Introduction

Supply chain statistics provide a data-driven snapshot of how goods, information, and finances flow across global and regional networks. Reflecting a shift from traditional cost-focused models to complex, interconnected systems shaped by globalization, digitalization, and changing consumer expectations.

Metrics related to inventory efficiency, transportation performance, supplier reliability, and fulfilment speed have become essential for assessing operational resilience and competitiveness. Especially amid rising demand volatility, geopolitical uncertainty, and disruption risks from events such as pandemics and climate impacts.

As organisations adopt advanced analytics, automation, and AI-driven forecasting, supply chain statistics increasingly support real-time visibility, risk mitigation, and strategic decision-making, underscoring their role in enabling agility, transparency, and long-term growth across industries.

Editor’s Choice

- U.S. business logistics spending reached USD 2.3 trillion, accounting for 8.7% of national GDP. Underscoring the scale of logistics costs in the overall economy.

- Private equity played a growing role in advanced industries, accounting for 22% of all transactions completed in 2024.

- Advanced industries accounted for roughly 35% of global private equity buyout value in 2024, a sharp increase from less than 20% a decade ago.

- The U.S. third-party logistics market returned to modest growth. With net revenues rising 1.6% to USD 131.2 billion in 2024, after a steep decline in the prior year.

- U.S. international transportation management revenues rebounded, increasing 6.5% to USD 78.8 billion in 2024 following a significant contraction in 2023.

- Ocean freight activity improved as U.S.-based transportation managers recorded a 6.7% increase in average container volumes during 2024.

- Global supply chain pressure eased further, with the index falling from -0.22 in December 2024 to -0.31 in January 2025, signalling reduced congestion.

- Rail container efficiency improved as average terminal dwell times in the U.S. declined by 5% year over year in January 2025.

- Inventory efficiency across industries remained steady, with the average inventory turnover rate reaching 8.5 in 2024.

- On-time delivery performance showed room for improvement, with average fulfilment rates hovering around 85% during 2024.

- Digital transformation remains constrained by workforce gaps. With 90% of supply chain leaders reporting insufficient skills and talent to meet digitization objectives.

- Nearly 48% of manufacturers continue to face notable difficulty filling production and operations management roles.

- Workforce and talent shortages ranked among the most influential supply chain trends. With 35% of industry respondents citing them as the third-most-impactful issue.

(Sources: McKinsey & Company, Armstrong & Associates, EY, CSI Market, Qualtrics XMI Institute, Deloitte, MHI)

AI, Automation, and Smart Manufacturing Investments Reshaping Supply Chain Strategy

- 50% of supply chain organisations planned dedicated investments in AI and advanced analytics through 2024. Reflecting a shift toward data-driven decision-making.

- A strong majority of C-suite leaders (86%) feel ready to accelerate spending on generative AI in 2025.

- Enterprise-scale deployment of GenAI is expected to rise sharply. With 60% of executives planning organisation-wide adoption in 2025, compared with 36% in 2024.

- Smart manufacturing continues to attract capital, as 78% of manufacturers allocate more than 20% of their improvement budgets to these initiatives.

- Investment momentum remains high, with 88% of manufacturers expecting smart manufacturing spending to continue or increase in the next fiscal year.

- Confidence in AI’s impact is widespread. With 91% of leaders believe AI will materially improve operational effectiveness within the next 2 years.

- Cost optimization is a major driver, with 86% of executives planning AI and advanced analytics investments in 2025 to reduce expenses across customer service, sales, marketing, and supply chains.

- Global technology spending is projected to grow 5.6% in 2025, reaching USD 4.9 trillion.

- Software and IT services are expected to dominate technology budgets, accounting for 66% of global tech spend in 2025.

- AI and machine learning adoption remains uneven. With 29% of manufacturers currently using these technologies at the facility or network level.

- Industry forecasts suggest rapid acceleration, with AI adoption expected to climb from 28% today to 82% within 5 years.

Moreover

- Physical automation is gaining priority, as 37% of manufacturers rank robotics as a top 1 or 2 investment focus for the next 2 years.

- Nearly 45% of manufacturers plan to purchase automation equipment such as AGVs, AS/RS, or robotics within the next 3 years.

- Process automation also ranks high, with 46% of manufacturers identifying it as a leading near-term investment priority.

- Sensor-driven visibility is expanding, as 34% of manufacturers prioritize investments in active sensors over the next 24 months.

- Long-term adoption outlooks remain strong, with inventory and network optimization technologies projected to reach 92% adoption within 5 years.

- Autonomous vehicles and drones are expected to see broader adoption, with 5-year adoption predicted to reach 64%.

- Smart manufacturing initiatives delivered measurable workforce benefits in 2024, improving employee productivity by an average range of 7% to 20%.

- Nearly half of the potential GenAI-driven EBITDA impact, 48%, is expected to come from augmenting low- to medium-complexity tasks.

- Scaling GenAI remains challenging, with 28% of executives citing data or technology infrastructure limitations as the primary barrier.

- Workforce readiness is another constraint, as 55% of employees say better training and clearer guidelines would increase their confidence using GenAI tools.

- Cultural resistance persists, with 80% of senior leaders reporting that hesitation toward new technology is slowing their organisations compared to competitors.

- Among organizations not yet using AI in supply chain management. Restrictive IT policies represent the main adoption barrier for 22% of respondents.

(Sources: KPMG, Accenture, Deloitte, BCG, Forrester, MHI, Inspectorio)

Procurement Strategy Statistics

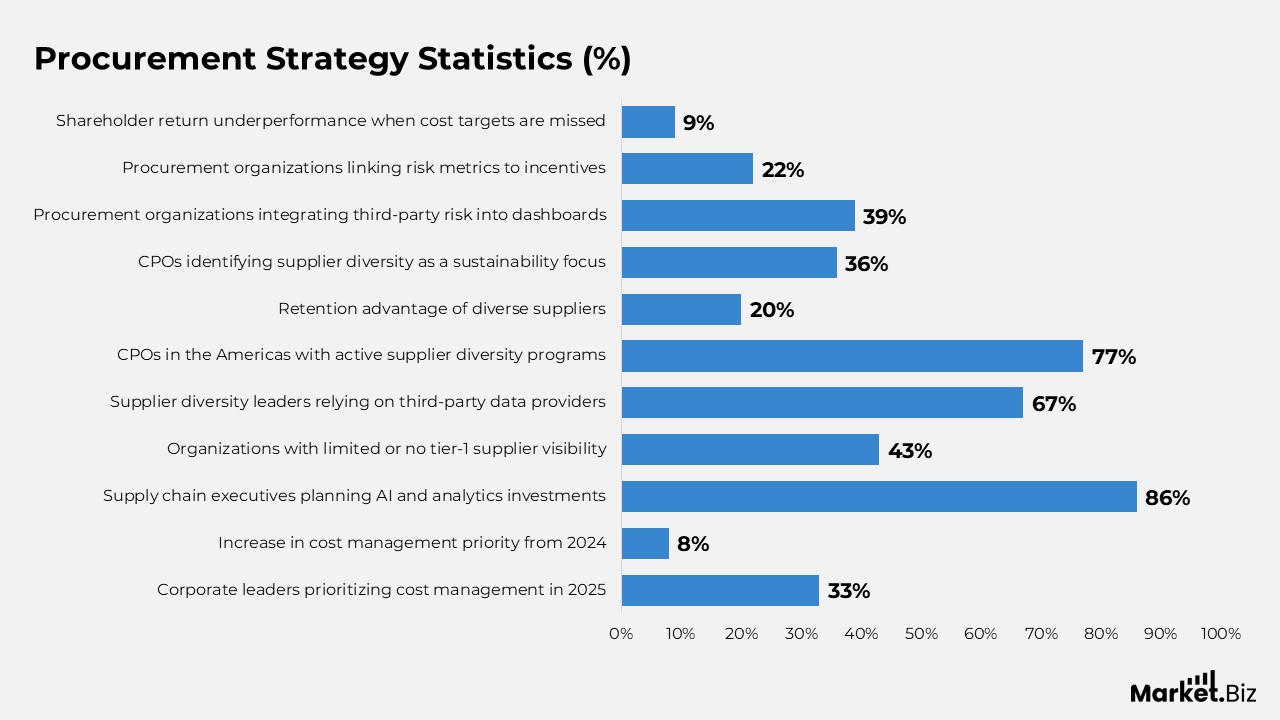

- Cost management remains the top priority, with one-third of corporate leaders ranking it as the top focus area in 2025, up 8 percentage points from 2024.

- Investment in advanced technologies is accelerating, as 86% of supply chain executives plan AI and analytics initiatives to drive cost reduction across procurement and supply chains.

- Supplier visibility gaps persist, with 43% of organizations reporting limited or no insight into tier-1 supplier performance.

- Data tracking and reporting capabilities emerged as the leading priority for supplier diversity leaders in 2023. Reflecting a stronger emphasis on measurable outcomes.

- External data dependence is high, with 67% of supplier diversity leaders relying on third-party data providers to improve accuracy and transparency.

- Supplier diversity programs are now mainstream. With 77% of chief procurement officers in the Americas report having an active program in place.

- Diverse suppliers deliver stronger continuity, with an average retention rate that is 20% higher than that of non-diverse suppliers.

- Sustainability objectives increasingly influence procurement strategy, with 36% of CPOs identifying supplier diversity as a core sustainability focus.

- Risk integration remains limited: only 39% of procurement organisations include third-party risk management in their executive dashboards, and just 22% link it to procurement incentive structures.

- Procurement performance directly affects shareholder outcomes: companies that miss cost targets underperform peers by an average of 9 percentage points in total shareholder return.

(Sources: EY, BCG, KPMG, Scoutbee, Bain & Company, The Hackett Group)

Supply Chain Risk, Disruption, and Compliance Statistics Defining Resilience Priorities

- Supply chain disruption has become a persistent risk, with events lasting longer than 1 month occurring every 3.7 years on average, and nearly 80% of organisations experiencing at least 1 disruption in the past year.

- Regulatory and compliance complexity continues to weigh on performance. As 77% of executives report negative business impact. While cybersecurity (51%) and data protection or privacy (51%) remain the top compliance risk priorities.

- Global trade dynamics are shifting toward regionalization, reflected in a 7% reduction in the average geopolitical distance of trade between 2017 and 2024.

- Strategic supply chain redesign is accelerating, with 71% of US CEOs planning changes over the next 3–5 years and 73% of US manufacturers citing trade uncertainty as a leading challenge in Q1 2025, up from 56% and 37% in the preceding quarters.

- Policy and tariff risk is prompting early action, as 31% of global executives have already launched contingency plans tied to regulatory and trade changes following the US election.

Moreover

- Macroeconomic pressure remains a dominant concern, with inflation (38%) and economic uncertainty (37%) ranking as the most impactful supply chain trends for 2025, and 61% of CEOs expect continued inflation alongside low economic growth.

- Cyber risk exposure is associated with rising financial consequences, with the average cost of a data breach increasing to USD 4.88 million in 2024 from USD 4.45 million in 2023.

- Technology-led resilience efforts are expanding, as 41% of organizations invest in asset engineering to withstand extreme weather, 85% of executives take proactive steps to address post-election market disruptions, and 40% of leaders still acknowledge a lack of preparedness for 2025.

- Organizations that use technology to strengthen compliance report clear performance gains. Including improved risk visibility (64%), faster issue identification and response (53%), and higher productivity or cost savings (43%).

(Sources: McKinsey & Company, BCI, PwC, Deloitte, BCG, MHI, Gartner, IBM, Marsh McLennan)

Current Levels of Supply Chain Visibility Across Organizations

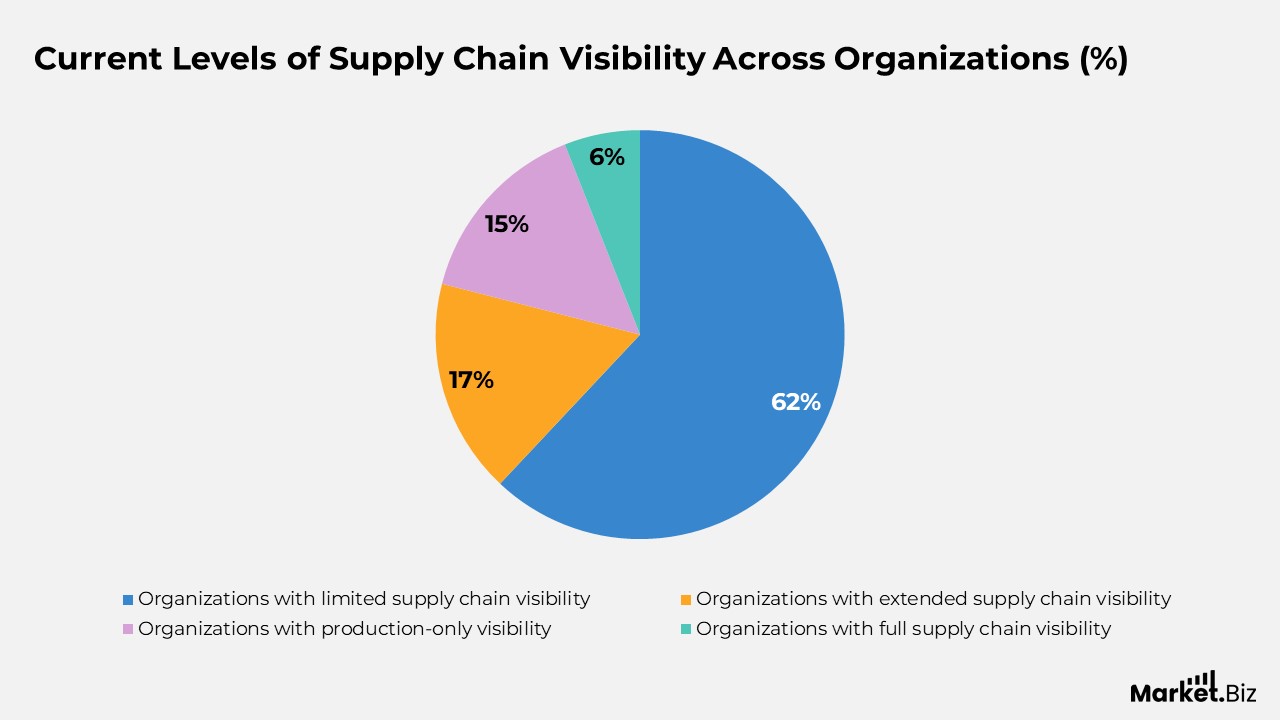

- A clear majority of organizations, 62%, operate with limited supply chain visibility, indicating significant gaps in end-to-end transparency.

- About 17% of organizations report extended visibility, suggesting partial insight beyond immediate operations but not full coverage.

- Visibility remains confined to production stages for 15% of organizations, limiting their ability to monitor upstream and downstream activities.

- Only 6% of organizations achieve full supply chain visibility, highlighting how rare comprehensive, real-time oversight remains across the industry.

(Sources: Blue Ridge Solutions Inc., Statistics)

Business Impact of Supply Chain Disruptions on Organizational Performance

- The most immediate consequence of supply chain disruptions is rising operating expenses. With 84.6% of organizations reporting increased working capital costs.

- Revenue erosion is a major outcome: 77.6% of organisations experience direct revenue losses following supply chain disruptions.

- Operational efficiency suffers significantly, with 76.4% of businesses reporting measurable productivity losses.

- Customer experience is heavily affected, as 73.8% of organizations face an increase in customer complaints during disruption periods.

- Stakeholder confidence weakens when disruptions occur, with 73.7% of organisations reporting stakeholder or shareholder concerns.

(Sources: Fictiv. com.., Statistics)

Strategic Supply Chain Resilience Actions Planned by Global Executives

- A majority of leaders are strengthening sourcing resilience, with 53% planning to adopt dual sourcing strategies for raw materials.

- Inventory buffers are becoming a priority, as 47% of executives intend to increase stock levels of critical products.

- Supplier diversification is gaining traction, with 40% of organisations planning nearshoring initiatives and expanding their supplier base.

- Regional supply networks are emerging, as 38% of executives plan to regionalize their supply chains to reduce dependency on distant markets.

- Portfolio simplification is underway, with 30% of companies aiming to reduce their SKU count to improve operational efficiency.

- Inventory placement strategies are evolving, as 27% of executives plan to hold higher inventory levels across multiple points in the supply chain.

- Production continuity is being reinforced, with 27% of organizations planning to establish backup manufacturing sites.

- Direct manufacturing relocation remains selective, as 15% of executives plan to nearshore their own production operations.

- Distribution capacity expansion is more targeted, with 15% of companies planning to increase the number of distribution centers.

(Sources: McKinsey & Company)

Technology Priorities Accelerating Digital Transformation in Supply Chains

- Advanced data analysis drives technology adoption, with 41% of supply chain organisations prioritising analytics to strengthen planning and decision-making.

- Connectivity and scalability are rising together, as 39% of companies focus on IoT solutions and another 39% emphasize cloud computing adoption.

- Digital risk management is gaining importance, with 31% of organizations ranking information security as a critical technology priority.

- Predictive capabilities are moving up the agenda, as 29% of supply chain leaders invest in predictive analytics to anticipate demand shifts and disruptions.

- Platform-based execution is expanding, with 25% of organizations prioritizing supply chain and logistics applications.

- Automation and advanced manufacturing tools are advancing steadily. As 22% of companies focus on robotics and another 22% on 3D printing technologies.

- Emerging logistics innovations are drawing attention, with 20% exploring drone usage and 19% assessing mobile production units.

- Distributed and intelligent systems remain long-term priorities, as 18% of organisations invest in blockchain and 17% explore cognitive robotics.

- The strategic value of technology is widely recognized, with 50% of companies stating that technological progress strongly impacts supply chain, logistics, and transportation performance.

(Sources: GEODIS, Forbes, Apps Run the World, Statista)

Conclusion

Supply chain statistics point to a fundamental evolution in how organizations design and manage their networks. Increasing exposure to disruption, rising logistics costs, and ongoing geopolitical and economic pressures have shifted priorities away from efficiency toward resilience and adaptability. While cost optimisation remains essential, it now operates alongside a stronger emphasis on supplier transparency, stronger compliance, and network flexibility.

Technology adoption continues to shape performance outcomes. Greater use of analytics, AI, automation, and cloud infrastructure is improving visibility, responsiveness, and planning accuracy, yet talent shortages, data quality issues, and internal resistance to change often constrain progress.

Taken together, the data show that long-term success depends on an organization’s ability to turn supply chain intelligence into timely action. Companies that embed risk awareness, leverage digital tools effectively, and build agile operating models are better equipped to navigate uncertainty and maintain sustainable growth.

FAQ’s

Supply chain statistics show that disruptions are more frequent and longer lasting. While costs, compliance complexity, and geopolitical risks continue to rise. At the same time, organizations are investing more in resilience, visibility, and digital capabilities to manage uncertainty and maintain continuity.

Data indicates that major disruptions occur regularly and affect a large share of organizations each year. These events often stem from geopolitical shifts, regulatory changes, climate impacts, or cyber incidents, making disruption a recurring challenge rather than a one-time event.

Statistics highlight technology as a critical enabler of performance. Analytics, AI, automation, and cloud platforms support better forecasting, faster response, and improved transparency, although skills gaps and infrastructure constraints still limit adoption.

Cost control remains a top priority, as logistics expenses and inflationary pressures directly affect profitability. However, statistics suggest that organisations are increasingly balancing cost management with investments in resilience, supplier diversification, and risk mitigation.

Data shows growing interest in nearshoring, dual sourcing, regionalization, and inventory buffering. These strategies aim to reduce dependency on single suppliers or distant regions while improving responsiveness and supply security.