account for over 75% of global smartphone connections by 2030 under baseline adoption scenarios.

- Asia Pacific is projected to become the largest contributor to global eSIM smartphone connections, accounting for approximately 55% of the global total by 2030.

- Regional penetration patterns point to near universal eSIM adoption in North America and Europe, with penetration approaching 95–98% in mature markets.

- In the cellular IoT domain, eSIM and iSIM together are forecast to represent over 70% of global connections by 2030, significantly reducing reliance on removable SIMs.

- Operator demand insights show that smart cities, healthcare, logistics, and utilities collectively account for more than 50% of anticipated eSIM-enabled IoT demand.

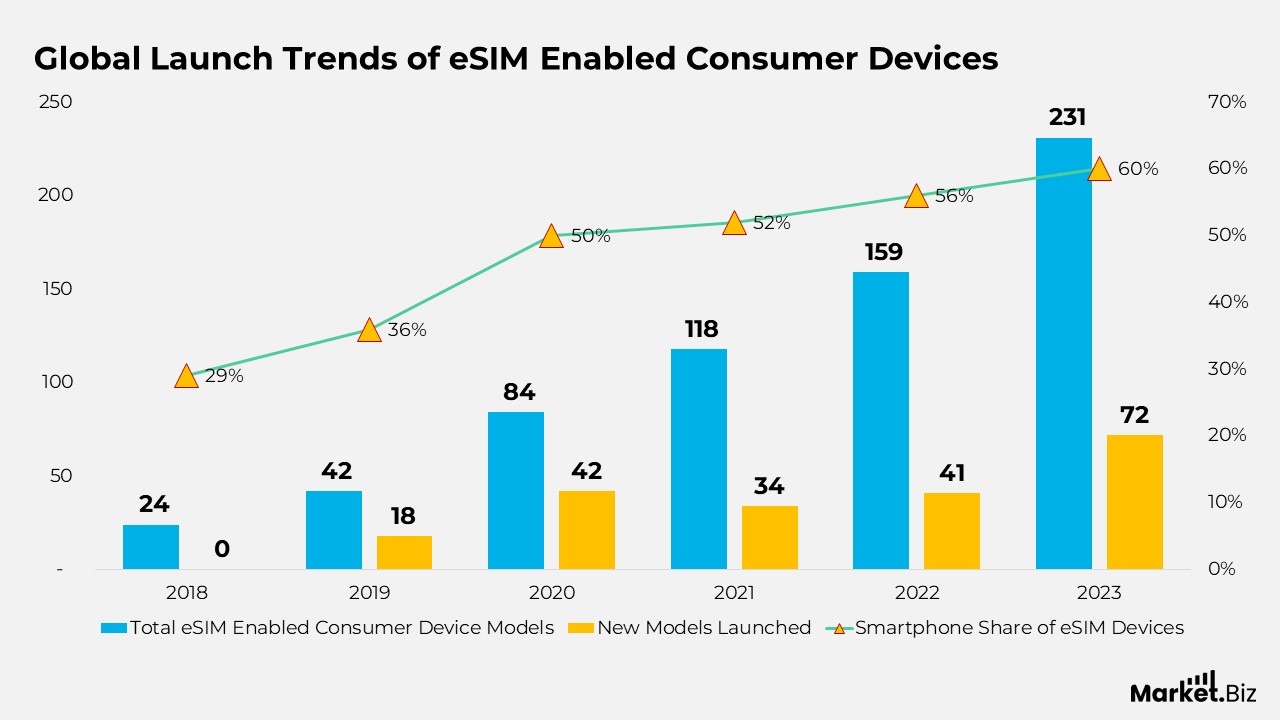

Global Launch Trends of eSIM-Enabled Consumer Devices

- The number of eSIM-enabled consumer device models expanded steadily from 24 in 2018 to 231 by 2023, indicating rapid ecosystem development.

- Smartphone share among total eSIM consumer devices increased steadily, rising from 29% in 2018 to 60% in 2023, underscoring smartphones as the primary driver of Adoption.

- In 2019, the total number of launched models grew to 42, while smartphone penetration reached 36%, reflecting early market acceleration.

- In 2020, the number of launched models jumped to 84, with smartphones accounting for 50% of all eSIM consumer devices.

- By 2021, cumulative launches reached 118 models, alongside a smartphone share of 52%, signalling balanced growth across device categories.

- In 2022, total eSIM consumer device models increased further to 159, while smartphone contribution rose to 56%, reinforcing their market dominance.

- The strongest expansion occurred in 2023, with 72 new models launched in a single year, pushing the cumulative total to 231 and smartphone share to 60%.

- Overall, the data reflects both rapid model proliferation and a structural shift toward smartphones as the leading platform for eSIM adoption.

(Source: GSMA Intelligence)

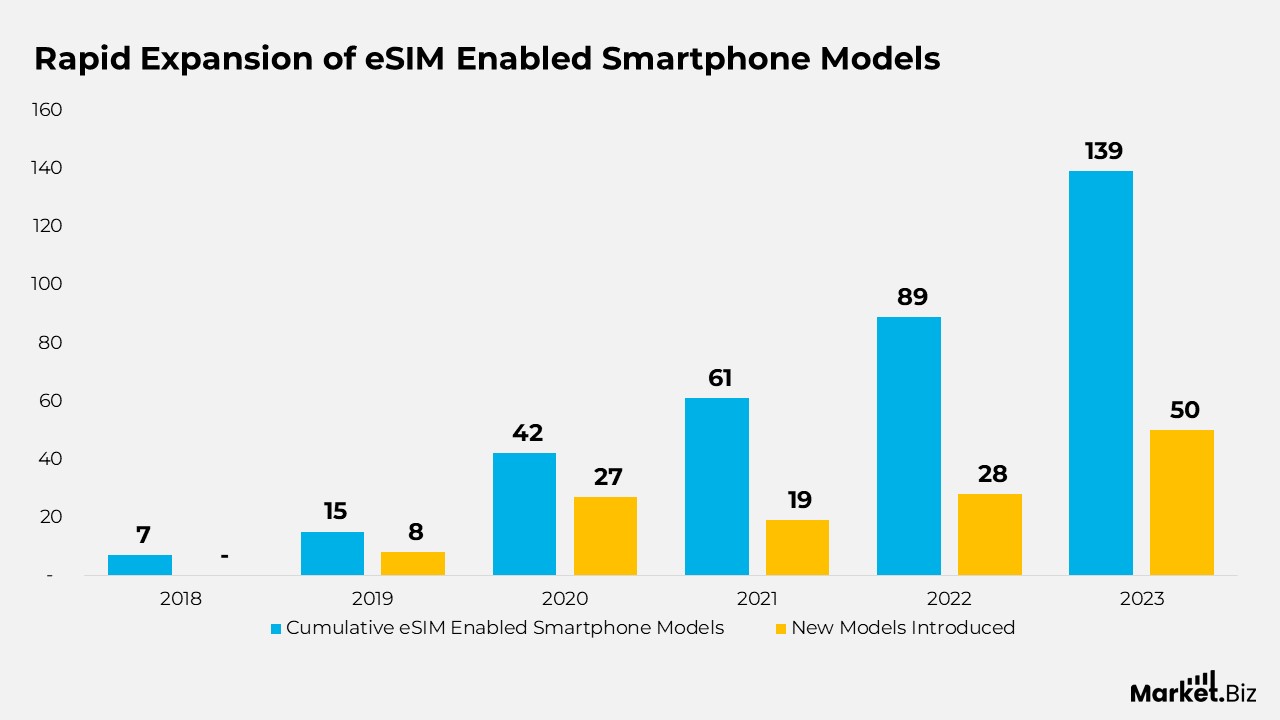

Rapid Expansion of eSIM-Enabled Smartphone Models

- The cumulative number of eSIM-enabled smartphone models increased from 7 in 2018 to 139 by 2023, reflecting strong and sustained market expansion.

- In 2019, commercially available eSIM smartphone models rose to 15, indicating early Adoption by leading device manufacturers.

- In 2020, the number of launched models jumped to 42, marking a clear inflexion point in eSIM smartphone integration.

- By 2021, cumulative launches reached 61 models, supported by wider operator compatibility and improved consumer awareness.

- In 2022, the total number of available eSIM smartphones expanded further to 89, reinforcing eSIM’s transition into mainstream device portfolios.

- The most substantial growth occurred in 2023, when 50 new eSIM smartphone models were introduced, driving the cumulative count to 139.

(Source: GSMA Intelligence)

Global Expansion of Commercial eSIM Smartphone Services

- The number of countries offering commercial eSIM services for smartphones increased from 24 in 2018 to 120 by 2023, reflecting rapid global Adoption.

- In 2019, eSIM smartphone service availability expanded to 45 countries, indicating growing operator readiness beyond early adopter markets.

- By 2020, the count rose further to 69 countries, supported by wider network upgrades and standardized remote SIM provisioning.

- In 2021, commercial eSIM smartphone services were available in 81 countries, marking steady geographic penetration across developed and emerging regions.

- In 2022, coverage expanded to 100 countries, highlighting the accelerated rollout by mobile network operators worldwide.

- By 2023, commercial eSIM services for smartphones were available in 120 countries, underscoring eSIM’s transition to a globally mainstream connectivity standard.

(Source: GSMA Intelligence)

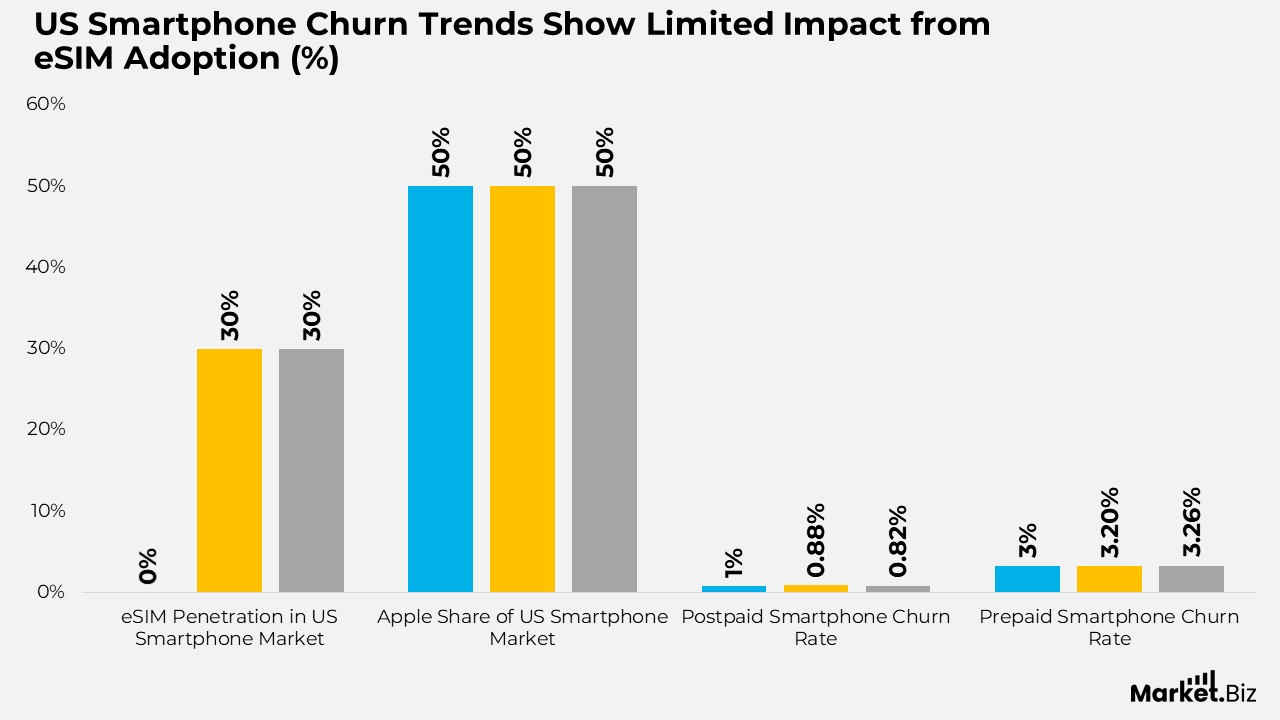

US Smartphone Churn Trends Show Limited Impact from eSIM Adoption

- The US remains the largest eSIM smartphone market globally, with approximately 30% eSIM penetration, driven primarily by strong device and operator support.

- Apple’s launch of eSIM-only iPhones in September 2022, combined with Apple’s nearly 50% share of the US smartphone market, marked a major structural shift in device provisioning.

- Despite this shift, postpaid smartphone churn remained largely stable, moving from around 0.76% in Q3 2020 to 0.88% in Q3 2022, and settling near 0.82% by Q1 2024.

- Prepaid churn also showed limited disruption, fluctuating around 3.24% in Q3 2020, approximately 3.20% at the time of the eSIM-only iPhone launch in Q3 2022, and reaching about 3.26% by Q1 2024.

- No sharp increase or decline in churn levels is visible immediately after the September 2022 introduction of the eSIM-only iPhone.

(Source: GSMA Intelligence)

Rapid Acceleration in Global eSIM SmartphoneConnection Base

- The global installed base of eSIM smartphone connections reached 144 million in 2022, establishing the foundation for rapid expansion.

- In 2023, eSIM smartphone connections more than doubled to 310 million, reflecting strong uptake across new device launches and operator support.

- Growth accelerated further in 2024, with the installed base nearly doubling again to 598 million connections worldwide.

- The consecutive year-on-year doubling highlights increasing consumer acceptance of eSIM-only and dual eSIM smartphones.

- This growth trend underscores the transition of eSIM from an emerging feature to a mainstream smartphone connectivity standard worldwide.

(Source: GSMA Intelligence)

Rising Awareness and Measured Adoption of eSIM in Smartphones

- Global eSIM smartphone adoption is increasing steadily, with consumer awareness rising faster than actual usage across installed smartphone connections.

- Under the baseline scenario, eSIM is projected to account for 76% of global smartphone connections by 2030, equivalent to approximately 6.9 billion connections.

- In a high adoption scenario, eSIM penetration could reach 88% of total smartphone connections by 2030, representing nearly 8.0 billion connections worldwide.

- Even in a low-adoption scenario, eSIM usage is expected to grow to 61% by 2030, translating into around 5.6 billion smartphone connections.

- A key milestone is expected by 2025, when global eSIM smartphone connections are projected to surpass 1 billion.

- By 2028, eSIMs are anticipated to be used in roughly 50% of all smartphone connections globally, marking a major inflexion point in Adoption.

(Source: GSMA Intelligence)

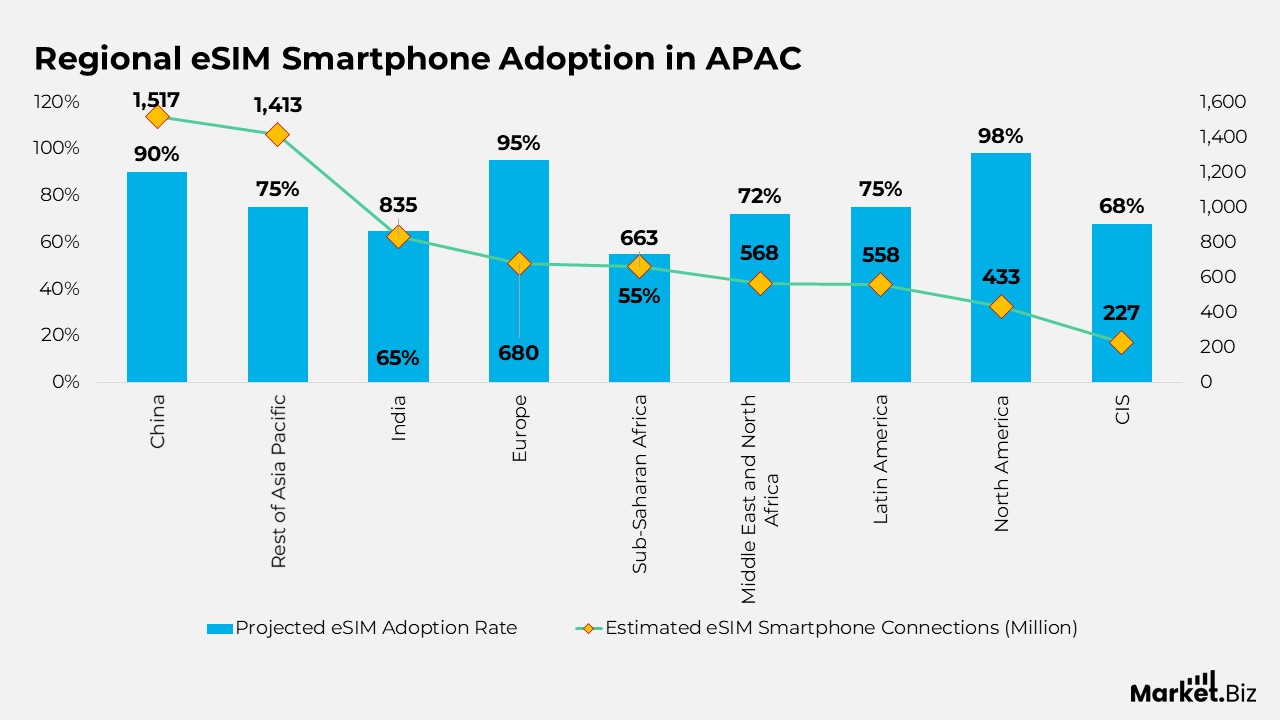

Regional eSIM Smartphone Adoption in APAC

- Asia Pacific is projected to lead global eSIM smartphone adoption by 2030, driven by large installed bases and accelerating digital connectivity.

- China is expected to reach around 90% eSIM adoption, with approximately 1,517 million eSIM smartphone connections, making it the single largest national market.

- The rest of Asia Pacific is projected to achieve about 75% adoption, accounting for nearly 1,413 million eSIM smartphone connections by 2030.

- India is anticipated to reach roughly 65% eSIM adoption, supported by an estimated 835 million eSIM smartphone connections as network readiness improves.

- Europe is forecast to record one of the highest adoption rates globally at around 95%, translating to approximately 680 million eSIM smartphone connections.

- Sub-Saharan Africa is projected to reach about 55% adoption, with nearly 663 million eSIM smartphone connections, reflecting gradual but steady uptake.

- The Middle East and North Africa region is expected to achieve around 72% adoption, supported by approximately 568 million eSIM smartphone connections.

- Latin America is projected to reach close to 75% adoption, accounting for about 558 million eSIM smartphone connections by 2030.

- North America is expected to show near-universal Adoption at approximately 98%, with around 433 million eSIM smartphone connections.

- The CIS region is forecast to reach about 68% adoption, corresponding to roughly 227 million eSIM smartphone connections.

(Source: GSMA Intelligence)

eSIM Penetration Across Asia Pacific Markets

- Asia Pacific is projected to play an increasingly influential role in shaping global eSIM smartphone adoption over the remainder of the decade.

- Regional eSIM penetration in Asia Pacific is estimated at 2% in 2023, indicating an early stage of Adoption across the installed smartphone base.

- Adoption is expected to rise steadily to 5% in 2024 and 9% in 2025, supported by expanding device availability and operator readiness.

- By 2026, eSIM penetration in the region is projected to reach 16%, marking the beginning of accelerated uptake.

- Growth intensifies from 2027 onward, with penetration increasing to 31% in 2027, 47% in 2028, and 63% in 2029.

- By 2030, eSIM penetration in the Asia Pacific is forecast to reach approximately 78% of total smartphone connections.

- Asia Pacific’s share of global eSIM smartphone connections is expected to increase from around 24% in 2023 to approximately 55% by 2030.

(Source: GSMA Intelligence)

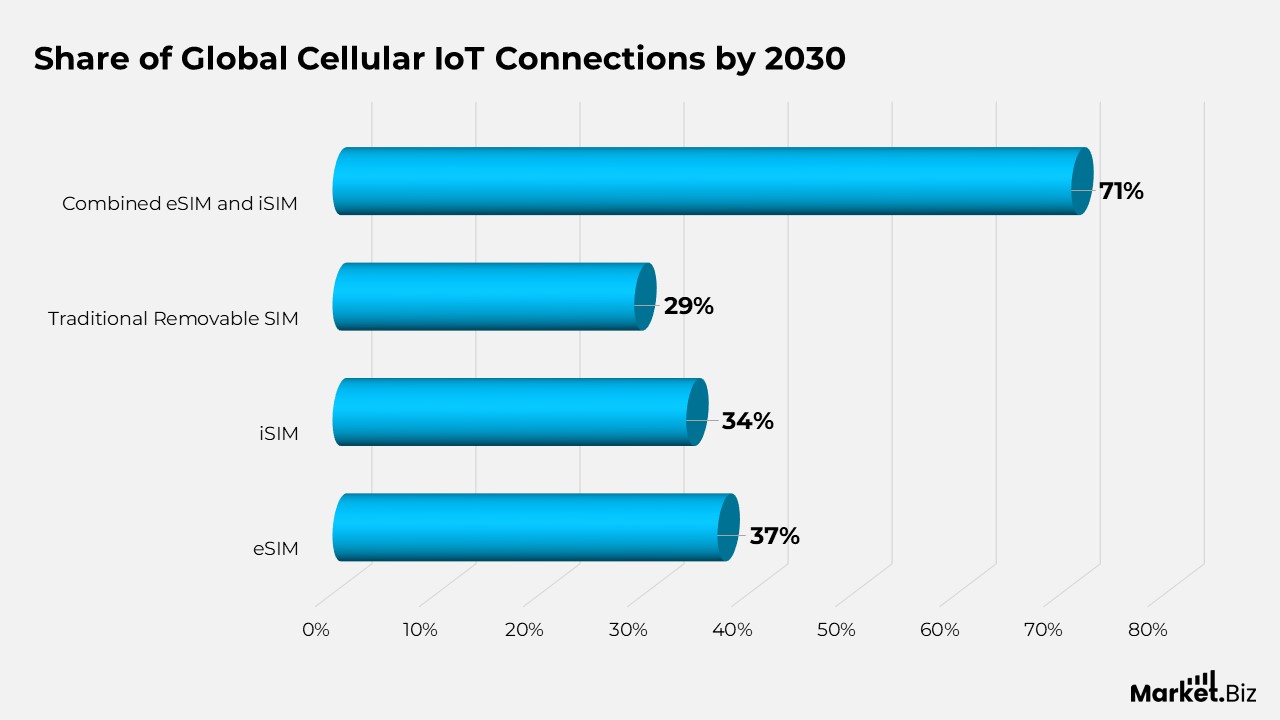

eSIM and iSIM Adoption Trends in the Global Cellular IoT Market Statistics

- By 2030, mobile network operators expect eSIM and iSIM technologies to capture a dominant share of global cellular IoT connections.

- Operator surveys indicate that eSIM is projected to account for approximately 37% of total cellular IoT connections worldwide by 2030.

- iSIM is expected to account for around 34% of global cellular IoT connections during the same timeframe.

- Traditional removable SIM cards are forecast to decline to about 29% of cellular IoT connections by 2030, as embedded solutions gain traction.

- Combined, eSIM and iSIM are expected to account for roughly 71% of the global cellular IoT market by 2030.

(Source: GSMA Intelligence)

Operator Demand for eSIM-Enabled Solutions by Industry

- During 2024–2025, mobile network operators expect demand for eSIM-enabled solutions to be led by smart city applications, accounting for roughly 18–20% of total anticipated eSIM IoT demand globally.

- The healthcare sector represents the second-largest demand cluster, at approximately 14–15%, driven by connected medical devices, remote diagnostics, and patient monitoring systems.

- Media and broadcasting use cases are expected to contribute around 12–13% of operator demand, supported by mobile production, live streaming, and content delivery infrastructure.

- Agriculture is projected to account for nearly 11–12% of demand, reflecting the growing Adoption of precision farming, smart irrigation, and livestock monitoring solutions.

- Retail applications are expected to account for about 10–11%, supported by connected point-of-sale systems, inventory tracking, and in-store analytics.

- Shipping and logistics are forecast to generate approximately 9–10% of demand, driven by fleet management, container tracking, and cross-border connectivity needs.

- Utilities and energy applications are expected to contribute close to 8–9%, mainly from smart metering and grid monitoring deployments.

- Home security and automotive use cases together are projected to represent around 7–8%, supported by connected alarms, telematics, and mobility services.

- Industrial applications are estimated to account for roughly 5–6%, reflecting longer upgrade cycles and selective eSIM integration.

- Aircraft-related use cases account for the smallest share, at approximately 3–4%, constrained by regulatory requirements and slower fleet modernisation timelines.

(Source: GSMA Intelligence)

Rapid Global Scale Up of Private Wireless Network Deployments

- Deployment of private wireless networks based on 4G and 5G technologies has accelerated significantly over the past few years.

- The number of unique organizations and government entities operating private wireless networks increased from approximately 500 in 2020 to around 1,400 by 2023, reflecting expanding enterprise and public sector adoption.

- Geographic coverage also broadened substantially, with private wireless networks present in roughly 40 countries in 2020.

- By 2023, the number of countries with active private wireless network deployments doubled to approximately 80, indicating rapid international expansion.

- Overall, the data highlights strong momentum in private wireless Adoption, driven by demand for secure, high-reliability connectivity across industrial, public safety, and enterprise use cases.

(Source: GSMA Intelligence)

Conclusion

eSIM statistics clearly illustrate a fundamental shift in the way connectivity is delivered and managed across consumer, enterprise, and IoT environments. The consistent increase in eSIM-enabled smartphones, the expanding global availability of eSIM services, and the rapid growth in installed connections indicate that eSIM is progressing from an emerging capability to a widely adopted standard. Regional trends further show that while North America and Europe are nearing saturation, the Asia Pacific is becoming the main contributor to global eSIM growth in absolute terms.

Operator-level data suggests that eSIM adoption has a neutral impact on subscriber churn, while delivering significant advantages in provisioning efficiency, operational flexibility, and international scalability. In parallel, the rising Adoption of eSIM and iSIM in cellular IoT, supported by strong demand from smart cities, healthcare, logistics, utilities, and industrial applications, underscores the long-term relevance of embedded connectivity.

Overall, the statistical evidence points to a steady and irreversible transition toward software-driven connectivity models. As device penetration increases, network ecosystems mature, and enterprise deployments scale, eSIM is expected to evolve into the default connectivity framework across smartphones and connected devices, shaping the future of global digital communication infrastructure.

FAQ’s

eSIM statistics are employed to study the Adoption and diffusion of embedded connectivity technologies within modern digital ecosystems. They offer a quantitative lens through which the transition from physical SIM cards to software-defined identity modules can be understood, reflecting broader trends in network virtualization, device convergence, and digital mobility.

From a theoretical standpoint, eSIM statistics mirror a typical technology diffusion lifecycle, progressing from initial experimentation toward widespread Adoption. Increasing penetration levels and expanding installed bases demonstrate how embedded technologies scale once standardization, ecosystem coordination, and economic efficiencies are established.

Smartphones serve as foundational reference devices in eSIM statistical models due to their large shipment volumes, rapid replacement cycles, and significant influence on user behavior. Their early Adoption reinforces network effects, stimulates operator investment, and facilitates broader compatibility across other connected device categories.

Differences in regional eSIM adoption can be attributed to variations in regulatory frameworks, network infrastructure maturity, consumer awareness, and levels of industrial digitalization. While developed markets typically exhibit faster penetration, high population regions contribute substantially to global growth once infrastructure and policy constraints ease.

Churn-related statistics indicate that technological capability alone does not directly drive changes in consumer behavior. From a behavioral economics perspective, switching decisions remain primarily influenced by perceived value, service quality, and pricing structures rather than the technical simplicity of changing network credentials enabled by eSIM.