Introduction

IT Statistics provide a clear snapshot of how organizations adopt, manage, and invest in digital systems across industries. These figures help businesses understand technology maturity, spending patterns, workforce readiness, and emerging risks such as cybersecurity and data governance.

By tracking trends in infrastructure, software, cloud adoption, artificial intelligence, and IT operations, decision makers can benchmark performance, identify gaps, and plan future strategies. Well-structured IT statistics turn complex technology landscapes into actionable insights that support smarter investment and operational decisions.

Editor’s Choice

- 92% of G2000 enterprises outsource at least part of their IT operations, underscoring the deep embedding of external IT services in large organisations.

- Global spending on digital transformation is projected to reach nearly US $3.9 trillion by 2027, reflecting technology’s role as a core business driver rather than a support function.

- Despite significant investment, only 35% of digital transformation initiatives achieve their stated objectives, highlighting a persistent execution gap.

- Artificial intelligence is expected to add approximately US $15.7 trillion to the global economy by 2030, making it one of the most influential economic forces of the decade.

- Around 65% of organizations have already implemented AI solutions, yet 74% struggle to scale AI initiatives into measurable business value.

- Cloud adoption continues to accelerate, with over 70% of companies using cloud services for some or all of their operations.

- Cybersecurity risks remain elevated, as 43% of cyberattacks target small businesses, many of which lack advanced security infrastructure.

- The global IT workforce is projected to grow at an annual rate of 6% between 2024 and 2034, driven by rising demand for digital and automation skills.

- Managed IT services adoption is widespread, with nearly 55% of small and mid-sized businesses relying on third-party providers to manage IT complexity and costs.

- Data quality remains the leading barrier to transformation, cited by 64% of organisations, and poor data contributes to trillion-dollar annual economic losses worldwide.

Key Artificial Intelligence Statistics Shaping Global Business and Workforce Trends

- Artificial intelligence is projected to contribute nearly USD 15.7 trillion to global economic output by 2030, making it one of the most powerful growth engines worldwide.

- By 2025, AI-driven transformation is expected to reshape employment, displacing around 85 million roles while generating about 97 million new ones, resulting in a net job gain of roughly 12 million.

- The AI industry continues to expand at an exceptional pace, with year-on-year growth projected at around 120%, reflecting accelerating enterprise demand.

- Over the next decade, AI adoption is expected to boost global labour productivity growth by approximately 1.5 percentage points through automation and smarter decision support.

- Software development, marketing, and customer service currently lead in AI investment and adoption, driven by the need for efficiency, personalization, and faster execution.

- Manufacturing is expected to benefit most from AI integration, with potential profit gains estimated at about USD 3.8 trillion by 2035, driven by automation and process optimisation.

- Despite technological advances, 73% of organizations still rely heavily on manual activities such as data entry and validation during planning and budgeting.

- Across global industries, around 65% of businesses have adopted AI mainly to reduce repetitive, labour-intensive workloads.

- About 92% of supply chain leaders admit they rely on intuition-based decisions because their reports lack the predictive insights that AI-enabled analytics can provide.

- AI-driven automation helps sales professionals save roughly 2 hours and 15 minutes each day, allowing greater focus on high-value tasks, a benefit acknowledged by 78% of sales teams.

(Sources: Point.co, Statista)

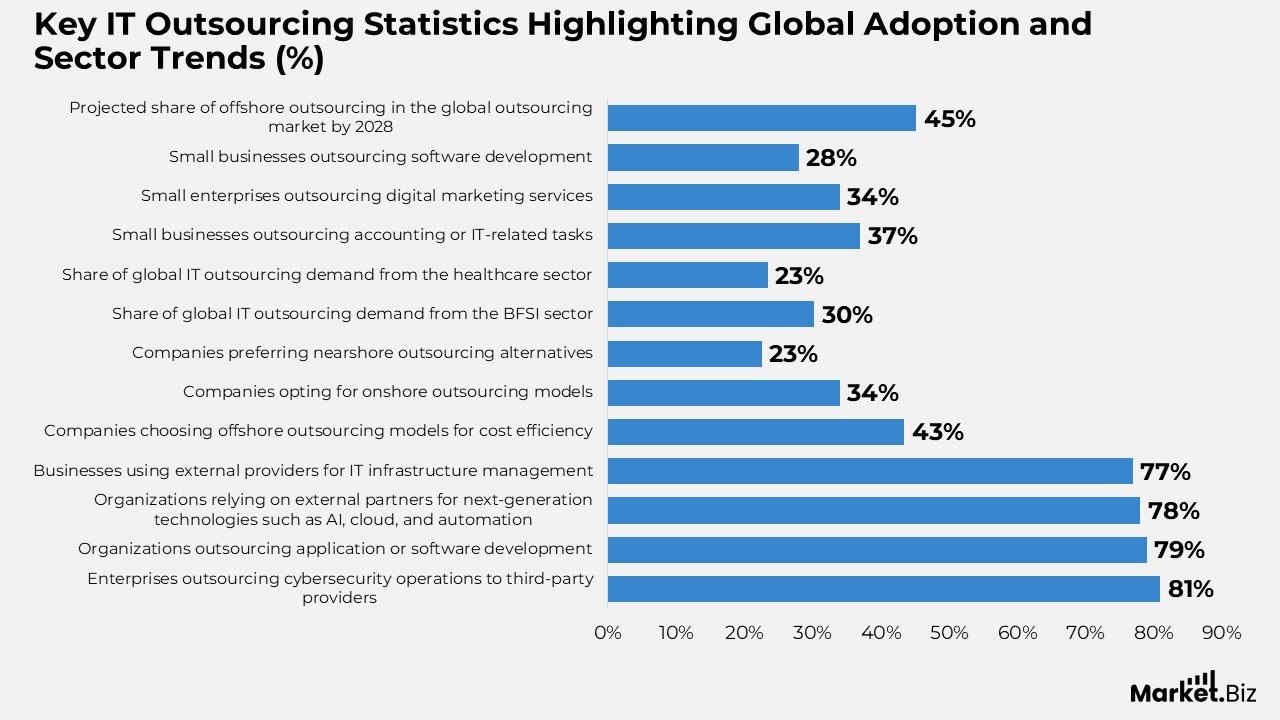

Key IT Outsourcing Statistics Highlighting Global Adoption and Sector Trends

- Recent industry analysis shows that 81% of enterprises now delegate cybersecurity operations to specialized third-party providers to strengthen protection and reduce internal workload.

- Around 79% of organizations outsource application or software development, while 78% rely on external partners for next-generation technology capabilities such as AI, cloud, and automation.

- Survey findings indicate that 77% of businesses use external service providers to manage their IT infrastructure, reflecting strong demand for scalable, managed environments.

- Cost optimization remains a key driver of outsourcing location strategy, with 43.46% of companies choosing offshore models, followed by 33.98% opting for onshore services and 22.56% favoring nearshore alternatives.

- The banking, financial services, and insurance sector represents the largest share of global IT outsourcing demand at 30.29%, driven by regulatory complexity and digital transformation needs.

- Healthcare accounts for approximately 23.43% of overall IT outsourcing activity, driven by rising digital health adoption and data management requirements.

- Among small businesses, 37% outsource accounting or IT-related tasks to lower operating costs and gain access to specialized expertise.

- About 34% of small enterprises outsource digital marketing services to gain external skills for online growth and customer engagement.

- Nearly 28% of small businesses turn to third-party vendors for software development to accelerate product delivery and manage resource constraints.

- Offshore outsourcing is projected to account for around 45.24% of the global outsourcing market by 2028, underscoring its continued appeal for large-scale cost efficiencies.

(Sources: Point.co, Statista)

IT Workforce and Budget Insights

- Nearly 9 out of 10 organizations plan to raise their IT budgets in 2025, reflecting sustained confidence in technology-led growth.

- Only about 4% of companies reported reductions in IT budgets during 2024, indicating limited pullback despite economic pressures.

- Average spending per employee in the IT services sector is estimated to reach US $399 in 2024.

- The global IT workforce is projected to expand at an annual rate of 6% between 2024 and 2034.

- India’s developer community on GitHub is expected to surpass the US’s by 2027, overtaking the current benchmark of 21 million developers.

(Sources: Gartner, IDC, Statista, US Bureau of Labour Statistics, GitHub Octoverse)

AI and Automation Statistics

- About 65% of companies have already implemented generative AI to improve productivity.

- The global AI market is projected to grow from US$ 214.6 billion in 2024 to US$ 1,339.1 billion by 2030.

- India leads global AI adoption at 59%, followed by the UAE at 58%.

- Nearly 72% of organizations report improved decision-making after adopting AI.

(Sources: McKinsey & Company, Statista, IBM Global AI Adoption Index, PwC)

Cloud Computing Statistics

- Around 51% of IT spending is expected to shift to cloud infrastructure by 2025.

- More than 70% of organizations already use cloud services for part or all of their operations.

- About 73% of companies adopt multi-cloud strategies.

- Nearly 50% of enterprises adopted cloud-native storage solutions between 2023 and 2024.

(Sources: Statista, IDC, Flexera, VMware, Red Hat)

Digital Transformation Statistics and Insights

- By 2024, nearly 94% of companies in the US and UK had adopted digital transformation strategies.

- Global digital transformation spending is expected to reach US $3.9 trillion by 2027.

- About 75% of organizations view digital transformation as critical to future success.

(Sources: PwC, IDC, Boston Consulting Group)

IT Spending Statistics by Sector

- Healthcare IT spending is projected to reach US $265.2 billion in 2024.

- The BFSI sector accounts for approximately 30.29% of global IT outsourcing activity.

- Manufacturing IT investments are growing by about 7.6% in 2024.

- Retail IT spending is expected to rise by nearly 6% in 2024.

(Sources: Statista, Deloitte, PwC, National Retail Federation)

Future Technology Trends

- About 90% of organizations expect blockchain to play a major role in data security.

- IoT adoption for automation increased to 58% in 2024, up from 33% in 2021.

- Nearly 93% of businesses see AI as a key growth driver in manufacturing.

(Sources: Gartner, Statista, Accenture)

Managed IT Services

- Nearly three-quarters of the total global outsourcing contract value is concentrated in IT services, underscoring their dominance in enterprise outsourcing strategies.

- IT outsourcing adoption is extremely high among large enterprises, with about 92% of G2000 companies relying on external IT service providers.

- Around 83% of IT decision makers are actively considering outsourcing security-related functions to improve protection and reduce internal complexity.

- Organizations adopting managed IT services can reduce internal IT operating costs by up to 40% through efficiency gains and reduced staffing needs.

- Managed IT services are widely used by smaller firms, with nearly 55% of small and medium-sized businesses leveraging these solutions.

- About 57% of organizations view IT outsourcing as a way to focus more effectively on core business activities rather than technology management.

- Email and data risks remain significant: 1 in every 323 emails sent to small businesses contains malicious content, and around 140,000 hard drives in the US experience data loss each week.

- Cost savings remain a major benefit: 50% of companies using managed service providers report IT cost reductions of 1 to 24%, while 33% achieve savings of 25 to 49%, and 13% report savings above 50%.

- Nearly 70% of organisations plan to shift their security responsibilities to managed security service providers within the next 12 months.

(Sources: ISG, Deloitte, Gartner, Statista, CompTIA, Kaspersky, US Cybersecurity Reports)

Cybersecurity

- Small businesses are disproportionately affected by cyber threats, accounting for approximately 43% of all recorded cyberattacks.

- Customer trust is highly sensitive to breaches, with about 24% of customers likely to discontinue their relationship with a company following a security incident.

- For small businesses, system outages and data crashes can result in losses of up to US $10,000 per hour, severely impacting operations.

- Only 54% of US companies with more than 500 employees have a fully developed disaster recovery plan.

- Internet-connected systems face constant threats, with research showing that hacking attempts occur roughly every 39 seconds.

- Human factors remain a major vulnerability, as more than 95% of cybersecurity incidents are linked to human error.

- Financial exposure is severe for SMBs: over 50% of cyberattacks result in losses exceeding US$500,000, and 83% lack the financial capacity to recover fully.

- Internal skill gaps persist, with about 62% of small and medium-sized businesses lacking sufficient in-house cybersecurity expertise.

- Data protection practices remain inconsistent, as roughly 21% of company data folders are left unsecured and accessible without restrictions.

(Sources: Verizon DBIR, IBM Security, University of Maryland, Turbotek, Maricopa Small Business Development Center, FEMA, US Small Business Administration)

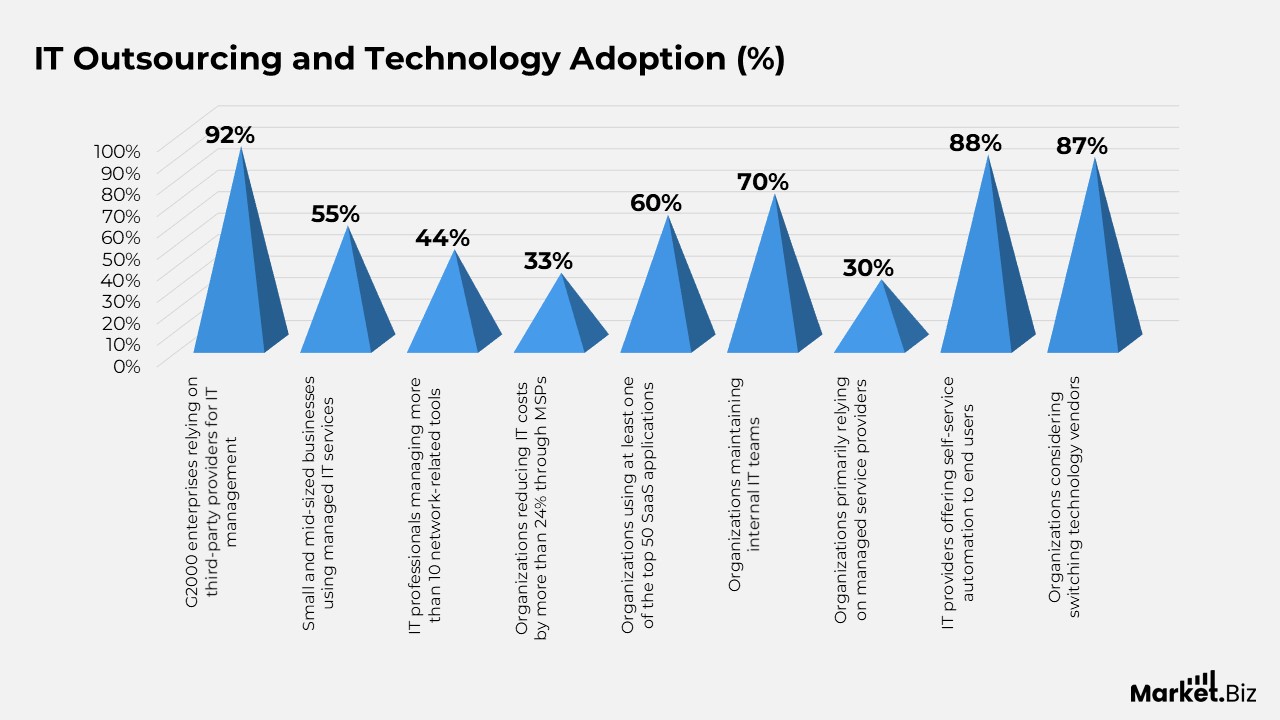

IT Outsourcing and Technology Adoption

- IT outsourcing is deeply embedded among large enterprises, with 92% of G2000 companies relying on third-party providers to manage part or all of their IT requirements.

- Adoption among smaller firms is also substantial, with around 55% of small and mid-sized businesses using managed IT services, though at a lower rate than among large enterprises.

- Network complexity continues to rise, with 44% of IT professionals managing more than 10 network-related tools, while federal government teams often handle 20 or more tools simultaneously.

- Managed IT service users report clear financial benefits, with roughly one-third of organisations working with MSPs reducing IT costs by more than 24%.

- The US technology ecosystem is vast, with over 585,000 tech-focused companies, and the combined valuation of Google, Apple, Amazon, and Meta exceeds US$4 trillion.

- The technology sector has become the largest industry in the US, overtaking healthcare in 2020 after ranking second in 2019.

- Current IT and technology trends are centred on applied AI, electrification, renewables, and future mobility, reflecting a shift from experimental AI to practical deployments.

- SaaS adoption is widespread, with nearly 60% of organizations using at least one of the top 50 SaaS applications.

- Globally, IT delivery models remain mixed, with about 70% of organizations maintaining internal IT teams and 30% depending primarily on managed service providers.

- Automation accessibility is expanding, as 88% of IT providers now offer self-service automation capabilities to end users.

- Vendor mobility is high, with 87% of organizations considering switching technology vendors within the next year.

(Sources: TechReport, Auvik, CompTIA, ChannelPro Network, McKinsey, Stonebranch, Spiceworks)

IT Jobs and Workforce Statistics

- As of October 2024, the US IT sector employed approximately 3.022 million professionals.

- The industry continues to expand rapidly, adding more than 300,000 new tech-related jobs annually in the US.

- IT professionals earn a median annual salary of about US $104,420, more than double the national median income.

- The most in-demand programming languages in job postings include SQL, Java, Python, Microsoft C#, C++, and HTML.

- Employment in IT roles is projected to grow by 11% over the next decade, significantly outpacing overall job growth.

- Workforce diversity remains uneven, with women accounting for about 22.7% of IT professionals and men roughly 77%.

- Around 10% of IT professionals worldwide identify as LGBTQ+.

- The fastest-growing IT roles include information security analysts, software developers, and computer and information research scientists.

- Nearly 25% of US workers are employed in STEM-related occupations, with this share expected to rise further.

- Gender disparity persists in education, as women accounted for only 22.6% of bachelor’s degrees in computer and information science in 2022.

- Key US states driving IT workforce growth include California, Texas, New York, Florida, and Virginia.

- Talent shortages remain a major challenge, with over 60% of companies reporting difficulty finding skilled IT professionals.

(Sources: Statista, Trade.gov, US Bureau of Labor Statistics, Dice, FinancesOnline, Forbes, CompTIA, Spiceworks)

IT Spending and Financial Trends

- Of the global US $1.4 trillion IT budget, about 15% is allocated to managed services, while 22% is allocated to hosted and cloud-based solutions.

- For small businesses, the main drivers of IT budget increases include infrastructure upgrades (57%), security needs (38%), and workforce expansion (32%).

- Hardware spending in small businesses is led by laptops, which account for approximately 24% of IT hardware budgets.

- Applied AI has emerged as a major investment focus, attracting around US $86 billion in equity funding over the past year.

- Electrification and renewables also saw strong investment, with equity funding reaching US $183 billion, alongside a 1% rise in job postings.

- Network automation is gaining traction, with a 24% increase in organizations planning related investments in 2024.

- Global AI-related IT investments are projected to reach US $200 billion by 2025, driven largely by US spending.

- Worldwide IT spending is expected to grow by 7.5% in 2024, signalling continued momentum in digital investment.

- More than 65% of organizations plan to increase IT budgets in 2024, while only 4% expect to reduce technology spending.

(Sources: FinancesOnline, McKinsey, Auvik, Deloitte, Gartner, Spiceworks)

Core Barriers to Digital Transformation

- Data quality stands out as the most critical challenge, with 64% of organisations identifying it as their primary barrier and 77% rating their data quality as average or below acceptable levels, contributing to estimated annual economic losses of trillions of dollars worldwide.

- The global IT skills shortage is reaching a tipping point, with up to 90% of organisations expected to face talent gaps, leading to projected losses of US $5.5 trillion by 2026 due to unfilled digital roles.

- Although 78% of companies have adopted AI, nearly 74% struggle to scale meaningful business value, while 95% of IT leaders report system integration as the key obstacle limiting returns.

- Digital maturity differs sharply by industry, with financial services achieving a digitalisation score of 4.5, compared to just 2.5 in the public sector, resulting in performance gaps of up to 80%.

- Regional disparities continue to widen, with Asia Pacific reaching roughly 45% generative AI adoption, while Europe trails the United States by an estimated 45-70%.

- Governance has overtaken advanced analytics as a top priority, with 62-65% of data leaders prioritising it due to rising regulatory exposure and single-violation penalties reaching €1.2 billion.

- Integrated transformation strategies deliver stronger outcomes: organisations with high integration maturity achieve 10.3x ROI, compared to 3.7x for poorly integrated initiatives.

(Sources: Gartner, McKinsey & Company, IDC, World Economic Forum, European Commission, PwC)

Global Digital Transformation Success and Failure Rates

- Only 35% of digital transformation initiatives achieve their intended objectives, according to an analysis of more than 850 organisations, highlighting persistent execution challenges.

- While success rates have improved modestly from around 30% in earlier assessments, the gap between ambition and results continues to widen as technology ecosystems grow more complex.

- Global digital transformation spending is projected to approach US $4 trillion by 2027, expanding at a 16.2% CAGR, with manufacturing and financial services leading investment momentum.

- Cultural and organizational barriers consistently outweigh technology limitations, with companies prioritizing culture and change management, achieving 5.3x higher success rates than technology-focused efforts alone.

- Across industries, approximately 70% of transformation programs fail to meet expectations, with some studies indicating failure rates as high as 95%, suggesting systemic rather than sector-specific issues.

- Failed transformation efforts cost organizations an estimated 12% of annual revenue through wasted investment and missed growth opportunities.

- Despite widespread investment, only 37.8% of Fortune 1000 companies operate as data-driven organizations, even though 98.8% actively invest in data initiatives each year.

(Sources: Boston Consulting Group, McKinsey & Company, IDC, NewVantage Partners, Deloitte)

Conclusion

The IT statistics underscore a clear trend of rising technology adoption, driven by digital transformation, artificial intelligence, cloud computing, and heightened cybersecurity requirements.

However, the data also reveal that increased spending does not always translate into successful outcomes. Challenges such as poor data quality, integration complexity, talent shortages, and resistance to organizational change continue to limit the impact of technology initiatives across many enterprises.

Sustainable results will depend on how well organizations connect technology investments with people, processes, and governance. Companies that focus on integration, workforce development, and strong data management consistently achieve better returns and greater operational stability. As IT environments continue to evolve, the ability to execute effectively will become just as important as the scale of investment in determining long-term success.

FAQ’s

IT statistics represent quantitative indicators that reflect how information systems, digital infrastructure, and technology resources are adopted, managed, and governed within organizations. They serve as analytical tools to evaluate technological maturity, efficiency, risk exposure, and alignment between IT capabilities and strategic objectives.

IT statistics are essential because they translate complex technological environments into measurable benchmarks. They support comparative analysis across time, industries, and regions, enabling organisations to assess progress, anticipate risks, and evaluate the effectiveness of technology-driven initiatives at both macro and micro levels.

IT statistics provide empirical evidence of how digital transformation unfolds by capturing patterns in investment, adoption, performance outcomes, and failure rates. They help explain why certain transformation efforts succeed or fail by linking technology use to organisational, cultural, and structural factors.

From a theoretical perspective, IT spending and adoption data illustrate the relationship between resource allocation and value creation. They reveal that technology investment alone does not guarantee performance improvement, and that complementary factors, such as integration, governance, and skills development, are critical for realising economic returns.

IT statistics expose systemic issues such as skills shortages, data quality limitations, integration complexity, and governance gaps. By highlighting recurring patterns across organisations and regions, these metrics help explain structural constraints that limit the scalability and sustainability of technology-driven growth.