Introduction

Low-Cost Airline Statistics: A Low-Cost Airline (LCC) operates under a business model that prioritises the reduction of operating expenses to provide considerably lower airfares. This is accomplished by eliminating traditional amenities such as complimentary meals and beverages.

Imposing fees for additional services (such as baggage and seat selection), utilising a single type of aircraft for operational efficiency, servicing secondary airports, and concentrating on direct, point-to-point routes with rapid turnaround times.

Low-cost carriers (LCCs) are transforming the aviation industry by making air travel attainable for billions of individuals through significantly reduced fares. They achieve this by minimising expenses via unbundled service offerings, operating single aircraft fleets (such as the A320 and B737), ensuring quick turnaround times, and utilising secondary airports.

This strategy has led to substantial global expansion, particularly in the Asia-Pacific region, where they have captured a considerable market share, accounting for approximately 30-33% of global seating capacity. Furthermore, they are intensifying competition with ultra-low-cost business models, establishing themselves as pivotal players in the leisure travel sector, and contributing to the evolution of the industry.

Editor’s Choice

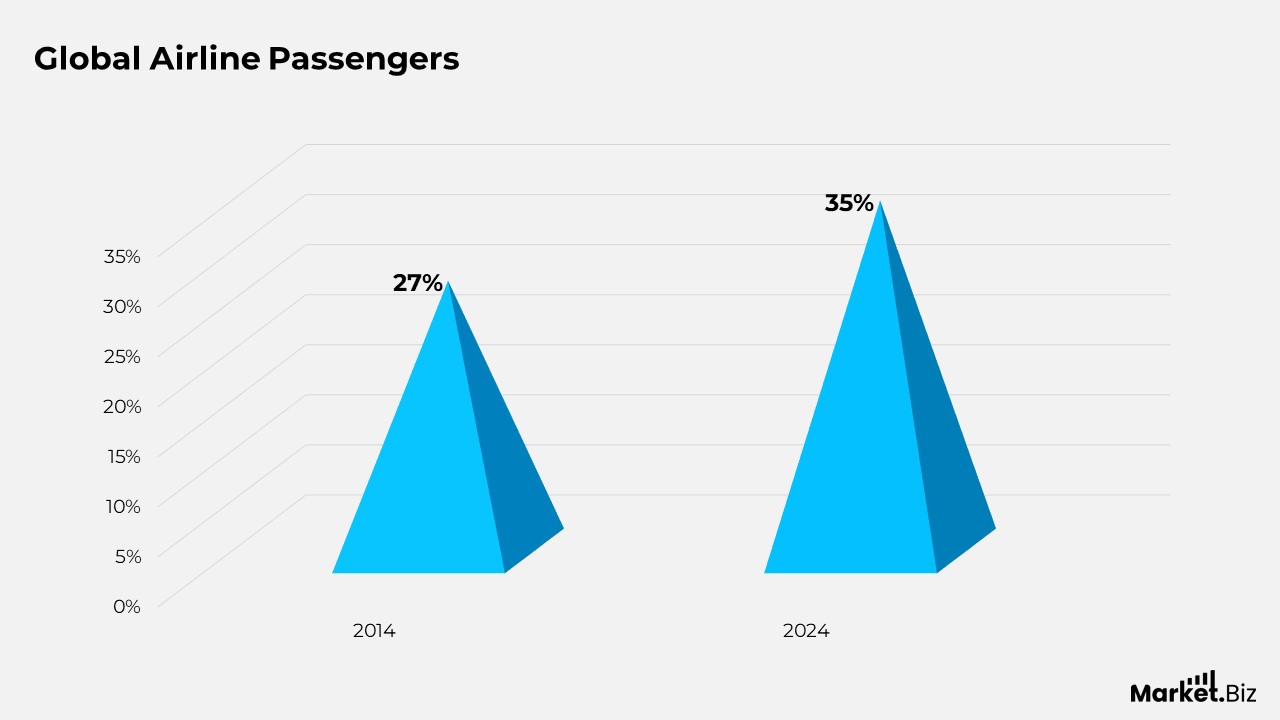

- Low-cost carriers represented roughly 35% of global airline passengers in 2024, an increase from approximately 27% in 2014.

- In 2024, Ryanair transported over 170 million passengers, establishing itself as the largest low-cost airline in the world by passenger volume.

- Domestic routes constitute approximately 69% of the overall passenger traffic for low-cost airlines globally.

- Online and mobile reservations represent roughly 91% of global ticket sales for low-cost airlines.

- Approximately 74% of travellers opt for low-cost airlines mainly because of their reduced ticket prices.

General Low-Cost Airline Statistics

- Low-cost carriers represented roughly 35% of global airline passengers in 2024, an increase from approximately 27% in 2014.

- More than 1.4 billion passengers globally travelled with low-cost airlines in 2024.

- Low-cost carriers function in over 90 countries, with more than 115 active airlines adhering to the LCC business model.

- Short-haul flights, generally lasting under 3 hours, constitute nearly 78% of all low-cost airline routes worldwide.

- Point-to-point routes make up about 76% of low-cost airline operations, in contrast to less than 45% for full-service carriers.

- Narrow-body aircraft comprise over 92% of LCC fleets, with the Airbus A320 and Boeing 737 families being the most prevalent.

- The average aircraft utilisation for low-cost airlines surpasses 12.5 flight hours per aircraft each day, compared to around 9–10 hours for traditional airlines.

- Ancillary services, such as baggage, seat selection, and food, are utilised by approximately 63% of LCC passengers on a typical flight.

Low-Cost Airline Market Size

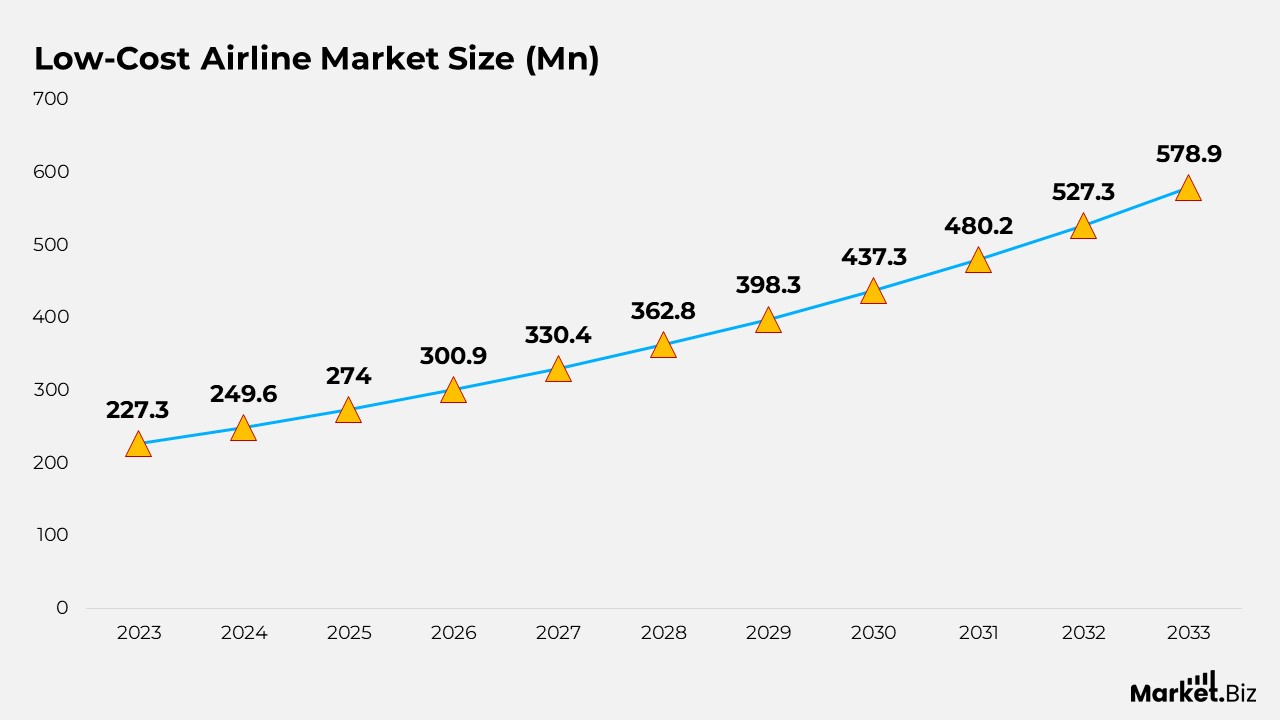

- The global market for low-cost airlines is anticipated to witness significant growth, increasing from USD 227.3 million in 2023 to an estimated USD 578.9 million by 2033, with a compound annual growth rate (CAGR) of 9.8% projected from 2024 to 2033.

- In 2023, the domestic sector dominated the market, capturing 63% of the share, driven by the post-pandemic recovery and an increasing demand for economical, short-distance travel.

- Leisure travel held a dominant position with a 70% market share in 2023, indicating a strong consumer inclination towards budget-friendly vacations and spontaneous travel experiences.

- Europe represented 31% of the market share in 2023, supported by its well-established infrastructure, competitive pricing, and a wide array of low-cost routes.

List of Low-Cost Airlines Statistics

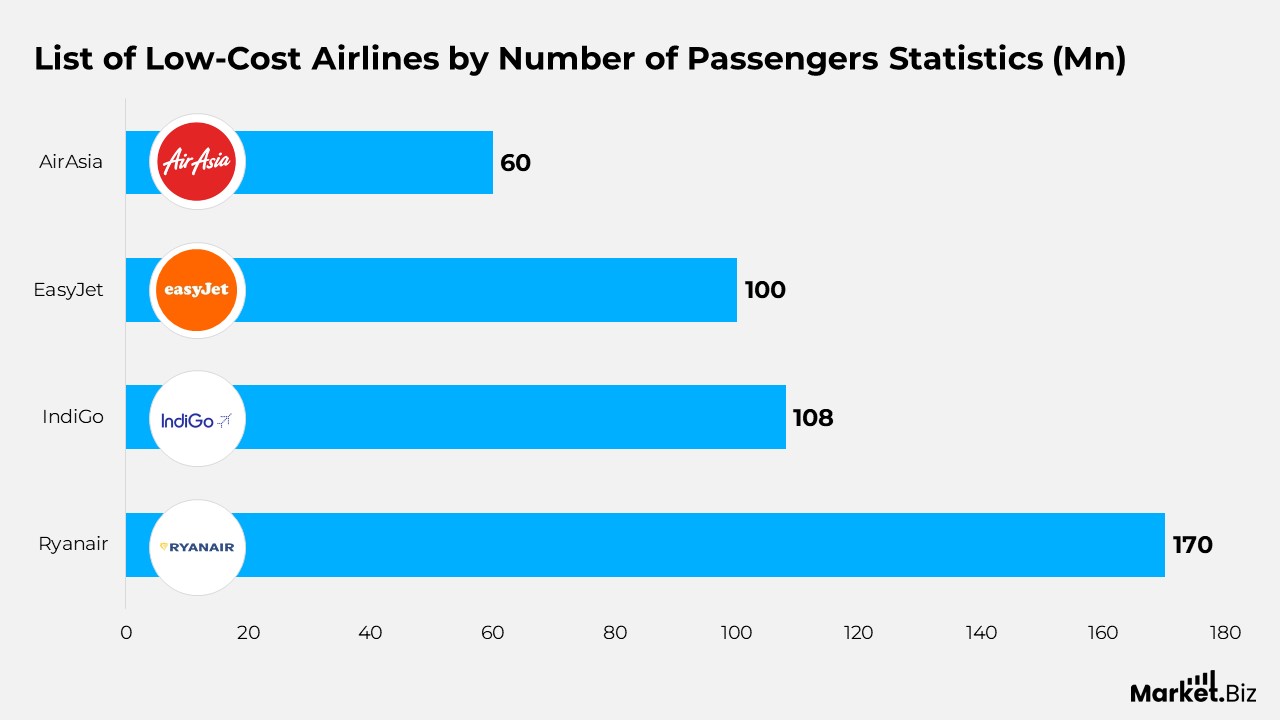

- In 2024, Ryanair transported over 170 million passengers, establishing itself as the largest low-cost airline in the world by passenger volume.

- In the same year, Southwest Airlines conducted more than 4,000 flights daily throughout the United States.

- IndiGo carried around 108 million passengers within a single year, capturing over 60% of India’s domestic air traffic.

- EasyJet provided services to more than 100 million passengers each year, operating in over 35 countries.

- AirAsia Group facilitated the travel of over 60 million passengers across Southeast Asia in 2024.

- Wizz Air operates in more than 50 countries and obtains over 55% of its passengers from Central and Eastern Europe.

- JetBlue represented approximately 9 to 10% of the total domestic passenger traffic in the U.S. among low-cost carriers.

- Together, Ryanair and EasyJet account for about 43 to 45% of the seat capacity for low-cost airlines in Europe.

Low-Cost Airline Passenger Statistics

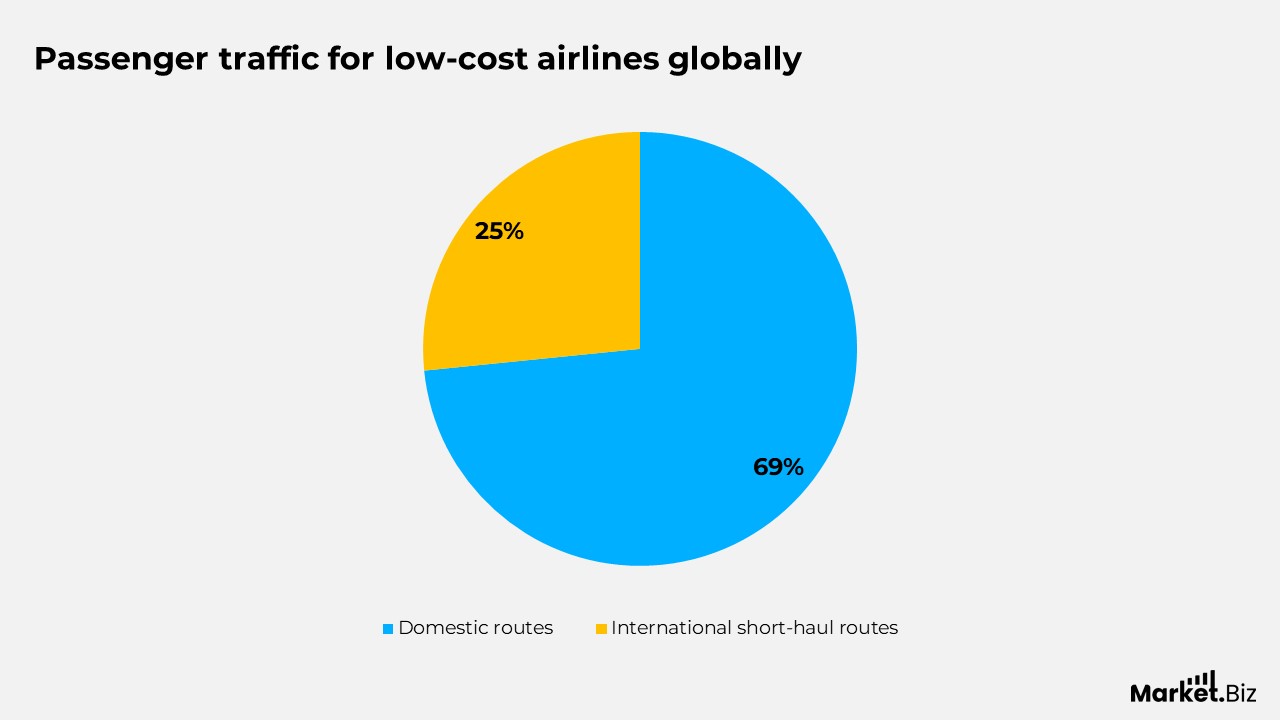

- Domestic routes constitute approximately 69% of the overall passenger traffic for low-cost airlines globally.

- International short-haul routes account for about 25% of total low-cost carrier passengers, especially in Europe and Southeast Asia.

- The average distance of low-cost airline routes worldwide is roughly 1,200–1,400 km.

- Low-cost airlines operate in excess of 640 airports around the globe, many of which are secondary or regional facilities.

- On average, more than 75 new low-cost airline routes are introduced each year globally.

- In Europe, low-cost carriers manage over 55% of all intra-European flights.

- The Asia-Pacific region represents approximately 37% of the global low-cost airline passenger market, marking the highest regional proportion.

- In the United States, low-cost carriers conduct nearly 33% of all domestic passenger flights.

Low-Cost Airline Booking Statistics

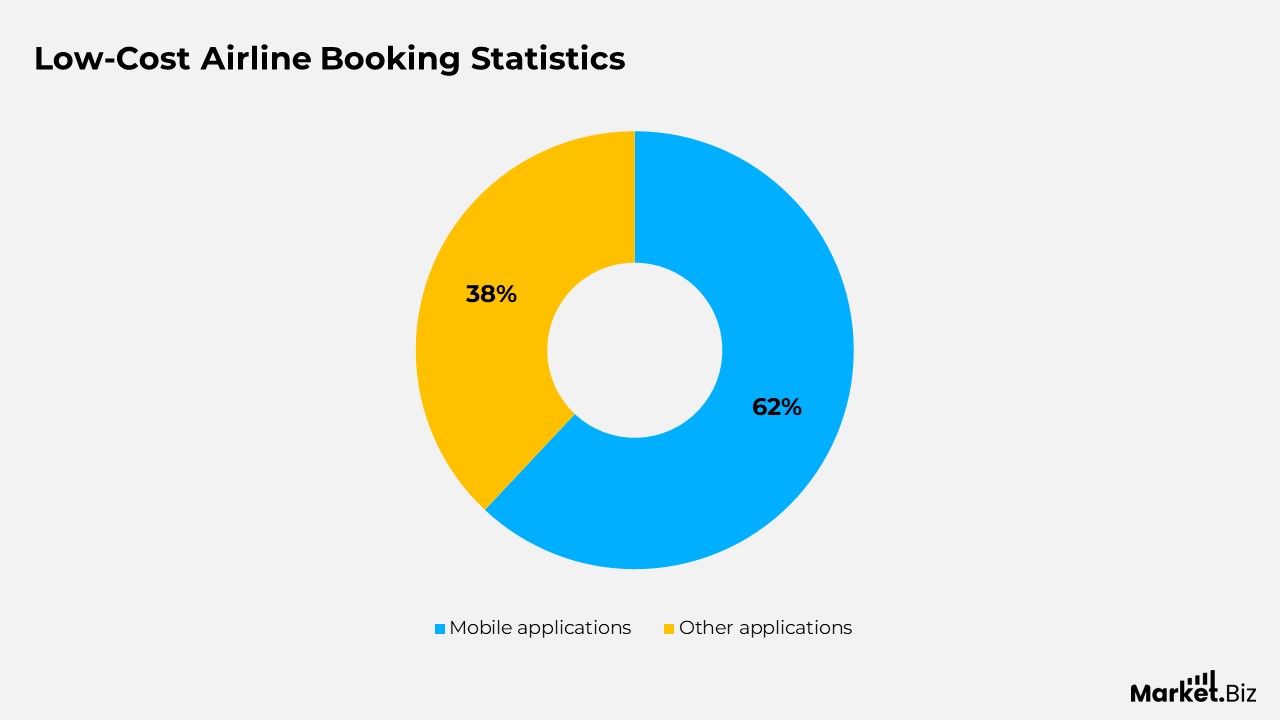

- Online and mobile reservations represent roughly 91% of global ticket sales for low-cost airlines.

- Mobile applications alone account for about 62% of total bookings for low-cost carriers.

- Over 70% of passengers flying with low-cost airlines opt for digital boarding passes rather than printed tickets.

- More than 85% of travellers using low-cost carriers utilise self-service check-in kiosks and online check-in options.

- Dynamic pricing mechanisms affect over 80% of ticket prices for low-cost airlines.

- Approximately 15% of customers of low-cost carriers take advantage of alternative payment methods such as ‘buy now, pay later.’

- Promotions via email and applications yield around 40% of repeat bookings for budget airlines.

- Tools for optimising load factors have enhanced average seat occupancy by 9% among leading low-cost carriers.

Regional Statistics Low-Cost Airline

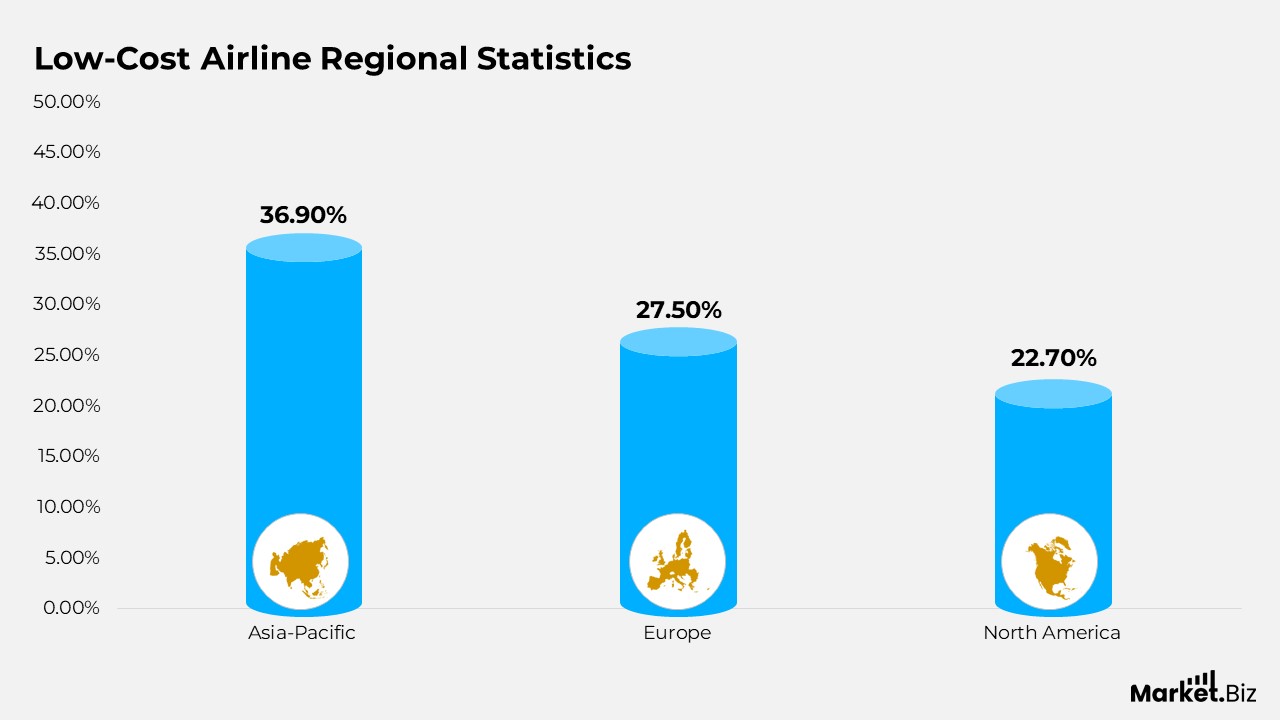

- In 2024, the Asia-Pacific region dominated global low-cost carrier (LCC) traffic, holding a 36.9% share, which equates to more than 528 million passengers.

- Both India and China experienced over 100 million low-cost airline passengers in 2024, indicative of robust domestic demand.

- Europe represented 27.5% of the worldwide low-cost airline traffic, accommodating over 390 million passengers across 32 nations.

- North America accounted for approximately 22.7% of global LCC traffic, with the United States being the primary contributor to this figure.

- In 2024, Ryanair and EasyJet together commanded 43.6% of the European LCC market share.

- Within Europe, Spain, Italy, and the United Kingdom each recorded more than 60 million LCC passengers in 2024.

- The utilisation of online and mobile boarding passes in Europe was notably high, with 76.5% of passengers opting for digital alternatives and 69.7% utilising mobile boarding passes.

Low-Cost Airline Consumer Behaviour Statistics

- Approximately 74% of travellers opt for low-cost airlines mainly because of their reduced ticket prices.

- Leisure travel accounts for nearly 58–60% of the overall passenger count on low-cost airlines globally.

- Business travellers make up about 24–26% of LCC passengers, a percentage that has consistently risen over the past ten years.

- Around 48–50% of passengers express concerns regarding baggage limitations and restricted on-board services.

- Almost 65% of travellers are willing to pay additional fees for extra services rather than opting for higher base fares.

- Repeat customers represent more than 55% of all low-cost airline reservations.

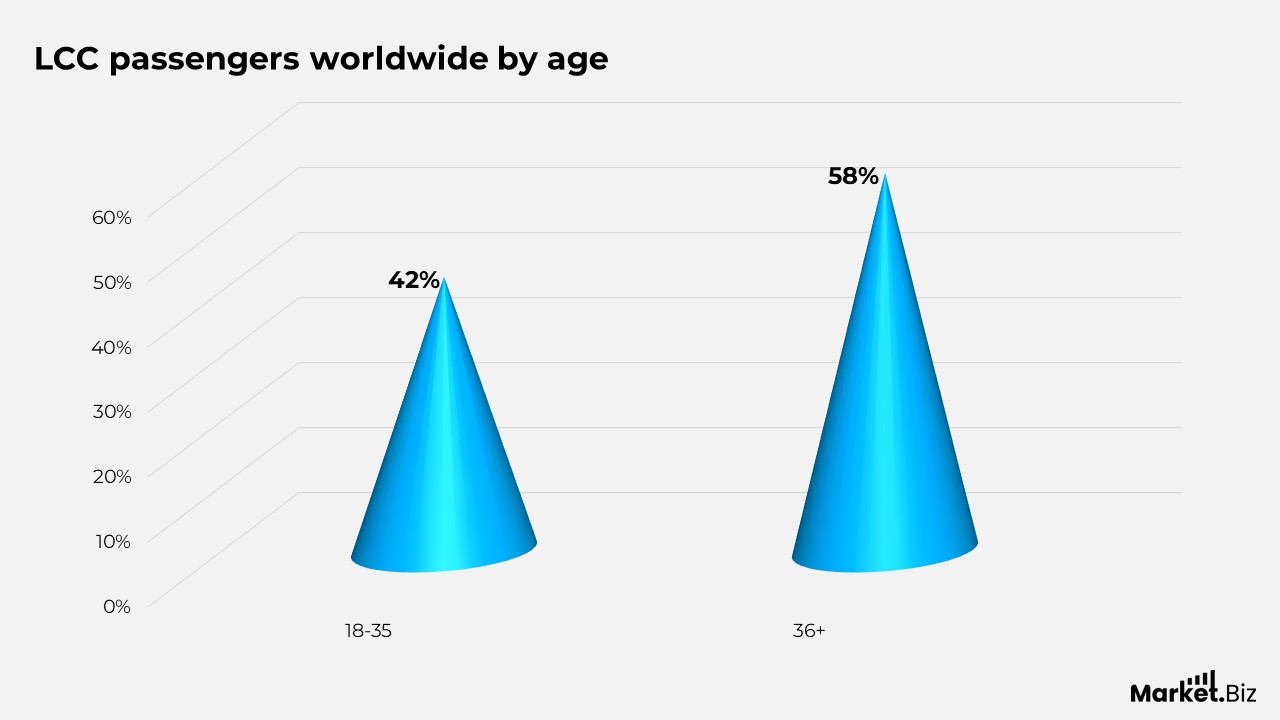

- Young travellers, aged 18–35, account for roughly 42% of LCC passengers worldwide.

- Customer satisfaction ratings for top low-cost airlines average between 7 and 7.5 out of 10.

Recent Development

- In 2024, JetBlue Airways declared that it had discontinued its $3.8 billion acquisition of Spirit Airlines Inc. This decision followed the ruling by the U.S. District Court for the District of Massachusetts in January, which determined that the transaction contravened antitrust laws designed to safeguard competitive markets within the United States.

- On October 1, 2024, Frontier Airlines, recognized for its extremely low fares, announced 22 new routes scheduled to commence in December.

Low-Cost Airline Future Prediction

- The LCC market size is anticipated to experience a substantial increase, potentially exceeding $380 billion by 2026, with a compound annual growth rate (CAGR) of over 16% through 2035.

- By 2030, low-cost carriers (LCCs) are expected to depend significantly on newer, fuel-efficient aircraft such as the A320neo and 737 MAX, which will enable them to achieve cost reductions of 15-20%. Additionally, the introduction of A321XLRs will facilitate entry into new long-haul markets.

- Furthermore, by 2030, short-haul flights may witness the emergence of hybrid or battery-powered aircraft, while overall design innovations. Including the use of lighter materials and concepts inspired by drones, could also come to the forefront.

Conclusion

Statistics from low-cost carriers (LCC) indicate significant global expansion, particularly in the Asia-Pacific region, fuelled by low fares and an expanding middle class. However, profitability encounters obstacles, especially regarding ancillary revenue in markets such as India.

Notable trends encompass operational efficiency through the use of secondary airports and standardised fleets, network growth, hybrid business models, heightened passenger demand, and fierce competition compelling legacy carriers to adjust.

The future appears to be oriented towards sustainability and the utilisation of technology to enhance customer experience, notwithstanding the financial changes following the pandemic.

FAQ’s

US low-cost airlines are encountering difficulties due to inflation in labour and maintenance costs, economic instability, and additional fees and flight delays that have negatively impacted many travellers’ perceptions of the budget-carrier model experience.

Currently, there are 811 scheduled airlines, of which 102 are classified as low-cost carriers. Despite the large number of airlines, it is noteworthy that 80% of all air travel, as indicated by Available Seat Kilometres (ASKs), is conducted by merely 13%, or 103 of these airlines.

Cebu Pacific is an ultra-low-cost airline from the Philippines, headquartered in Pasay, Metro Manila. Established in 1988, it holds the distinction of being the first low-cost carrier in Asia and is also the largest airline in the Philippines in terms of fleet size