Introduction

Champagne Statistics: Champagne, a symbol of elegance and sophistication, represents sparkling wine produced solely in the Champagne region of France. Shaped by elements such as soil, climate, and grape varieties, Chardonnay, Pinot Noir, and Pinot Meunier, it reflects the region’s distinctive terroir.

Utilising the traditional méthode champenoise, Champagne experiences secondary fermentation within the bottle, resulting in its signature bubbles. It is categorized by sweetness levels, ranging from the bone-dry Brut Nature to the sweeter Doux, providing a variety of styles to cater to different tastes.

Whether savored as a non-vintage blend or a distinguished cuvée, Champagne enchants with its grace and complexity. Ideally served chilled in slender flutes, it complements a wide array of dishes.

Although its influence is felt worldwide, only wines produced in the Champagne region are permitted to carry its name. Grasping these fundamentals enhances one’s appreciation for the enduring charm of Champagne.

The global champagne market is propelled by luxury demand, premiumization, and its reputation as a top-tier celebratory beverage. Predominantly led by Europe, which accounts for the majority of both consumption and production, the industry is transitioning towards sustainable practices, with over 90% of production overseen by more than 16,000 growers, while key exports are dominated by major houses.

Editor’s Choice

- The global champagne market has shown consistent revenue growth from 2022 to 2032, with a compound annual growth rate (CAGR) of 6.2%.

- In 2023, the global revenue of the champagne market was estimated at USD 7.2 billion.

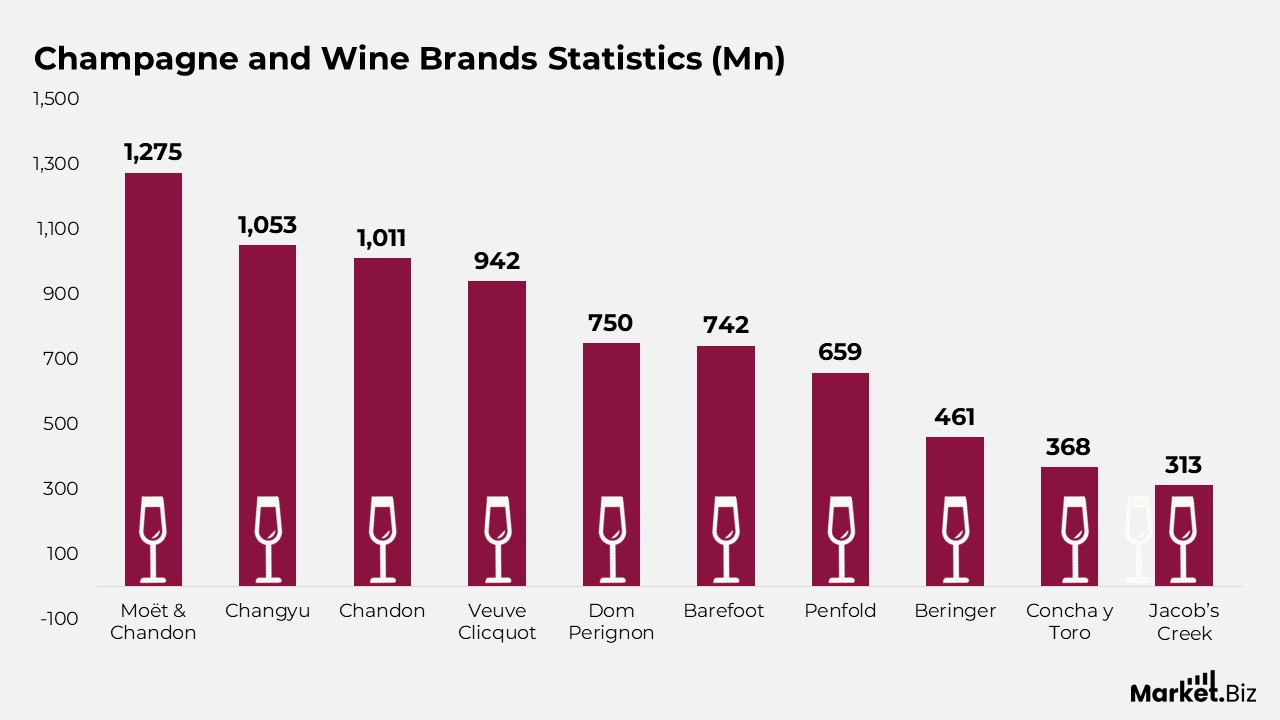

- Moët & Chandon, esteemed at $1,275 million, underscoring its prominent position in the industry.

- France took the lead with a remarkable consumption of 138.3 million bottles, highlighting its cultural connection to champagne.

- China ranks as the second-largest exporter, with a notable shipment volume of 52,119 units.

General Champagne Statistics

- In 2023, the global revenue of the champagne market was estimated at USD 7.2 billion.

- In that year, all categories experienced growth: Prestige Cuvee (USD 1.90 billion), Blanc de Noirs (USD 1.67 billion), Brut Champagne (USD 0.61 billion), Demi-Sec (USD 1.44 billion), Rosé Champagne (USD 0.84 billion), and Blanc de Blancs (USD 1.14 billion).

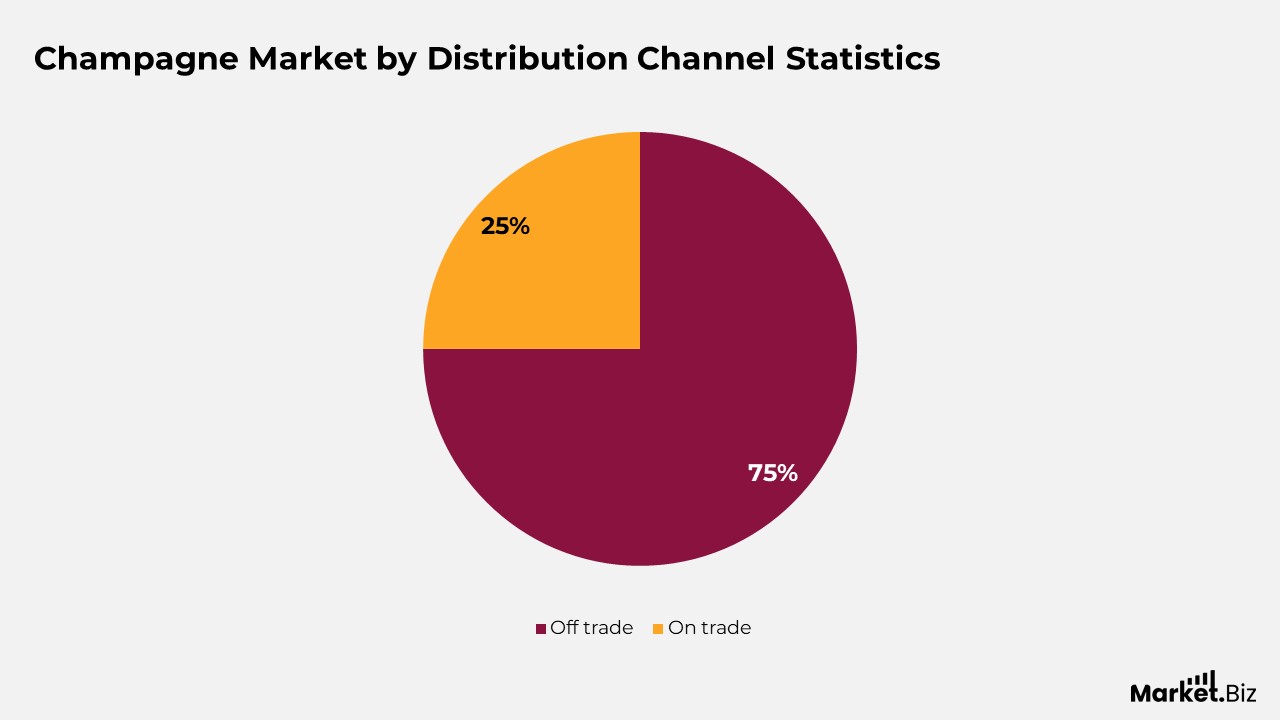

- The off-trade channel maintains a leading role, representing 75% of the market share.

- Moët & Chandon topped the brand rankings in 2023, valued at $1,275 million, which highlights its prominent position in the industry.

- France was at the forefront with a remarkable consumption of 138.3 million bottles in 2022, emphasising its cultural connection to champagne.

- Luxembourg ranked highest in per capita spending on champagne at €14.7, reflecting its elevated standard of living and luxury consumption patterns.

- In 2022, the United States was the leading nation for champagne imports, bringing in 34.1 million bottles valued at around 793.5 million EUR.

Champagne Market Size Statistics

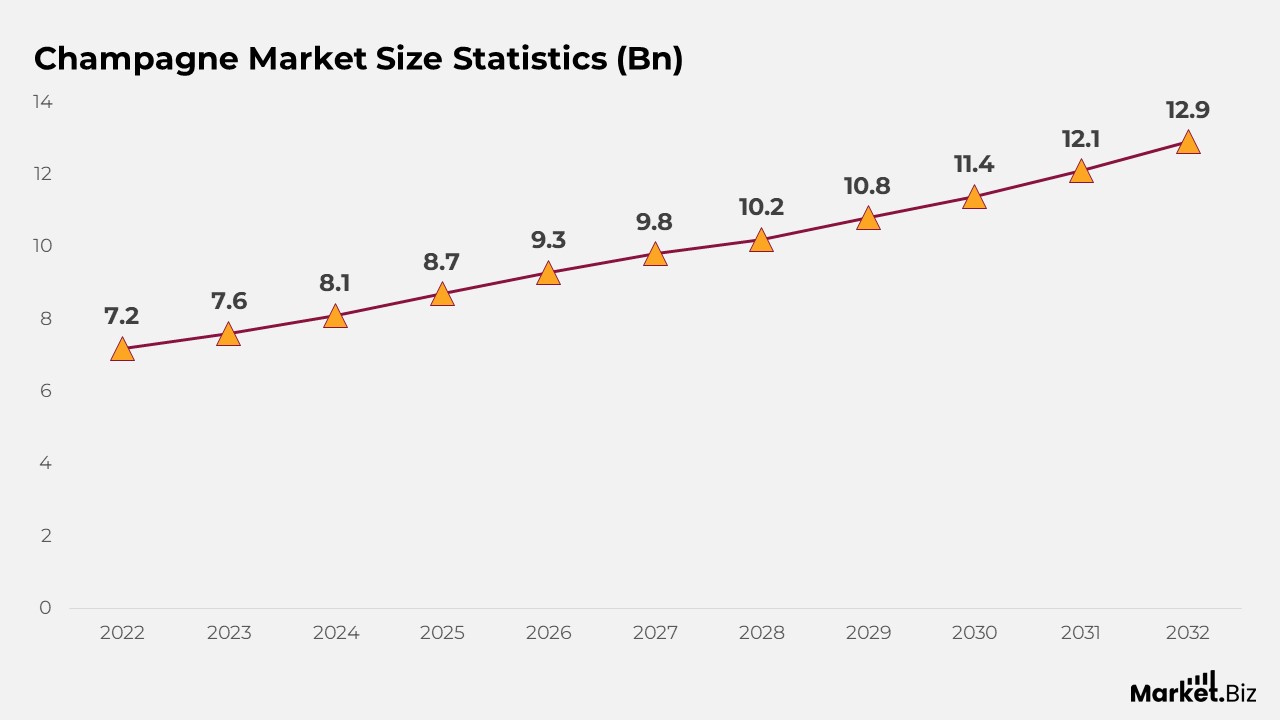

- The global champagne market has shown consistent revenue growth from 2022 to 2032, with a compound annual growth rate (CAGR) of 6.2%.

- In 2022, the market was valued at USD 7.2 billion, and it has gradually risen to USD 7.6 billion in 2023.

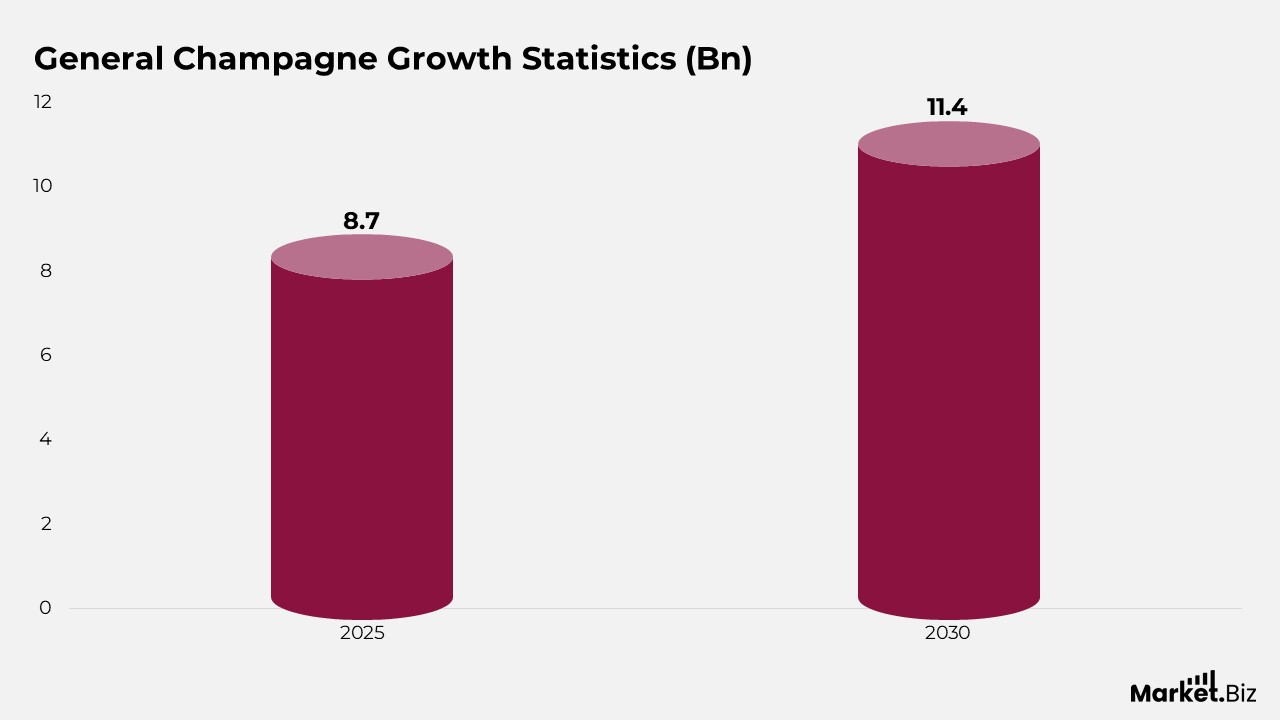

- The growth trend is expected to persist, with market revenue projected to reach USD 8.1 billion in 2024, USD 8.7 billion in 2025, and USD 9.3 billion by 2026.

- As the market evolves, a further increase is anticipated, with estimates of USD 9.8 billion in 2027, USD 10.2 billion in 2028, and USD 10.8 billion in 2029.

- By the end of the decade, the market is forecasted to rise to USD 11.4 billion in 2030, followed by a significant increase to USD 12.1 billion in 2031, culminating at USD 12.9 billion by 2032.

Champagne Market by Distribution Channel Statistics

- The off-trade channel occupies a leading role, representing 75% of the market share. This segment comprises sales made through retail establishments such as supermarkets, liquor stores, and various other retail locations where consumers buy champagne for personal consumption away from the premises.

- Conversely, the on-trade channel, which includes establishments like restaurants, bars, and clubs where champagne is enjoyed on-site, accounts for 25% of the market.

Statistics of Champagne and Wine Brands

- In 2023, the global market for champagne and still wine was significantly influenced by several leading brands, each recognized for its brand value in millions of U.S. dollars.

- At the top of the rankings was Moët & Chandon, esteemed at $1,275 million, underscoring its prominent position in the industry.

- Following closely was Changyu, a notable brand with a valuation of $1,053 million, and Chandon, which possessed a brand value of $1,011 million.

- Veuve Clicquot also made a significant impact, with a valuation of $942 million. Dom Perignon, celebrated for its luxury products, was valued at $750 million.

- Barefoot followed with a value of $742 million, closely trailed by Penfold’s at $659 million.

- Beringer, with a brand worth of $461 million, and Concha y Toro, at $368 million.

- Jacob’s Creek, at $313 million.

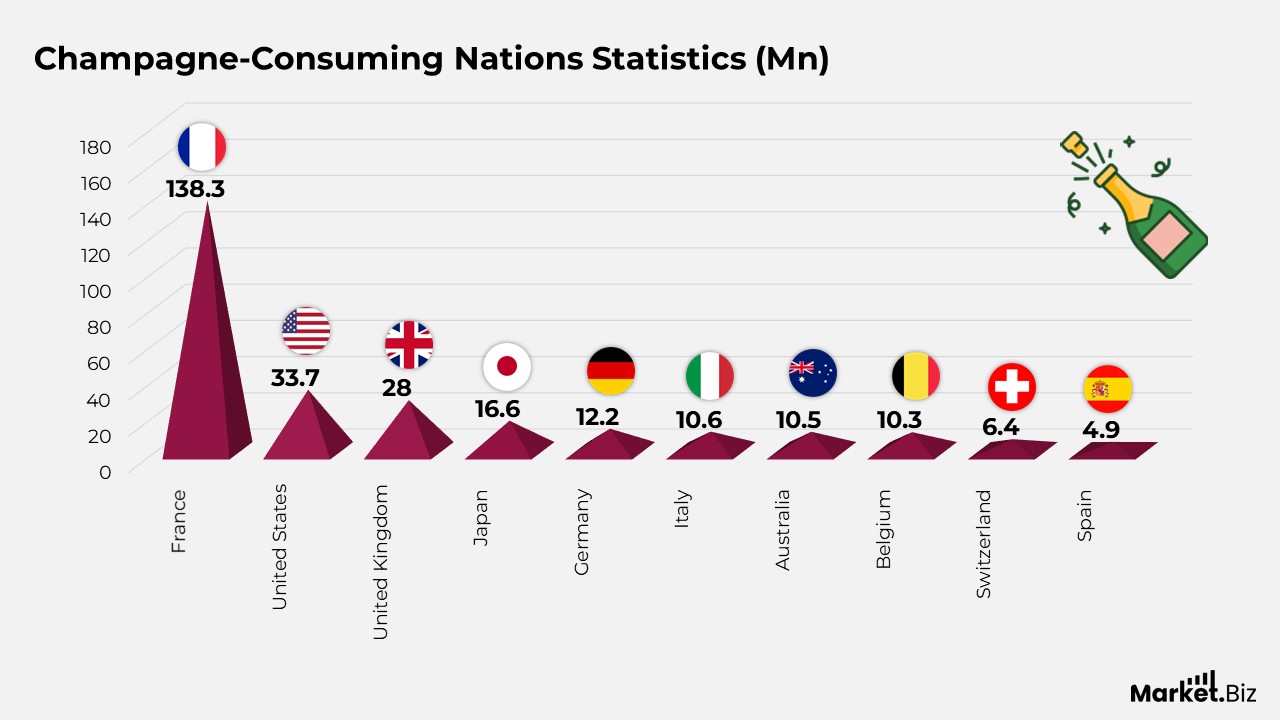

Champagne-Consuming Nations Statistics

- France took the lead with a remarkable consumption of 138.3 million bottles, highlighting its cultural connection to champagne.

- The United States came in a distant second, with 33.7 million bottles consumed, which reflects its vast market size and trends in luxury consumption.

- Following closely was the United Kingdom, with 28 million bottles consumed, demonstrating its enduring appreciation for champagne.

- Japan also exhibited significant consumption at 16.6 million bottles, while Germany followed with 12.2 million bottles, indicating a robust market presence in these economies.

- Italy and Australia were fierce competitors in the champagne market, with consumption figures of 10.6 million and 10.5 million bottles, respectively. Belgium also showed a strong demand with 10.3 million bottles.

- Finally, Switzerland and Spain completed the list with 6.4 million and 4.9 million bottles, respectively, showcasing their niche yet significant markets for champagne.

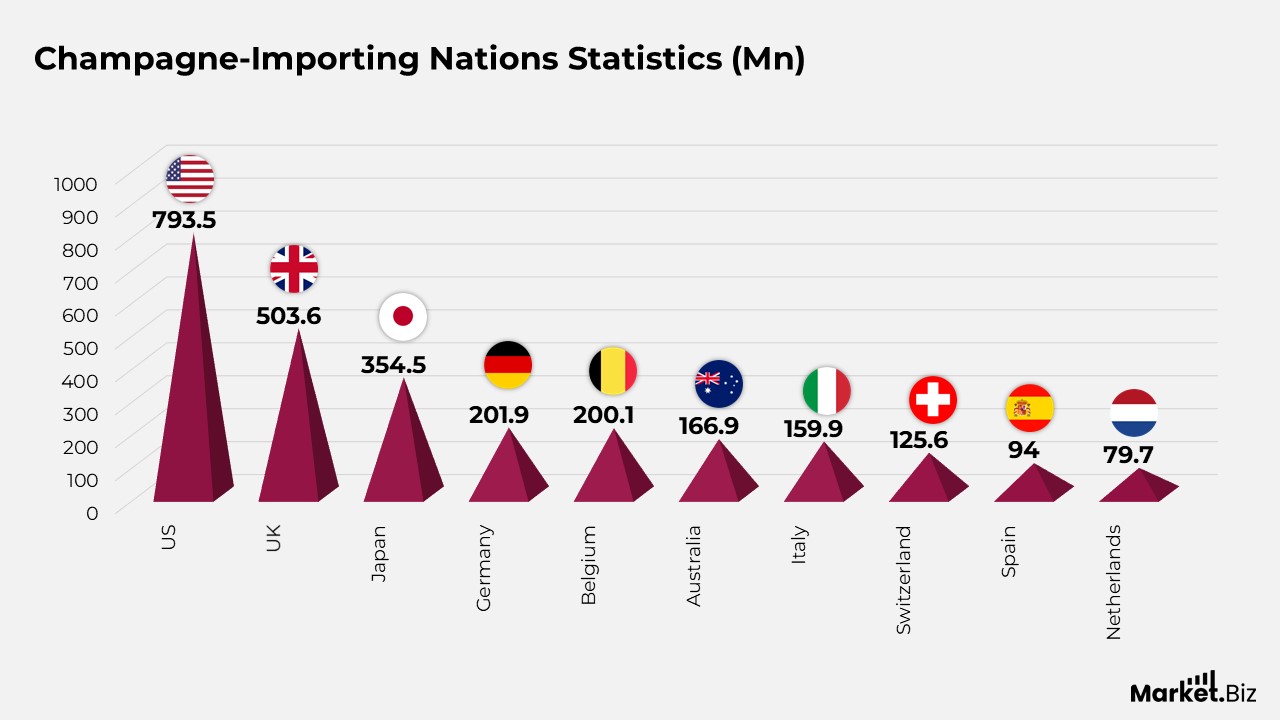

Statistics of Champagne Importing Nations

- In 2022, the United States topped the list of countries importing champagne, with an impressive total of 34.1 million bottles valued at around 793.5 million EUR, establishing it as the leading spender on champagne imports.

- The United Kingdom closely followed, bringing in 29.9 million bottles with a cumulative value of 503.6 million EUR.

- Japan also played a significant role as an importer, with 13.8 million bottles traded in at a cost of 354.5mn EUR.

- Belgium and Germany completed the top five, importing 10.3 and 11.1 million bottles valued at 200.1 million EUR and 201.9 million EUR, respectively.

- Additionally, Australia, Italy, and Switzerland were noteworthy importers, with import volumes of 9.9, 9.2, and 6.1 million bottles and corresponding values of 166.9 million EUR, 159.9 million EUR, and 125.6 million EUR, respectively.

- Finally, Spain and the Netherlands rounded out the top ten, importing 4.4 million bottles (94 million EUR) and 3.9 million bottles (79.7 million EUR), respectively.

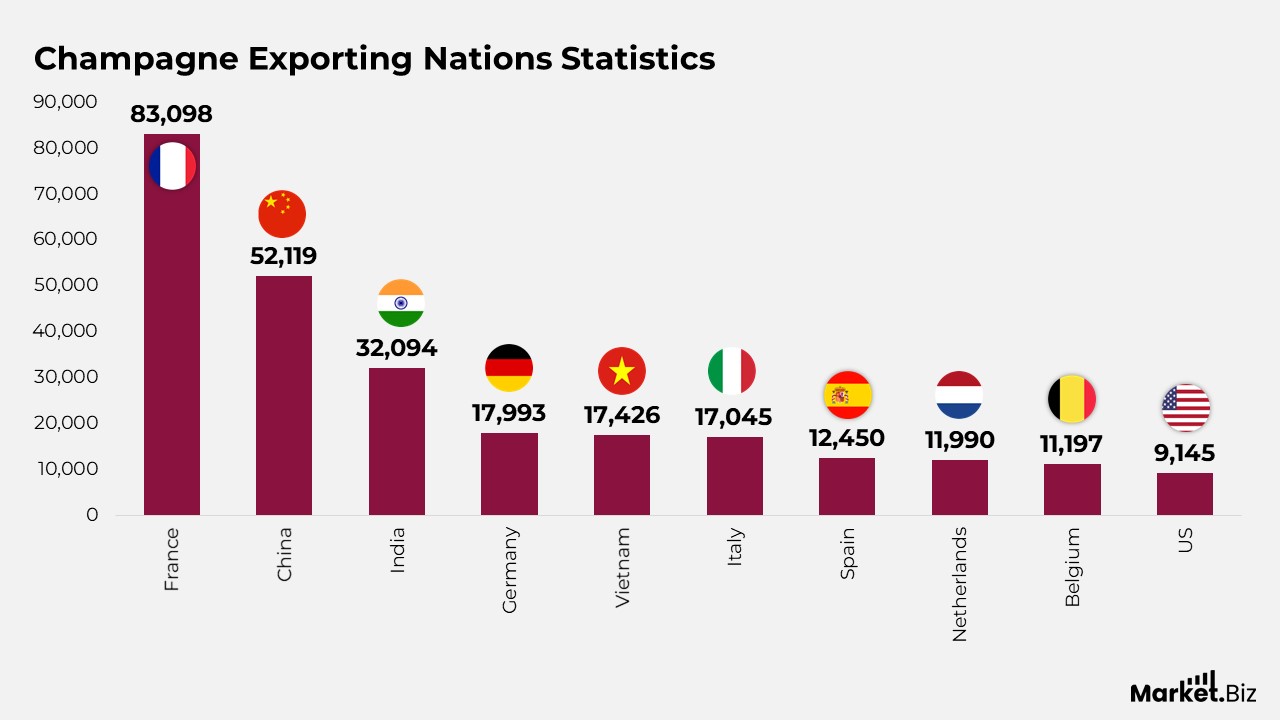

Champagne Exporting Nations Statistics

- In the realm of champagne exports, France is distinguished as the foremost exporter, boasting a considerable shipment volume of 83,098 units, thereby underscoring its preeminent position in the global champagne sector.

- China ranks as the second-largest exporter, with a notable shipment volume of 52,119 units. India occupies the third position, contributing 32,094 units to the worldwide champagne market.

- Germany and Vietnam also emerge as significant exporters, with shipments of 17,993 and 17,426 units, respectively. Italy closely follows with an export volume of 17,045 units.

- The list extends to include Belgium, the Netherlands, and Spain, which exported 11,197, 11,990, and 12,450 units, respectively.

- The United States completes the top ten, having exported 9,145 units of champagne.

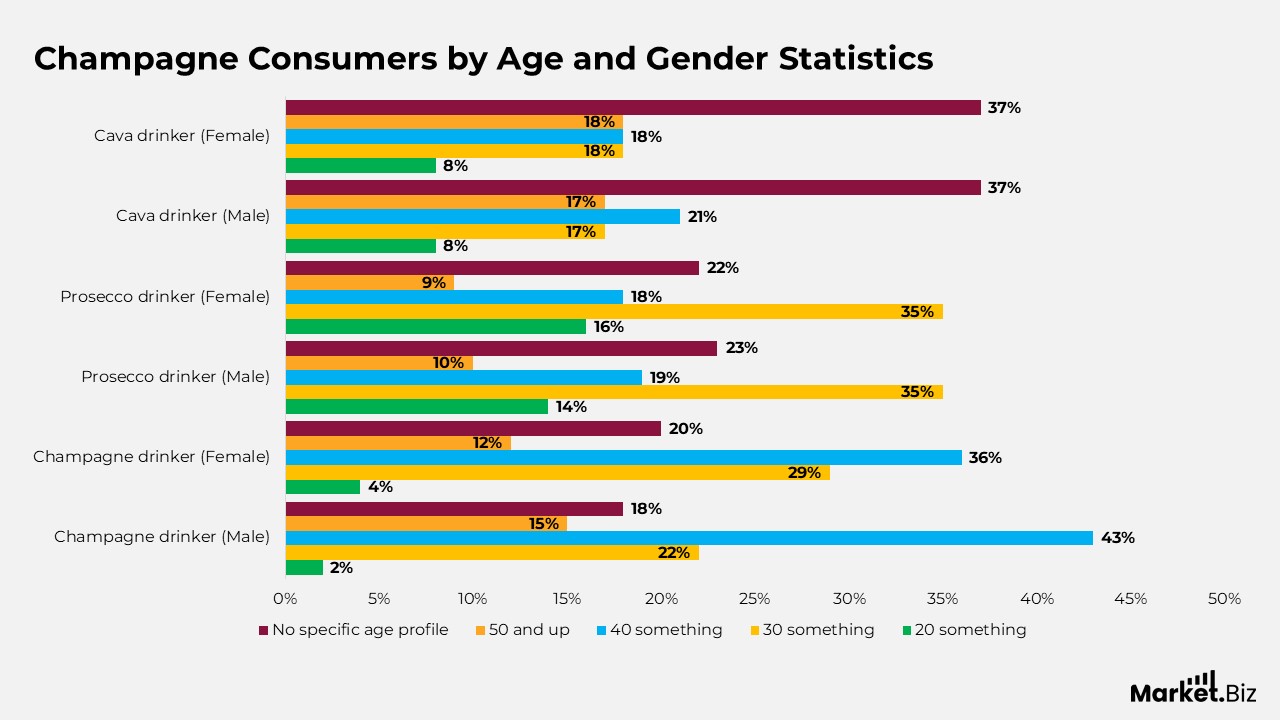

Champagne Consumers by Age and Gender Statistics

- In the realm of Champagne consumption, the majority of male drinkers are primarily in their 40s, accounting for 43% of the demographic.

- This is followed by those in their 30s, who represent 22%, and individuals aged 50 and above, making up 15% of the total.

- Only 2% of male Champagne consumers are in their twenties, whereas 18% do not fit into a defined age group.

- On the other hand, female Champagne drinkers exhibit a higher concentration in their 30s, at 29%, and 36% in their 40s, with a smaller proportion of 12% in the 50 and older bracket. Approximately 4% belong to the 20s age group, and 20% lack a defined age profile.

- Prosecco drinkers tend to be younger, particularly among females, with 16% in their 20s and 35% in their 30s. Male Prosecco drinkers reflect a similar trend, with 14% in their 20s and 35% in their 30s.

- However, the representation in older age groups diminishes significantly, with only 10% of males and 9% of females over the age of 50. two genders exhibit around 22-23% of consumers who do not fit into a specific age category.

- Cava consumers display a more balanced age distribution, especially among females, with 8% in their 20s, 18% in their 30s, 18% in their 40s, and 18% aged 50 and older. Males, however, show slightly less uniformity, with 8% in their 20s, 17% in their 30s, 21% in their 40s, and 17% over 50.

- It is noteworthy that both male and female Cava drinkers have a significant percentage, 37%, who do not adhere to a specific age profile, indicating a wide-ranging appeal across various age demographics.

Recent Statistics

- The M&A landscape in 2024 is defined by strategic consolidations and substantial investments. For example, significant acquisitions in related fields such as life sciences have occurred, including Novo Holdings’ acquisition of Catalent, Inc. for $16.5 billion, with the goal of improving health and sustainability outcomes.

- The champagne market in 2024 is characterized by strategies focused on simplifying business models, heightened cross-border M&A activity, and an emphasis on value creation.

Conclusion

In summary, Champagne is characterised not only by its geographic and production exclusivity but also by rigorous international regulations that safeguard its quality and authenticity. Only sparkling wine produced in France’s Champagne region is permitted to bear this name, thereby ensuring the preservation of its integrity and heritage.

This worldwide acknowledgement reinforces its luxury status and substantial economic impact, especially through exports. As markets change, the Champagne industry’s commitment to upholding high standards of quality and authenticity remains essential for its lasting prestige and success.

FAQs

Champagne refers to a specific type of sparkling wine that is crafted from grapes cultivated in the Champagne region of France, adhering to the regulations of the appellation that stipulate particular vineyard practices. This involves sourcing grapes from designated areas within Champagne and conducting a secondary fermentation in the bottle to produce carbonation.

The primary varieties consist of Non-Vintage, a blend of grapes from various years, Vintage (produced from grapes harvested in a single year), Blanc de Noirs (crafted from black grapes), Blanc de Blancs, made from white grapes, and Rosé Champagne (which can be created by blending red and white wines or by macerating the juice with the grape skins).

Champagne is ideally served chilled, generally at a temperature range of 8°C to 10°C (46°F to 50°F). It is recommended to pour it into a tall, narrow glass, such as a flute or tulip, to fully appreciate its bubbles and aroma.