Introduction

Supply chain cybersecurity statistics provide a data-driven foundation for understanding how cyber risks propagate across interconnected suppliers, vendors, logistics providers, and technology partners, especially as modern supply chains increasingly rely on cloud platforms, third-party software, IoT-enabled logistics, and shared data environments.

These statistics highlight the growing shift from direct enterprise attacks to indirect compromises through vendors, managed service providers, and software dependencies, revealing how a single weak link can trigger widespread operational disruption, data exposure, and financial loss.

For decision makers, supply chain cybersecurity metrics on breach frequency, attack vectors, downtime, and economic impact support risk prioritization, investment planning, and regulatory compliance, ultimately serving as a critical benchmark for evaluating cyber resilience and strengthening long-term supply chain security strategies in an increasingly interconnected digital economy.

Editor’s Choice

- A strong majority of organizations report heightened anxiety about supply chain cybersecurity, with nearly 88% of respondents indicating they are either highly or moderately concerned about the associated risks.

- Third-party exposure continues to rise, with over 70% of enterprises acknowledging at least one significant cybersecurity incident linked to an external partner in the past year, while around 5% report more than 10 such incidents.

- End-to-end visibility remains limited, with fewer than 50% of organizations able to actively monitor cybersecurity posture across even half of their extended third-party supplier networks.

- Incident readiness remains largely reactive, as only 26% of organizations embed formal incident response processes into their third-party risk management programs, instead relying heavily on periodic vendor assessments or cyber insurance coverage.

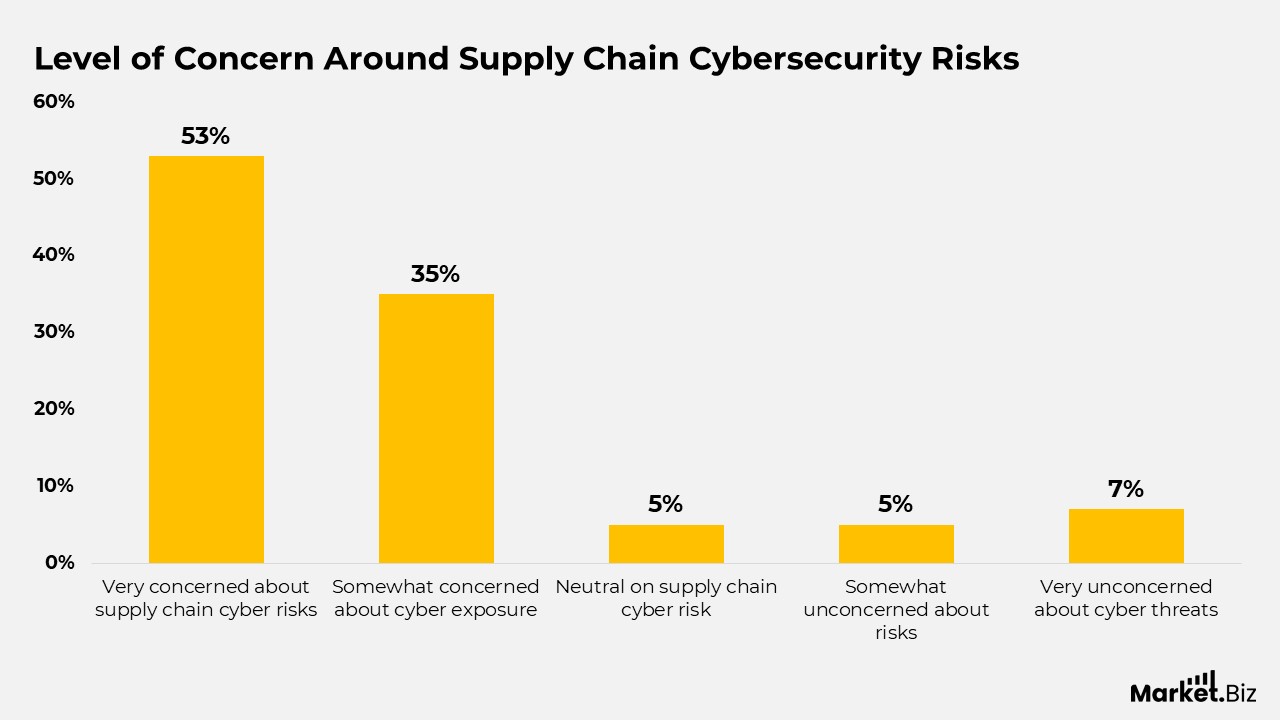

Level of Concern Around Supply Chain Cybersecurity Risks

- A clear majority of respondents demonstrate high risk awareness, with 53% indicating they are very concerned about supply chain-related cybersecurity threats.

- A substantial portion of organizations, accounting for 35%, report being somewhat concerned, reflecting widespread recognition of supply chain vulnerabilities even if not viewed as critical.

- Neutral sentiment remains limited, with only 5% of respondents expressing neither concern nor comfort about supply chain cyber risks.

- Low concern levels are relatively uncommon, with 5% describing themselves as somewhat unconcerned, suggesting minimal complacency across the ecosystem.

- A slightly higher share, 7%, reports being very unconcerned, representing a small minority that may underestimate supply chain cyber exposure.

(Source: Security Score Card, Supply Chain Cybersecurity Trends Report)

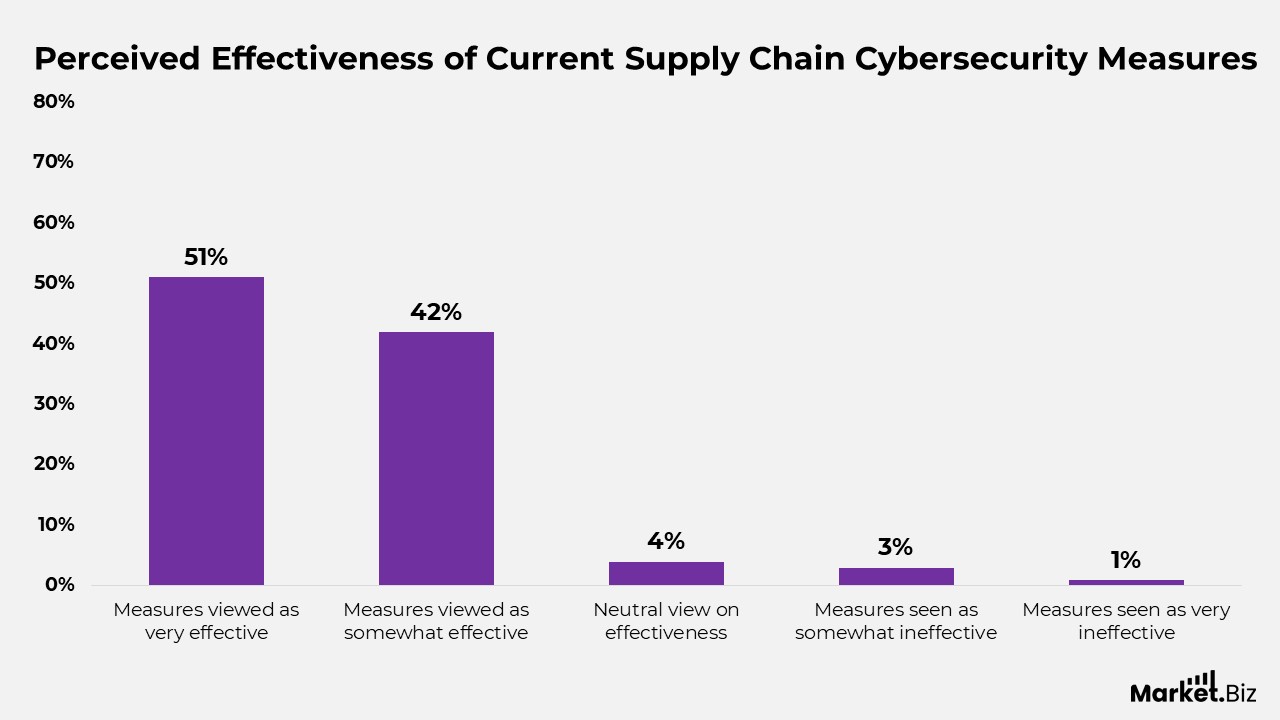

Perceived Effectiveness of Current Supply Chain Cybersecurity Measures

- A majority of organizations express strong confidence in their defenses. With 51% rating their supply chain cybersecurity measures as very effective.

- A significant share, representing 42% of respondents, considers their current controls to be somewhat effective. Indicating moderate confidence but room for improvement.

- Neutral perceptions remain limited, as only 4% of organizations neither endorse nor criticize the effectiveness of their supply chain cybersecurity posture.

- Signs of weakness persist at the margins, with 3% of respondents describing their measures as somewhat ineffective, highlighting localized control gaps.

- Very low confidence is rare, as just 1% of organizations believe their supply chain cybersecurity measures are very ineffective, suggesting minimal widespread failure.

(Source: Security Score Card, Supply Chain Cybersecurity Trends Report)

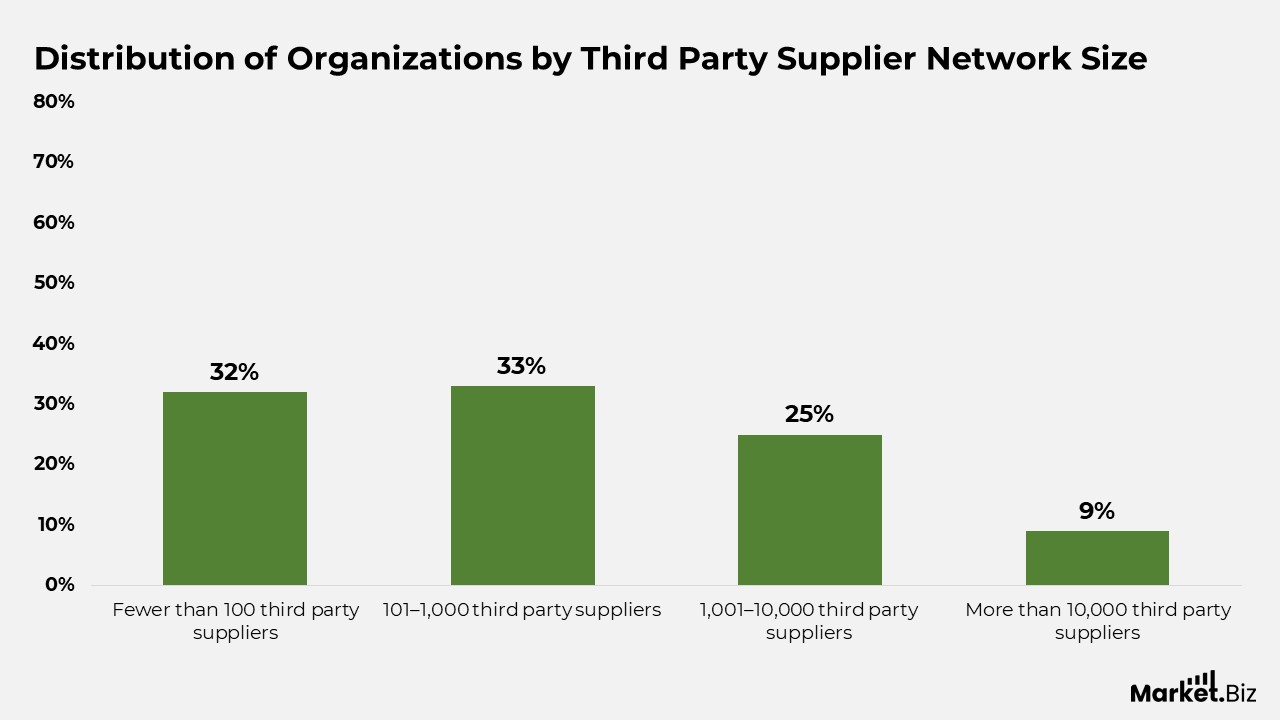

Distribution of Organizations by Third-Party Supplier Network Size

- Smaller supplier ecosystems remain common, with 32% of organizations managing fewer than 100 third-party suppliers.

- Mid-sized supply networks account for the largest share, with 33% of respondents reporting working with 101–1,000 external suppliers.

- Larger supplier portfolios continue to pose complexity challenges, with 25% of organizations overseeing 1,001–10,000 third-party relationships.

- Highly extended supply chains are less common but still notable. As 9% of organisations report reliance on more than 10,000 third-party suppliers.

(Source: Security Score Card, Supply Chain Cybersecurity Trends Report)

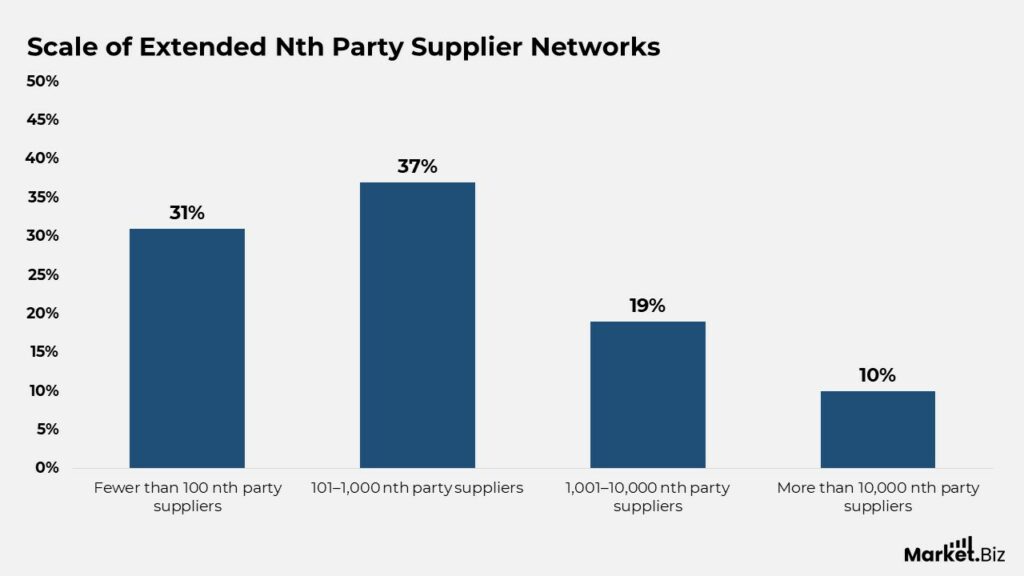

Scale of Extended Nth Party Supplier Networks

- A significant portion of organizations maintain relatively limited extended networks, with 31% reporting fewer than 100 nth party suppliers.

- Moderate complexity dominates the landscape, as 37% of respondents indicate their third-party exposure falls within the 101-1,000 supplier range.

- Larger, multi-tier dependency structures are evident among 19% of organisations managing between 1,001 and 10,000 third-party suppliers.

- Extremely large and highly interconnected ecosystems remain less common but impactful, with 10% of organizations reporting reliance on more than 10,000 nth party suppliers.

(Source: Security Score Card, Supply Chain Cybersecurity Trends Report)

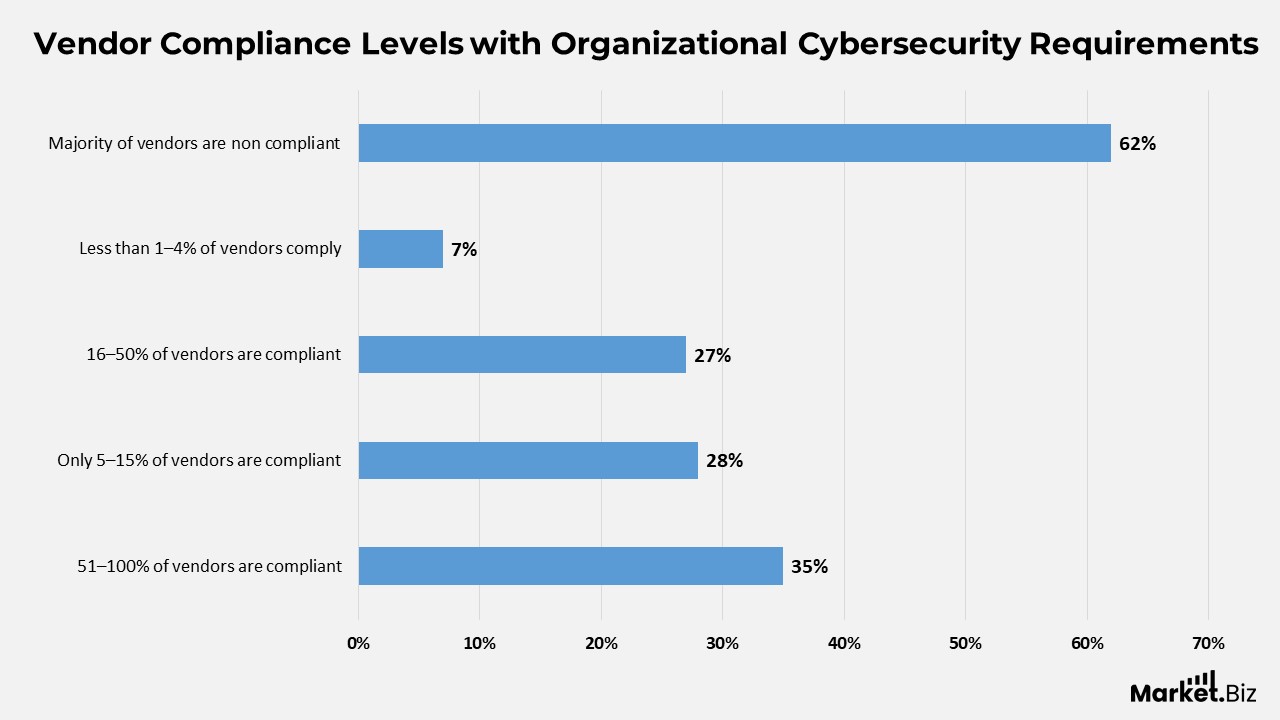

Vendor Compliance Levels with Organizational Cybersecurity Requirements

- Full compliance across vendor ecosystems remains limited, with only 35% of organizations reporting that 51%-100% of their vendors meet internal cybersecurity standards.

- Partial compliance dominates, as 28% of respondents indicate that just 5% to 15% of their vendors align with required cybersecurity controls.

- A comparable share, accounting for 27%, reports moderate adherence, with only 16% to 50% of vendors meeting cybersecurity expectations.

- Extremely low compliance persists among a subset of organizations, with 7% stating that only 1% to 4% of their vendors comply with cybersecurity requirements.

- Overall, compliance gaps remain significant, as 62% of organizations acknowledge that more than half of vendors within their supply chain ecosystems fail to meet mandated cybersecurity requirements.

(Source: Security Score Card, Supply Chain Cybersecurity Trends Report)

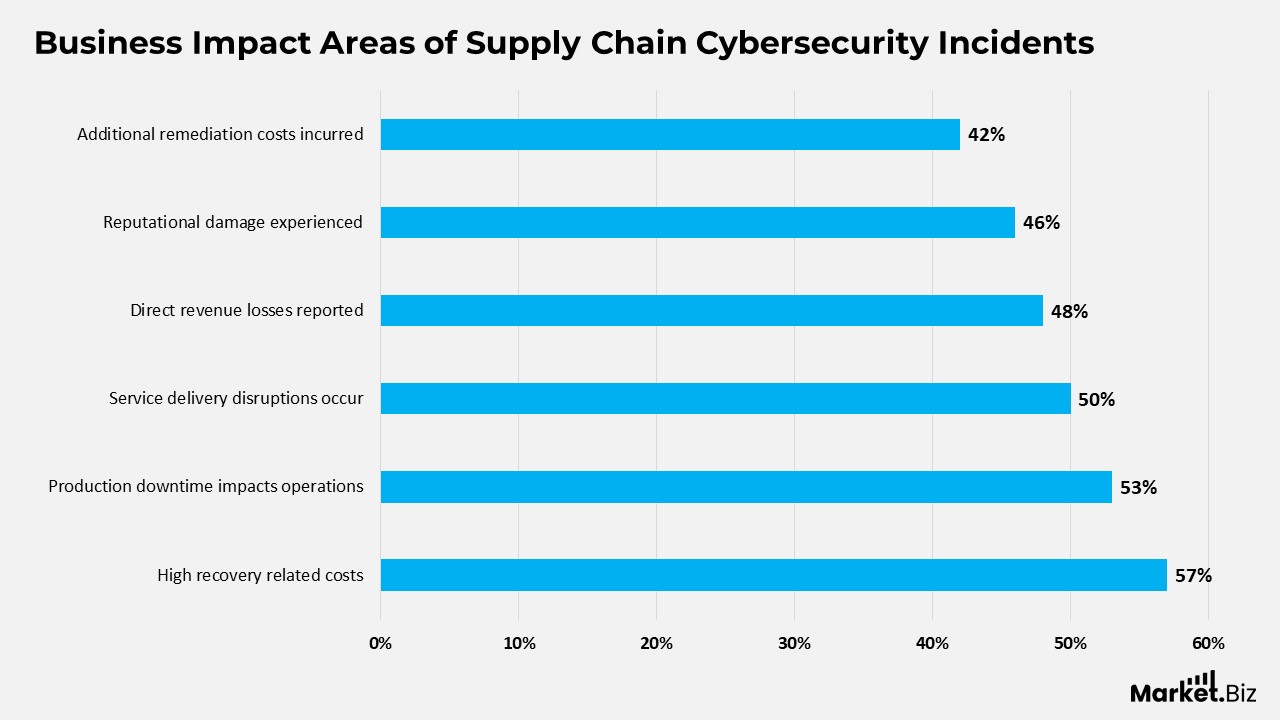

Business Impact Areas of Supply Chain Cybersecurity Incidents

- Financial recovery burdens rank highest, with 57% of organizations identifying recovery-related expenses as the most significant consequence of supply chain cyberattacks.

- Operational continuity faces substantial risk, as 53% of respondents highlight production downtime as a major impact on business operations.

- Service reliability remains vulnerable, with 50% of organizations reporting disruptions in service delivery following supply chain-related cyber incidents.

- Direct financial performance is affected, as 48% of respondents associate supply chain cyberattacks with measurable revenue losses.

- Brand and stakeholder trust erosion is widely recognized, with 46% citing reputational damage as a key outcome of such attacks.

- Post-incident corrective actions add further strain, as 42% of organizations cite remediation costs as an additional operational and financial burden.

(Source: Security Score Card, Supply Chain Cybersecurity Trends Report)

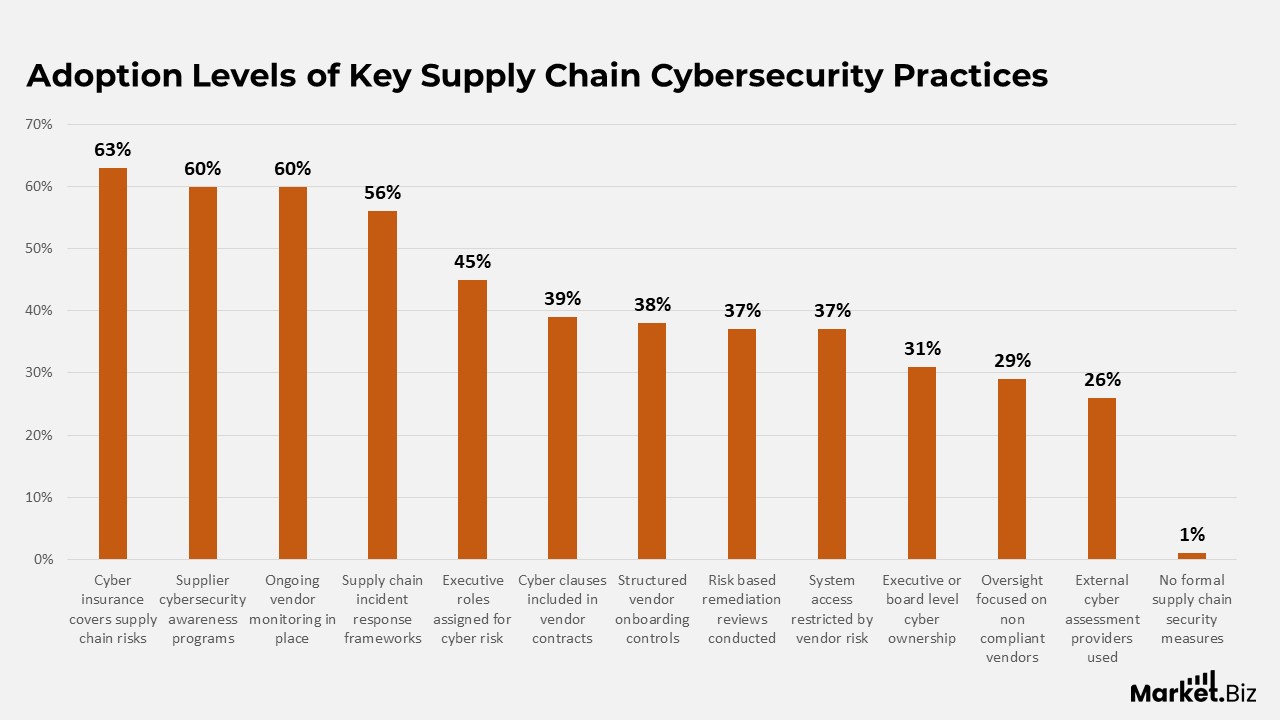

Adoption Levels of Key Supply Chain Cybersecurity Practices

- Broad supplier coverage forms the foundation of cybersecurity programs, with 63% of organizations extending cyber insurance coverage to include supply chain incidents.

- Awareness-driven controls remain a priority, as 60% of respondents emphasize cybersecurity awareness initiatives across their supply ecosystems.

- Continuous oversight is widely adopted, with 60% reporting active use of ongoing vendor monitoring mechanisms.

- Incident preparedness shows moderate maturity, as 56% of organizations maintain defined incident response frameworks for supply chain-related cyber events.

- Governance and accountability structures are less consistent, with 45% assigning dedicated roles for executive management of vendor cyber risk.

- Contractual enforcement remains limited, as only 39% of companies integrate formal cybersecurity requirements into their vendor contracts.

- Standardized onboarding controls lag further behind, with 38% applying structured vendor onboarding and offboarding processes.

- Risk-driven decision-making is uneven, with 37% conducting routine business remediation reviews tied to vendor cyber-risk exposure.

- Technical access controls are not universal, as 37% restrict digital system access based on vendor risk profiles.

- Strategic oversight gaps persist, with just 31% establishing clear ownership of cyber risk at the executive or board level.

- Tiered supplier governance remains underdeveloped, with 29% prioritizing cybersecurity oversight only for vendors that do not fully meet compliance requirements.

- Collaboration with external experts is limited, as 26% engage third-party vendors for cybersecurity assessments or monitoring.

- End-to-end maturity is rare, with only 1% of organizations reporting that they have no defined or formal supply chain cybersecurity measures in place.

(Source: Security Score Card, Supply Chain Cybersecurity Trends Report

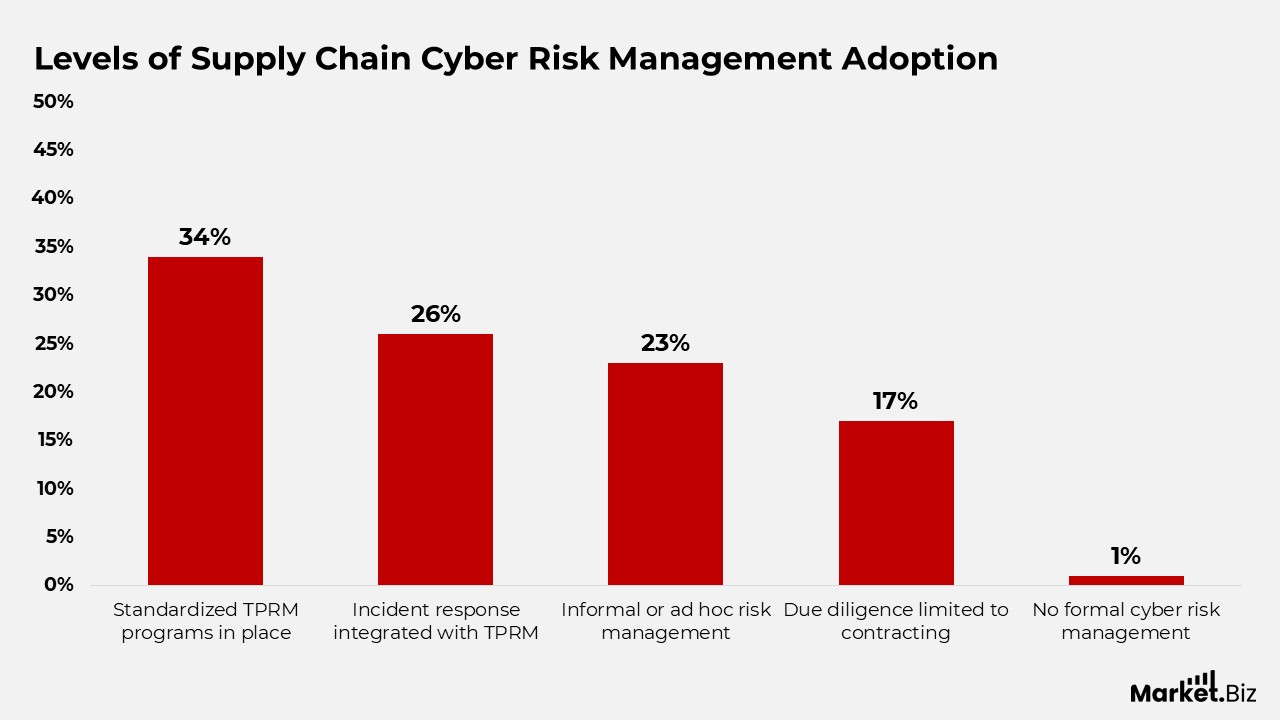

Levels of Supply Chain Cyber Risk Management Adoption

- Proactive risk management drives adoption, with 34% of organisations implementing standardised third-party risk management programs that emphasise breach prevention and ongoing controls.

- Advanced maturity is evident among 26% of respondents, who incorporate supply chain incident response capabilities focused on rapid remediation of supplier-related security issues.

- Informal governance structures remain common, as 23% of organizations rely on ad hoc third-party risk management practices supported by basic policies and workflows.

- Limited engagement persists across 17% of organisations, restricting cybersecurity due diligence to the initial contracting phase without continuous oversight.

- Comprehensive risk management remains absent for a small minority: 1% of respondents report no formal supply chain cyber risk management activities in place.

(Source: Security Score Card, Supply Chain Cybersecurity Trends Report)

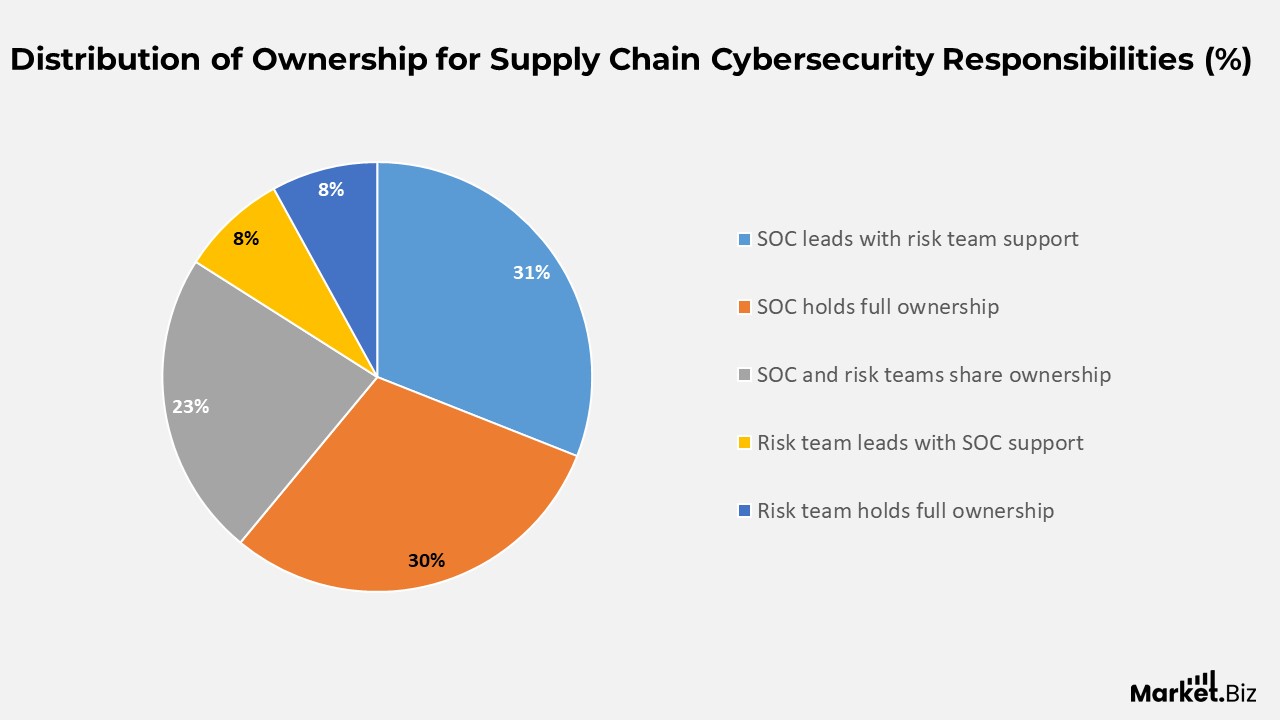

Distribution of Ownership for Supply Chain Cybersecurity Responsibilities

- Security Operations Centers dominate ownership models, with 31% of organizations assigning primary responsibility to the SOC while involving risk management teams in a supporting role.

- Centralized control remains common, with 30% of respondents reporting that supply chain cybersecurity ownership sits entirely within the SOC function.

- Balanced accountability is less widespread, with 23% of organizations sharing responsibility equally between SOC teams and risk management functions.

- Risk management-led approaches are limited, as only 8% of organizations place most responsibility with risk management while retaining some SOC involvement.

- Fully risk-management-driven ownership is rare, with just 8% of respondents indicating that risk teams alone manage supply chain cybersecurity oversight.

(Source: Security Score Card, Supply Chain Cybersecurity Trends Report)

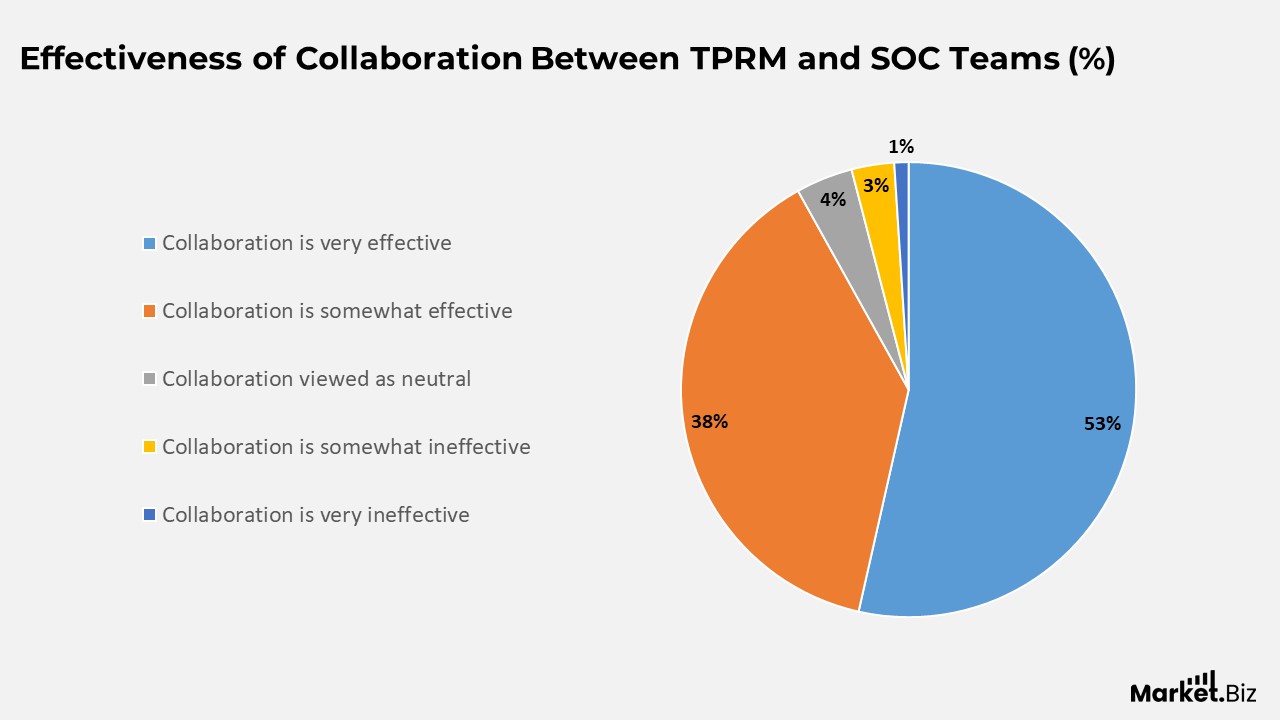

Effectiveness of Collaboration Between TPRM and SOC Teams

- Strong coordination dominates the landscape, with 53% of organizations reporting that collaboration between TPRM and SOC teams is very effective, supported by open communication and aligned workflows.

- Moderate effectiveness is also common, as 38% of respondents describe the collaboration as somewhat effective, indicating functional cooperation with scope for process improvement.

- Neutral perceptions remain limited, with 4% of organizations stating that collaboration is neither clearly effective nor ineffective in practice.

- Signs of coordination challenges persist, as 3% of respondents rate TPRM SOC collaboration as somewhat ineffective, reflecting gaps in information sharing or response alignment.

- Severe collaboration breakdowns are rare, with only 1% of organizations reporting very ineffective coordination between TPRM and SOC functions.

(Source: Security Score Card, Supply Chain Cybersecurity Trends Report)

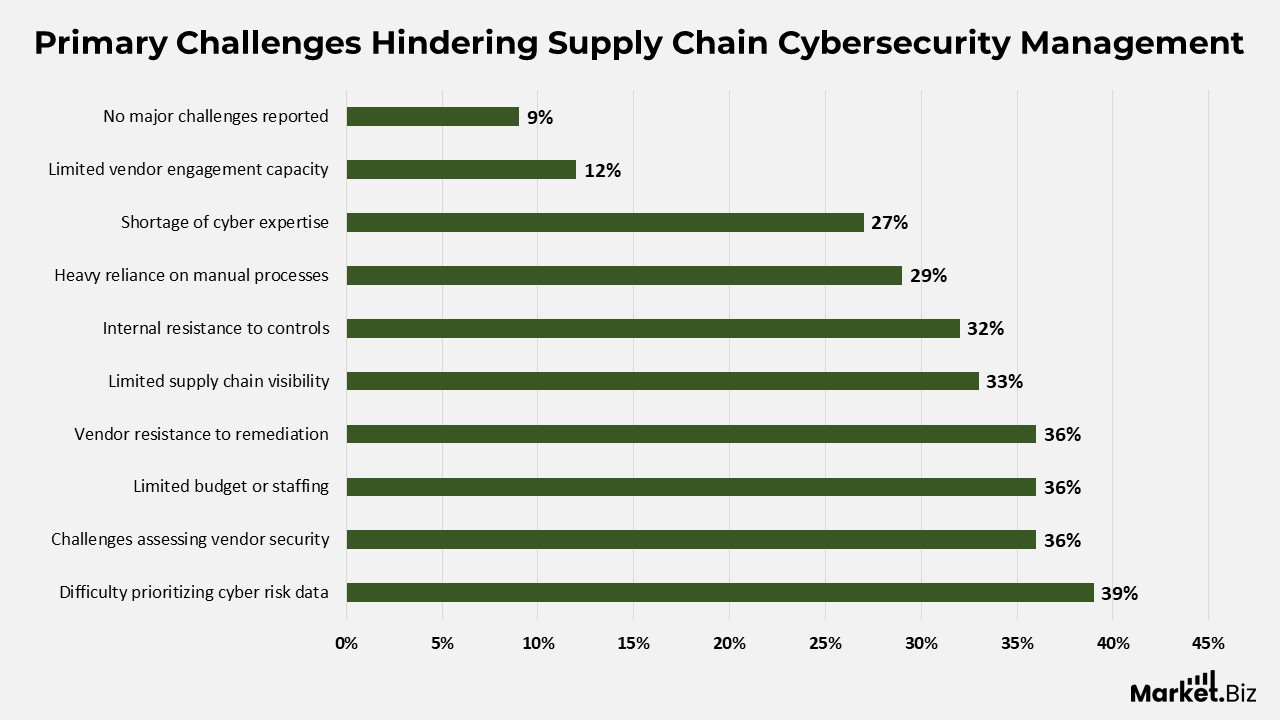

Primary Challenges Hindering Supply Chain Cybersecurity Management

- Information saturation remains the leading challenge, with 39% of organizations struggling to filter data and prioritize the most critical supply chain cyber threats.

- Vendor risk evaluation remains complex, as 36% of respondents report difficulty accurately assessing the cybersecurity posture of third-party suppliers.

- Resource constraints significantly limit program maturity, with 36% reporting insufficient staffing or budget to support supply chain cybersecurity initiatives adequately.

- Supplier engagement gaps persist: 36% of organisations face resistance or low participation from vendors when attempting to remediate identified security issues.

- End-to-end transparency remains inadequate, with 33% citing limited visibility across their broader supply chain ecosystem.

- Internal adoption barriers are also evident, as 32% report pushback from business units when implementing required security controls.

- Operational inefficiencies slow progress, with 29% highlighting an overreliance on manual processes in managing supply chain cyber risk.

- Skills shortages continue to constrain effectiveness, with 27% of respondents citing a lack of specialised cybersecurity expertise.

- Outreach capacity remains underdeveloped, with 12% stating they lack the resources to engage vendors on cybersecurity improvements actively.

- Only a small minority, 9%, report facing none of these supply chain cybersecurity challenges.

(Source: Security Score Card, Supply Chain Cybersecurity Trends Report)

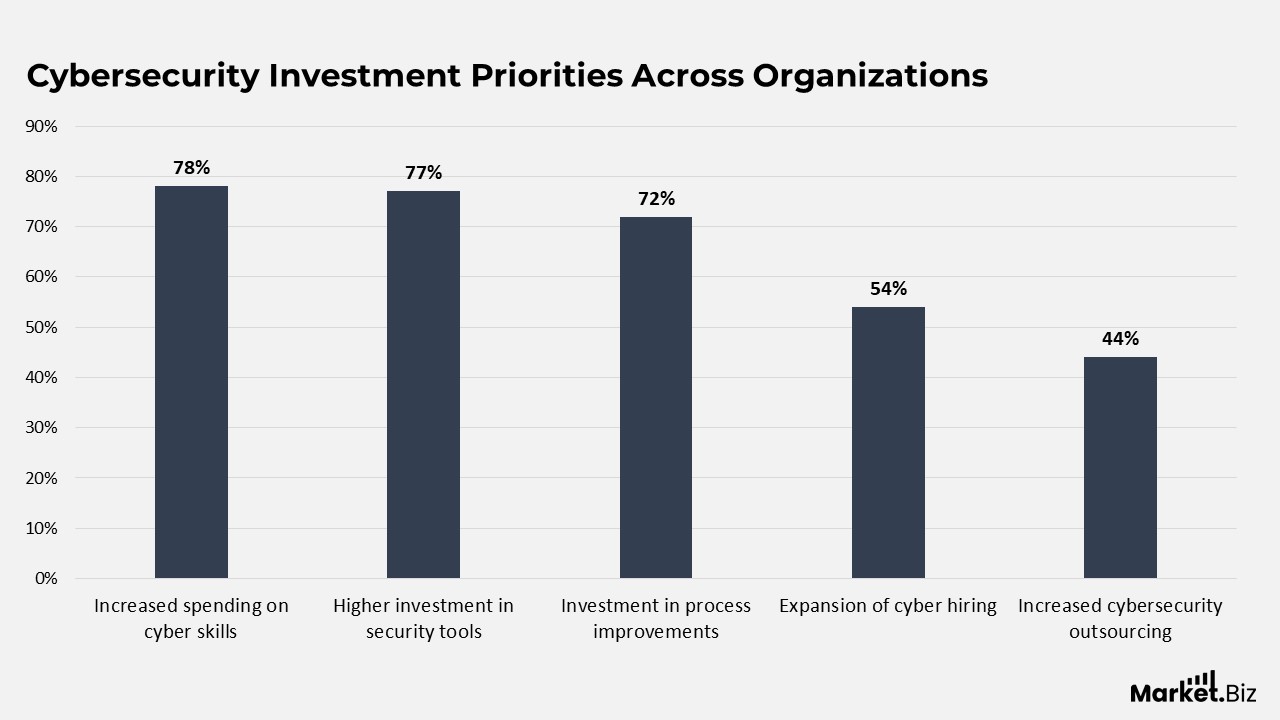

Cybersecurity Investment Priorities Across Organizations

- Skills enhancement leads budget allocation, with 78% of organizations increasing investment in cybersecurity skills development.

- Security tooling remains a core focus, as 77% of respondents allocate higher spending toward tools and advanced technologies.

- Operational maturity gains importance, with 72% investing in cybersecurity process improvements.

- Talent expansion continues steadily, as 54% of organizations increase hiring for cybersecurity roles.

- External service reliance grows at a slower pace, with 44% increasing cybersecurity outsourcing.

(Source: Security Score Card, Supply Chain Cybersecurity Trends Report)

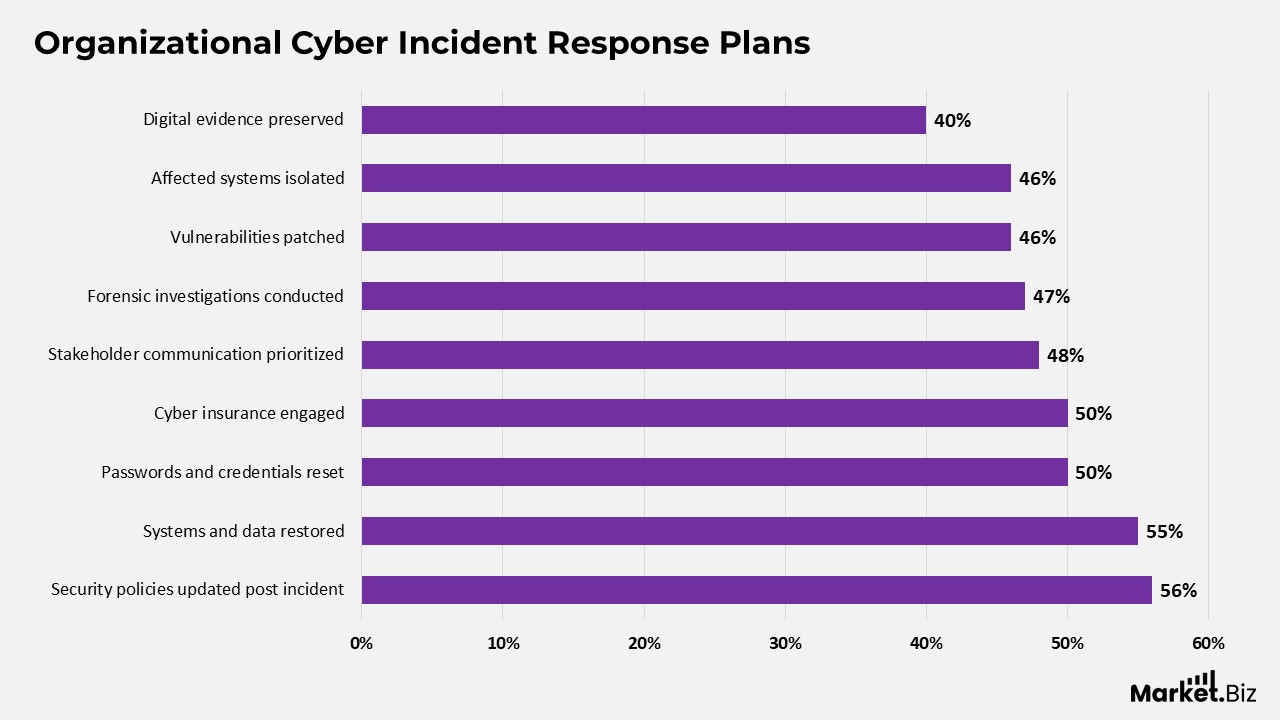

Organizational Cyber Incident Response Plans

- Policy strengthening is most common, with 56% of organisations reviewing and updating security policies after incidents.

- Business continuity takes priority, as 55% focus on restoring affected systems and data.

- Access control hygiene remains critical, with 50% of organisations changing passwords and credentials post-incident.

- Financial risk mitigation is widely practised, with 50% engaging cyber insurance providers during response efforts.

- Stakeholder transparency is emphasized, with 48% prioritizing communication during incidents.

- Technical root cause analysis is standard, with 47% conducting forensic investigations.

- Post-incident hardening continues, as 46% patches identified vulnerabilities.

- Containment measures remain essential, with 46% of impacted systems isolated.

- Legal and regulatory readiness receives comparatively less focus, with 40% focusing on preserving digital evidence.

(Source: Security Score Card, Supply Chain Cybersecurity Trends Report)

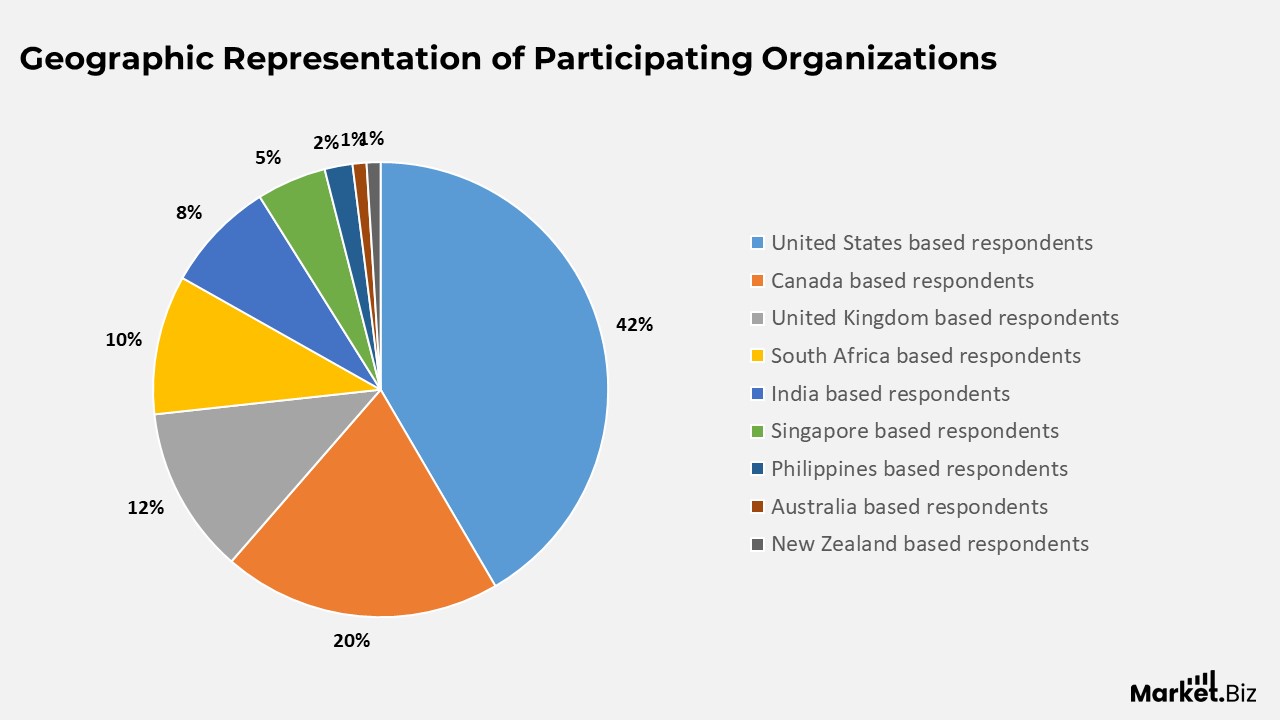

Geographic Representation of Participating Organizations

- The United States accounts for the largest share of respondents at 42%, indicating strong participation from North American organizations.

- Canada contributes 20% of responses, reinforcing North America as a key region in the dataset.

- The United Kingdom represents 12%, reflecting solid engagement from European markets.

- Emerging and smaller markets collectively add diversity, with South Africa at 10%, India at 8%, and Singapore at 5%.

- Limited participation is observed from the Philippines (2%), Australia (1%), and New Zealand (1%), indicating lower regional representation.

(Source: Security Score Card, Supply Chain Cybersecurity Trends Report)

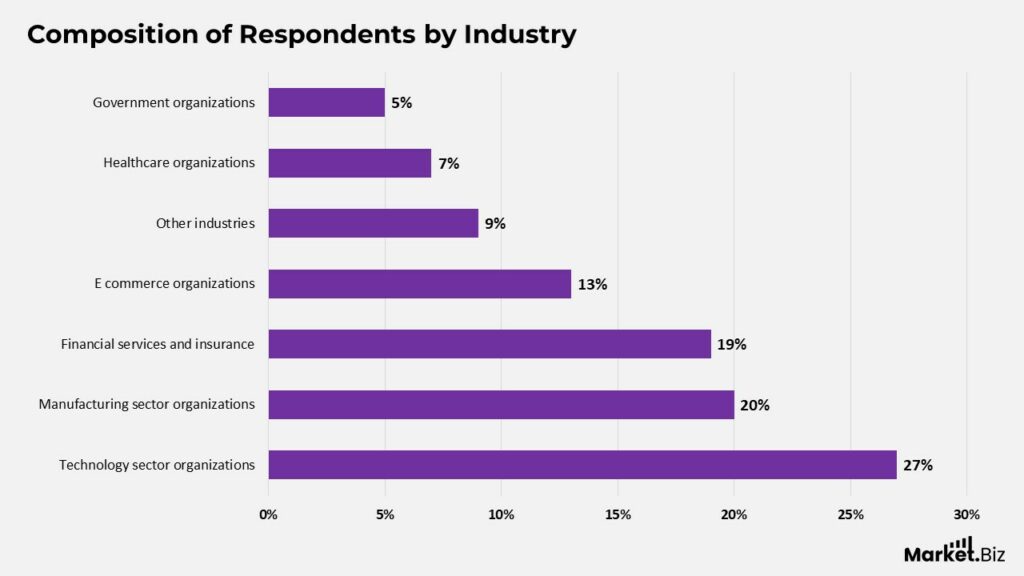

Composition of Respondents by Industry

- Technology-driven organizations form the largest group, representing 27% of total respondents.

- Manufacturing follows closely at 20%, highlighting the sector’s growing exposure to supply chain cybersecurity risks.

- Financial services and insurance account for 19%, reflecting high regulatory and cyber risk sensitivity.

- E-commerce contributes 13%, underscoring the importance of digital supply chains.

- Other industries collectively represent 9%, while healthcare (7%) and government (5%) show comparatively lower participation.

(Source: Security Score Card, Supply Chain Cybersecurity Trends Report)

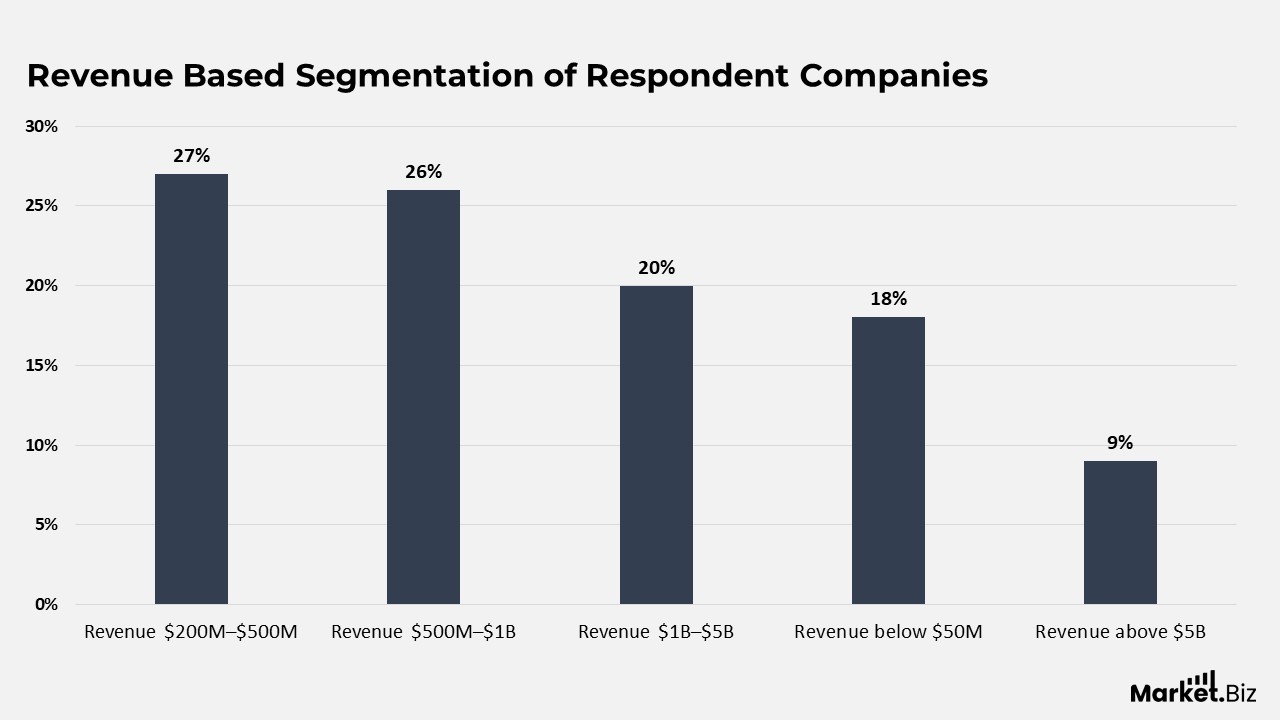

Revenue-Based Segmentation of Respondent Companies

- Mid-sized enterprises dominate the sample, with 27% reporting annual revenues between $200M–$500M.

- Large organisations are well represented, with 26% falling within the $500M–$1B revenue range.

- Upper mid-market firms account for 20% and generate revenues between $1B–$5B annually.

- Smaller organizations remain present, with 18% reporting revenues below $50M.

- Very large enterprises are rare, as only 9% report annual revenues exceeding $5B.

(Source: Security Score Card, Supply Chain Cybersecurity Trends Report)

Conclusion

Supply Chain Cybersecurity Statistics: The supply chain cybersecurity statistics point to an environment where risk awareness is high, yet exposure remains widespread due to limited visibility and uneven maturity across supplier networks.

Organisations increasingly acknowledge the seriousness of third-party and nth-party cyber threats, but gaps in vendor compliance, monitoring coverage, and governance continue to create systemic weaknesses.

The growing financial, operational, and reputational impacts reported across industries confirm that supply chain cyber risk is no longer an isolated issue, but a core business challenge. At the same time, the data reflects steady progress toward stronger defenses.

Rising investments in cybersecurity skills, tools, and process standardization, along with improved coordination between TPRM and SOC teams, suggest a gradual move from reactive to more structured risk management approaches.

However, persistent issues around accountability, incident readiness, and supplier engagement indicate that maturity remains uneven. Overall, the findings emphasize that lasting supply chain cyber resilience depends on continuous risk oversight. Clearer ownership models, and deeper integration of cybersecurity across the entire supplier ecosystem.

FAQ’s

In theory, supply chain cybersecurity statistics function as aggregated analytical indicators that explain how cyber risk spreads across interconnected organizational ecosystems. They are used to identify recurring patterns in vulnerability concentration, risk transmission, dependency exposure, and overall system resilience within complex, multi-tier supply networks.

From a conceptual risk management viewpoint, these statistics serve as evidence-based inputs for evaluating risk probability, impact severity, and exposure across third-party and nth-party relationships. They demonstrate how small, localized weaknesses can escalate into enterprise-wide or systemic risk due to dense interconnectivity and reliance on trusted external entities.

The data illustrates a transition from direct, perimeter-centric attack models to indirect infiltration tactics. In theoretical terms, this supports network risk theory, which posits that attackers intentionally exploit weaker or less protected nodes to penetrate more secure organisations through established trust relationships.

These statistics reveal a structural gap between assumed control and actual oversight within extended supply chains. Theoretically, reduced visibility weakens an organization’s capacity to detect, evaluate, and manage risk, thereby increasing uncertainty and magnifying the potential scale of loss.

From a governance theory standpoint, vendor compliance metrics reflect how effectively policies, contractual obligations, and accountability frameworks are enforced. Persistently low compliance levels signal a disconnect between formal governance structures and real-world execution across external supplier environments.