Introduction

Fraud detection and prevention statistics provide a data-driven overview of how financial crime is evolving across banking, digital payments, e-commerce, insurance, and enterprise systems as transactions increasingly move to online and real-time environments, making fraud more frequent, automated, and complex.

These statistics quantify loss exposure, identify high-risk industries and fraud types such as identity theft, account takeover, and payment fraud, and measure the effectiveness of prevention strategies through indicators such as detection c, false positives, and return on security investments.

They also highlight regional and sector-level differences shaped by digital adoption, consumer behavior, and regulatory frameworks, helping organizations benchmark risk, optimize fraud management tools, strengthen compliance, and support informed decision-making in an interconnected digital economy.

Editor’s Choice

- Over 80% of merchants reported a year-over-year increase in the adoption of real-time payment methods. Reflecting a strong shift toward faster transaction ecosystems.

- Nearly 6 in 10 merchants have integrated tokenization into their payment workflows to enhance transaction security. Improve authorization success and support seamless customer experiences.

- About 80% of merchants report ongoing challenges in effectively leveraging data and technology to improve the accuracy and performance of AI- and ML-driven fraud management tools.

- Close to 90% of merchants are actively deploying anti-first-party misuse strategies. With widespread adoption of compelling evidence to reduce false disputes and chargebacks.

(Source: Visa)

Fraud and Identity Theft Statistics

- In 2024, the FTC recorded total fraud-related losses of USD 12.5 billion. An increase of USD 2.5 billion from 2023, highlighting the accelerating financial impact of fraud.

- Fraud Detection and Prevention Market size is expected to be worth around USD 226.0 Billion by 2033, from USD 36.5 Billion in 2023

- Around 449,032 individuals experienced credit card fraud. With new accounts fraudulently opened using stolen personal information.

- Fraud accounted for 40.0% of all FTC complaints, representing approximately 2.6 million reports. While identity theft followed at 18.0%, or nearly 1.1 million cases.

- Nearly 1 in 5 consumers reported suffering a direct financial loss after falling victim to imposter-related scams.

- Identity theft disproportionately affected younger working-age groups. With 291,807 victims aged 30 to 39 and 187,195 victims aged 20 to 29, indicating higher exposure among digitally active populations.

(Source: Consumer Sentinel Network, Federal Trade Commission)

Global Banking and Digital Payment Fraud Landscape Highlights

- Nearly 1 in 3 adults worldwide were affected by banking-related fraud in 2023, underscoring the extensive global reach of financial crime.

- Online fraud targeting bank customers expanded by 28%. Largely fueled by the growing use of phishing campaigns and counterfeit mobile banking applications.

- Fraud linked to digital wallets, including Apple Pay and Google Wallet, rose by 31%, pointing to rising risks in mobile payment ecosystems.

- The US, UK, and India emerged as the most impacted markets. Together, accounting for financial fraud losses exceeding USD 22 billion globally.

- Cryptocurrency-related fraud incidents increased by 35%. Reflecting heightened exploitation amid expanding decentralised finance adoption.

- About 85% of organizations reported experiencing at least one payment fraud attempt during 2023, highlighting the vulnerability of business transactions.

- Social engineering-based fraud, particularly impersonation- and deception-driven schemes, grew by 19%, signalling a shift toward more targeted, psychologically driven attack methods.

(Source: CoinLaw, Statista)

Financial Institution Fraud Exposure and Risk Trends

- Around 65% of surveyed organizations reported incidents of check-related fraud. Positioning checks as the most exposed and frequently targeted payment method.

- Nearly 47% of Business Email Compromise incidents involved ACH credit transactions, overtaking wire transfers as the most vulnerable payment channel.

- More than 50% of banks, fintech companies, and credit unions observed a rise in business-focused fraud, while over two-thirds also reported an increase in consumer fraud.

- About 35% of financial institutions experienced more than 1,000 fraud attempts over the past year, with 1 in 10 encountering volumes exceeding 10,000.

- Fraud-related activity accounted for approximately 39% of all Suspicious Activity Reports filed, reflecting its dominance among reported financial crimes.

- Nearly 25% of financial organisations disclosed individual fraud losses exceeding USD 1 million. While aggregate consumer losses exceeded USD 10 billion.

- The growing sophistication enabled by generative AI is projected to impose costs of nearly USD 40 billion on banks by 2027, driven by increasingly advanced, scalable fraud attacks.

(Source: CoinLaw, Statista)

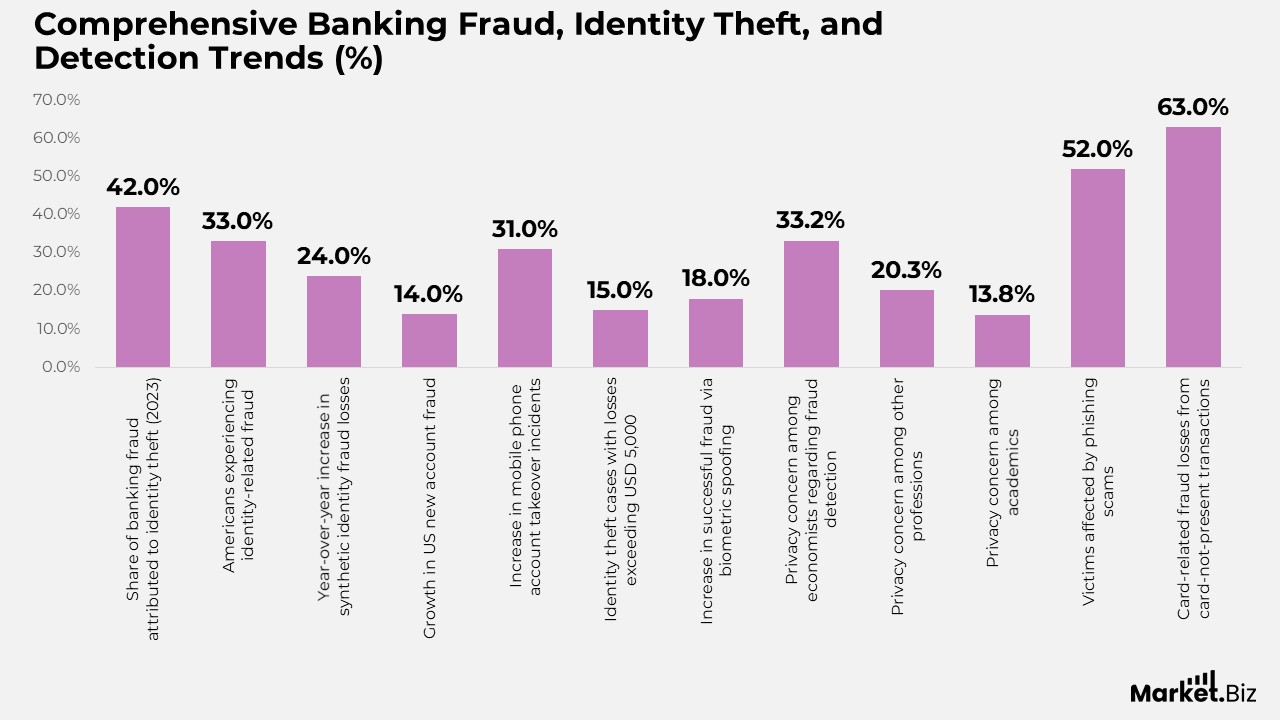

Comprehensive Banking Fraud, Identity Theft, and Detection Trends

- Identity theft remained the leading driver of banking fraud in 2023, accounting for 42% of all reported cases, reinforcing its dominance among financial crime categories.

- Nearly 33% of Americans experienced identity-related fraud, up sharply from 28% in 2022, signalling accelerating consumer exposure.

- Global losses from synthetic identity fraud reached USD 6 billion. Reflecting a 24% year-over-year increase as fraudsters exploited blended real and fake identities.

- In the US, new account fraud increased by 14%, largely due to weaknesses in digital credit card onboarding and verification processes.

- Mobile phone account takeover incidents surged by 31%, highlighting growing risks at the intersection of telecom services and financial access.

- Identity theft victims spent an average of 200 hours resolving fraud-related issues, while 15% incurred direct financial losses exceeding USD 5,000 per case.

- Biometric spoofing techniques enabled fraudsters to bypass authentication controls, resulting in 18% more successful fraud attempts compared to the previous year.

- Privacy concerns about fraud detection were greatest among economists at 33.24%, followed by respondents from other professions at 20.27% and academics at 13.78%, indicating varying levels of trust across professional groups.

- Phishing scams affected 52% of fraud victims, while card-not-present transactions accounted for 63% of card-related fraud losses, confirming the dominance of digital fraud channels.

(Source: CoinLaw, Statista)

Key Drivers Accelerating Digital Banking Fraud Risks

- Digital banking adoption has expanded by 63% since 2020, significantly increasing the attack surface that fraudsters exploit through security gaps.

- Weak or reused passwords accounted for 21% of banking fraud incidents, underscoring the need for stronger authentication and user awareness.

- Large-scale data breaches exposed nearly 290 million records in 2023, supplying criminals with sensitive data for highly targeted financial scams.

- The growing use of deepfake technologies enabled more convincing impersonation attacks, contributing to a 15% rise in identity theft cases.

- Inadequate security controls at smaller financial institutions accounted for 12% of total reported fraud losses, reflecting uneven protection across the banking ecosystem.

- The rapid shift toward remote and digital financial services during the COVID-19 period led to a 42% increase in fraud targeting online banking platforms.

- Emerging economies experienced a 27% surge in financial fraud as digital banking adoption outpaced the implementation of robust security infrastructure.

(Source: CoinLaw, Statista)

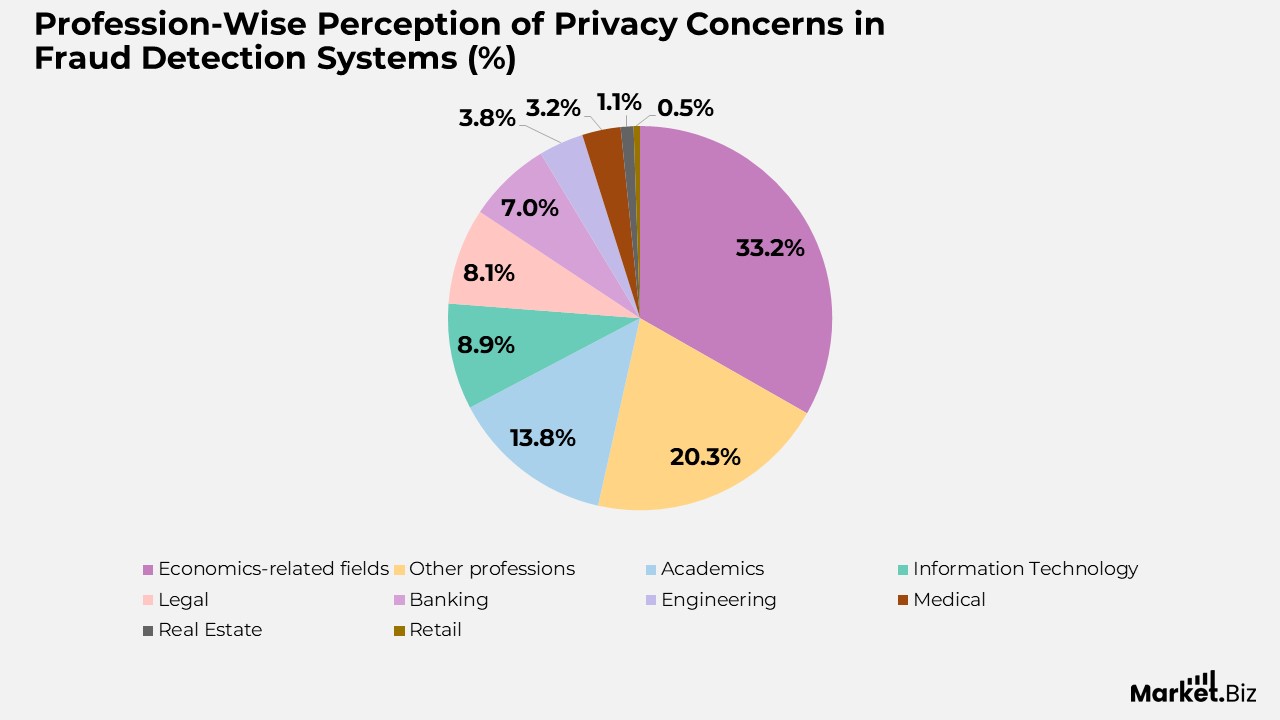

Profession-Wise Perception of Privacy Concerns in Fraud Detection Systems

- Professionals from economics-related fields expressed the highest level of concern, with 33.24% viewing fraud detection systems as intrusive to personal privacy.

- Respondents classified as other professions reported the highest level of concern at 20.27%, making this group the second most sensitive to privacy issues.

- Academics accounted for 13.78% of respondents, reflecting strong awareness of data usage and privacy implications in fraud monitoring.

- Information technology professionals accounted for 8.92%, indicating moderate concern, likely influenced by their technical understanding of data systems.

- The legal sector contributed 8.11%, highlighting a strong focus on regulatory compliance, data rights, and ethical data handling.

- Banking professionals accounted for 7.03%, suggesting greater trust in internal controls and fraud-detection frameworks.

- Engineering professionals reported lower sensitivity levels at 3.78%, despite their technical backgrounds.

- The medical community accounted for 3.24%, reflecting balanced but limited concern about data confidentiality in fraud-detection contexts.

- Real estate professionals represented just 1.08%, while retail sector respondents showed the lowest concern at 0.54%, indicating minimal perceived privacy intrusion.

(Source: CoinLaw, Statista)

Banking Fraud Methods and Their Financial Impact

- Phishing emerged as the most prevalent fraud technique in 2023, impacting 52% of victims through deceptive emails, spoofed messages, and counterfeit banking websites.

- Card-not-present transactions accounted for 63% of total card-related fraud losses, reinforcing the elevated risk associated with remote and online payments.

- Malware and spyware-based attacks increased by 22%, with small- and medium-sized businesses being primary targets due to weaker endpoint security.

- Unauthorized wire transfer fraud resulted in global losses of approximately USD 2 billion, typically stemming from compromised credentials and manipulated payment instructions.

- Check fraud, while gradually declining, still represented 7% of overall fraud cases, driven by the misuse of digital check imaging and remote deposit technologies.

- Account takeover incidents rose by 19%, as fraudsters gained access to legitimate accounts to divert funds and initiate unauthorized transactions.

- Cryptocurrency wallet scams intensified, leading to the theft of nearly USD 3 billion in digital assets, largely through fraudulent investment schemes and fake trading platforms.

(Source: CoinLaw, Statista)

Financial and Trust Impact of Fraud on Institutions and Consumers

- Financial institutions faced an average fraud cost of USD 4.3 million per incident. Including investigation and recovery costs and regulatory penalties.

- Consumer confidence in banking systems declined by 15%. Nearly 4 in 10 individuals expressing hesitation toward adopting new digital banking technologies.

- Legal action related to fraud intensified, as lawsuits filed against banks increased by 18%. Driven by claims of security lapses and institutional negligence.

- Businesses incurred total fraud losses of approximately USD 14 billion. Small enterprises bearing 47% of reported cases, highlighting their heightened vulnerability.

- The financial services industry invested USD 12.6 billion in fraud prevention technologies and services. Reflecting a 20% year-over-year increase in defensive spending.

- Insurance claims linked to fraud damages rose by 26%. Underscoring the broader economic and operational ripple effects on both consumers and organizations.

(Source: CoinLaw, Statista)

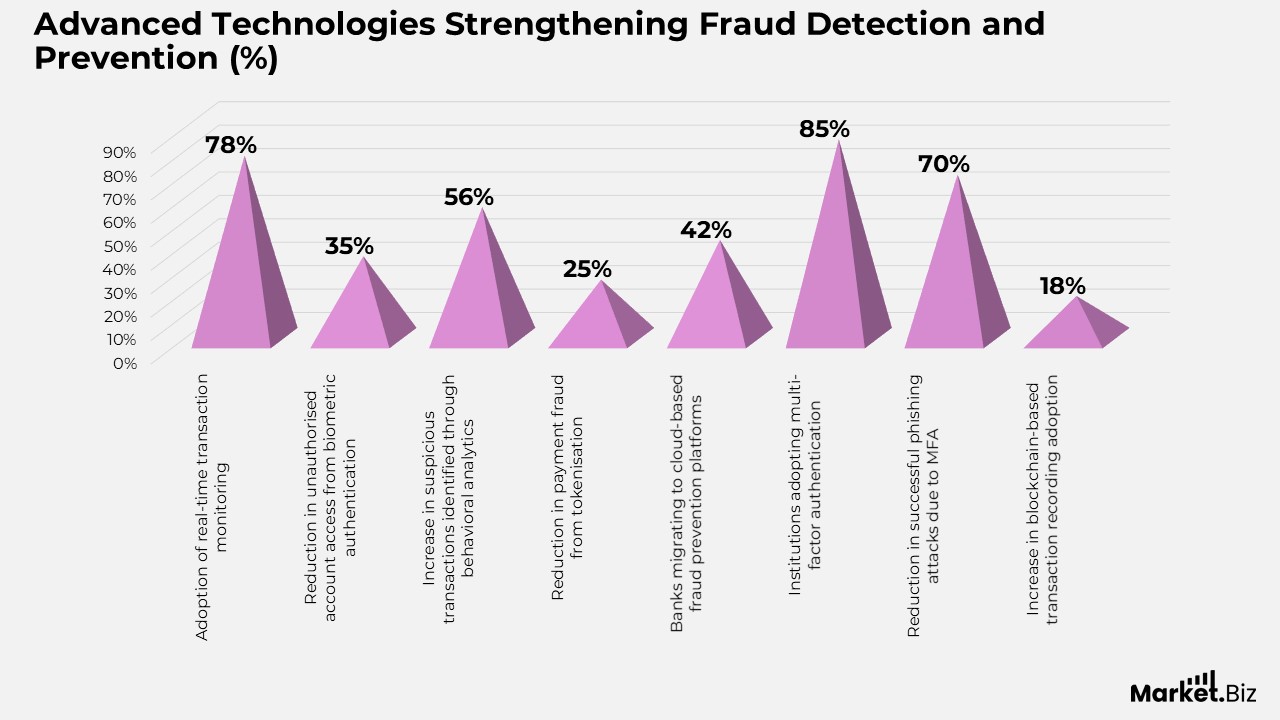

Advanced Technologies Strengthening Fraud Detection and Prevention Statistics

- Real-time transaction monitoring was implemented by 78% of financial institutions in 2023. Enabling faster detection and narrowing the time window for fraudulent activity.

- The adoption of biometric authentication reduced unauthorised account access by 35% compared to traditional password-based security.

- Behavioral analytics solutions identified 56% more suspicious transactions by analyzing user behavior patterns rather than fixed rule sets alone.

- Banks that deployed tokenization reported a 25% reduction in payment fraud, as sensitive card and account data were replaced with secure, non-exploitable tokens.

- Cloud-based fraud prevention platforms gained traction, with 42% of banks migrating to scalable environments to improve resilience and responsiveness.

- 85% of institutions adopted multi-factor authentication, resulting in a 70% decline in successful phishing attacks.

- Blockchain-based transaction recording saw an 18% increase in adoption, providing tamper-resistant ledgers that enhance transparency and trust in financial operations.

(Source: CoinLaw, Statista)

AI and Advanced Analytics Transforming Banking Fraud Prevention

- AI-based fraud detection solutions generated savings of more than USD 20 billion for financial institutions worldwide in 2023, underscoring their growing role in risk mitigation.

- Natural language processing-powered tools successfully flagged over 60% of phishing attempts by analyzing contextual cues and language patterns.

- Machine vision technologies intercepted nearly USD 3 billion worth of forged documents during digital identity verification workflows.

- Banks using predictive analytics identified fraudulent activity 85% faster, enabling early intervention and loss avoidance.

- AI-driven chatbots handled approximately 75% of fraud-related customer queries, significantly reducing the workload on human support teams.

- Institutions with AI-enabled detection platforms recorded a 30% reduction in false positives, minimizing friction for legitimate customers.

- Deep learning models achieved 92% accuracy in detecting high-risk and emerging fraud techniques, strengthening real-time defences.

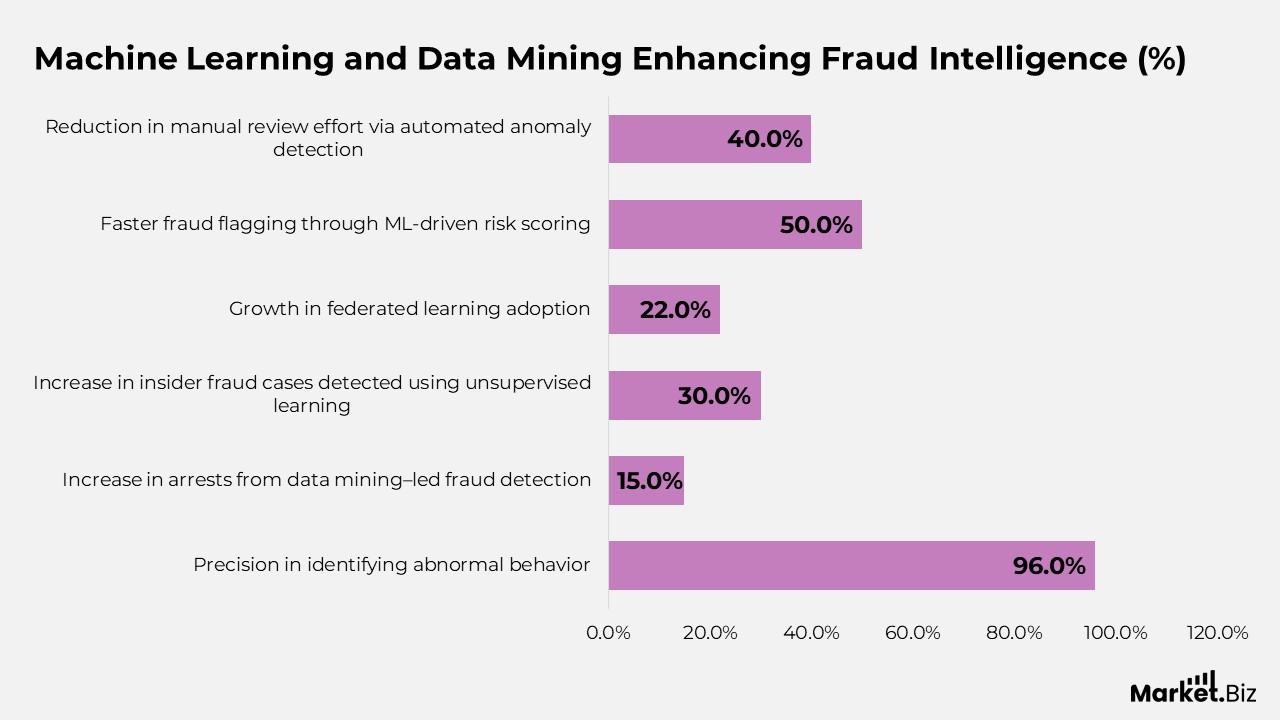

Machine Learning and Data Mining Enhancing Fraud Intelligence

- Machine learning systems processed more than 10 billion transactions in 2023, achieving 96% precision in identifying atypical behavior.

- Data mining techniques uncovered complex fraud patterns, including layered money laundering, contributing to a 15% rise in related arrests.

- Banks applying unsupervised learning detected 30% more insider fraud cases without relying on predefined rules.

- Federated learning adoption increased by 22%, enabling secure data collaboration across institutions while preserving privacy.

- Machine-learning-driven risk-scoring models flagged suspicious activity 50% faster than traditional detection approaches.

- Real-time graph analytics uncovered coordinated fraud networks spanning multiple accounts and regions before large-scale losses occurred.

- Automated anomaly detection reduced manual review effort by 40%, allowing teams to focus on higher-value investigations.

(Source: CoinLaw, Statista)

Fraud Type Distribution Reinforces Need for Real-Time AI Monitoring

- Payment card fraud accounted for 45% of total banking fraud cases.

- Authorised Push Payment fraud accounted for 38% of incidents, highlighting the growing exposure in real-time payment environments.

- Remote banking fraud accounted for 15% of cases, largely driven by credential compromise and unauthorised access.

- Cheque fraud, though minimal in volume, still accounted for 1%, showing legacy channels remain susceptible.

(Source: CoinLaw, Statista)

Regulatory Pressure and Compliance Shaping Fraud Prevention Strategies

- Data protection regulations such as GDPR and CCPA prompted 65% of financial institutions to modernise fraud controls and data governance practices.

- In 2023, the US OCC imposed USD 1.2 billion in fines on banks for inadequate fraud prevention measures.

- KYC-related compliance failures resulted in penalties exceeding USD 800 million globally.

- AML regulations enabled the recovery of USD 4.5 billion in illicit funds through coordinated enforcement efforts.

- Cross-border fraud prevention agreements among 15 countries reduced losses by 20% through real-time information sharing.

- Banks that invested in compliance training achieved a 25% increase in employee adherence to fraud-detection protocols.

- Regulatory sandbox initiatives expanded by 18%, supporting controlled testing and faster deployment of innovative anti-fraud technologies.

(Source: CoinLaw, Statista)

Conclusion

Fraud detection and prevention statistics highlight the accelerating scale, sophistication, and digital nature of financial crime across modern banking and payment ecosystems.

The data make it clear that legacy and reactive controls are no longer adequate, as fraud volumes, attack methods, and financial losses continue to rise. At the same time, the statistics demonstrate tangible progress, with artificial intelligence, machine learning, behavioral analytics, and real-time monitoring delivering faster detection, higher accuracy, and meaningful reductions in fraud losses.

These insights also emphasize the critical role of regulatory oversight, cross-border cooperation, and customer education in strengthening overall fraud resilience. Increased investment in advanced security technologies, robust authentication frameworks, and data governance measures is helping institutions improve compliance, reduce operational friction, and restore consumer confidence.

Collectively, fraud detection and prevention statistics point to the need for ongoing innovation, proactive risk strategies, and coordinated action among financial institutions, regulators, and consumers to stay ahead of increasingly adaptive fraud threats in a digital-first financial environment.

FAQ’s

Fraud detection and prevention statistics consist of quantitative data that track the extent of fraudulent activity, common fraud methods, the financial impact, detection performance, and the effectiveness of security tools and controls across banking, payment systems, and digital channels.

These statistics enable financial institutions to assess their fraud risk, identify emerging threat patterns, compare performance against industry benchmarks, strengthen prevention frameworks, and justify investments that lower losses and regulatory exposure.

Banking-related statistics most often point to payment card fraud, identity-related crimes, account takeover incidents, phishing attacks, authorised push payment fraud, and online or mobile banking fraud as the dominant threats.

Artificial intelligence strengthens fraud detection by processing massive transaction volumes in real time, recognising complex behaviour patterns, reducing false alerts, and identifying new fraud techniques more quickly than traditional rule-driven approaches.

Machine learning supports fraud prevention by continuously analysing transaction behaviour, detecting anomalies early, automatically adapting to new attack methods, and improving accuracy over time without constant manual intervention.