Introduction

Digital Banking Statistics: The rapid advancement of digital technologies has transformed the financial services sector, revolutionizing how consumers engage with banks and financial institutions. The growth of mobile banking applications, AI-powered financial services, and online account management is reshaping the industry to meet the rising demand for convenience, security, and personalized solutions.

Digital banking statistics offer critical insights into trends in customer adoption, transaction volumes, and emerging market opportunities, enabling stakeholders to understand user behavior better, assess market potential, and identify areas for strategic expansion.

This report provides a detailed analysis of the current digital banking landscape, presenting essential data on usage trends, demographic preferences, and technological innovations to help businesses navigate the increasingly digital-focused financial world.

Editor’s Choice

- There are currently 1.75 billion digital banking accounts globally, processing approximately $1.4 trillion annually, which amounts to $2.7 million per minute.

- In the United States, an average of 1,646 physical bank branches have been closing each year since 2018, highlighting the shift to digital-first banking solutions.

- Over 76% of American customers now use mobile banking apps for their financial needs.

- Banks that have embraced digital transformation are seeing significant cost reductions, with operating expenses dropping by 20%–40%, largely due to automation, process optimization, and reduced reliance on physical locations.

- A large majority of consumers (77%) prefer to manage their bank accounts through mobile apps or computers.

- Millennials are the most likely generation to prefer digital banking, with 80% of them opting for digital solutions, while 72% of Generation Z show a preference for traditional banking methods.

- The majority of consumers are satisfied with their banks’ digital services, with 96% rating their mobile and online banking experiences as excellent, very good, or good.

- 83% of customers believe that digital innovations in banking have made banking services more accessible and convenient.

- Among those who do not have an online bank account, 45% prefer branch access, and 42% have security concerns.

- Approximately 4.2% of Americans remain unbanked, meaning they do not have access to any bank accounts.

(Source: American Bankers Association, Bankrate, FDIC, Unblu Inc., TechFin UAB, Statista)

Traditional Banking Usage Statistics

- In 2024, traditional banks globally recorded a remarkable $7.03 trillion in net interest income.

- As of 2024, around 4.5% of people in the U.S. remain unbanked, lacking access to traditional banking services.

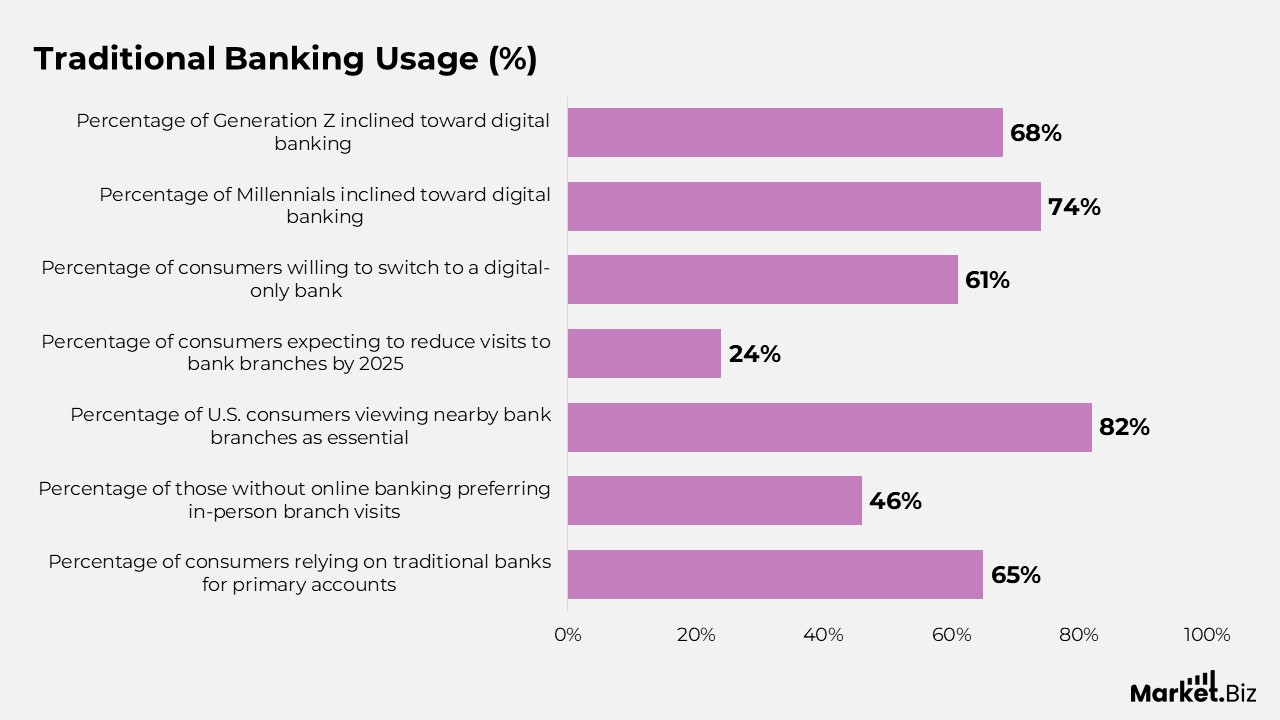

- 65% of consumers still rely on traditional banks for their primary accounts, reflecting their continued preference for established banking institutions.

- Among those without online banking, 46% prefer in-person visits to bank branches for their financial needs.

- 82% of U.S. consumers view having a nearby bank branch as an essential feature for their banking convenience.

- 24% of consumers anticipate reducing their visits to bank branches in 2025, indicating a growing reliance on digital banking.

- In a move toward digital banking, HSBC UK closed 10% of its branches in 2022, cutting its branch network by 69 out of 510 locations.

- 61% of consumers express a willingness to switch to a digital-only bank, reflecting the growing trend of online banking adoption.

- The global market for digital-only banks is projected to reach $2.05 trillion by 2030.

- 74% of Millennials and 68% of Generation Z are more inclined to opt for digital banking over traditional branch-based services.

(Source: G2.com, Inc., Statista)

Digital Banking Usage Statistics

- Bank of America leads the way with over 30 million vigorous mobile app users and more than 40 million online banking customers.

- China, the world’s second-largest economy, is forecasted to reach a $4.6 billion market size by 2026, growing at a 19.9% compound annual growth rate (CAGR) throughout the analysis period.

- China is expected to continue being one of the fastest-growing regions in the global digital banking market. The broader Asia-Pacific market, encompassing countries like India, South Korea, and Australia, is projected to grow to $615.6 million by 2026.

- Canada and Japan are notable markets, with Japan’s digital banking sector projected to grow at an 11% CAGR and Canada at 13.1% from 2021 to 2026.

- In Europe, Germany is expected to see an approximate 14.5% CAGR, while the rest of Europe’s digital banking market is set to reach $5.2 billion by 2026.

- India now boasts around 295.5 million digital banking users, surpassing the U.S. by over 70 million users.

- Net interest income from digital banks is projected to grow at an average annual rate of 6.86% from 2024 to 2029, reaching a total of $2.09 trillion by 2029.

- By 2029, total customer deposits at digital banks are expected to exceed $5.4 trillion globally.

- It is anticipated that by 2025, over 90% of all banking interactions will occur through digital channels worldwide.

- The average digital spending per $1 billion in assets has surged dramatically, from $200,000 in 2022 to nearly $780,000 in 2024, marking a 310% increase over just two years.

(Source: G2.com, Inc., McKinsey & Company, Statista, Dmeand Sage)

Digital Banking Platform Market Size

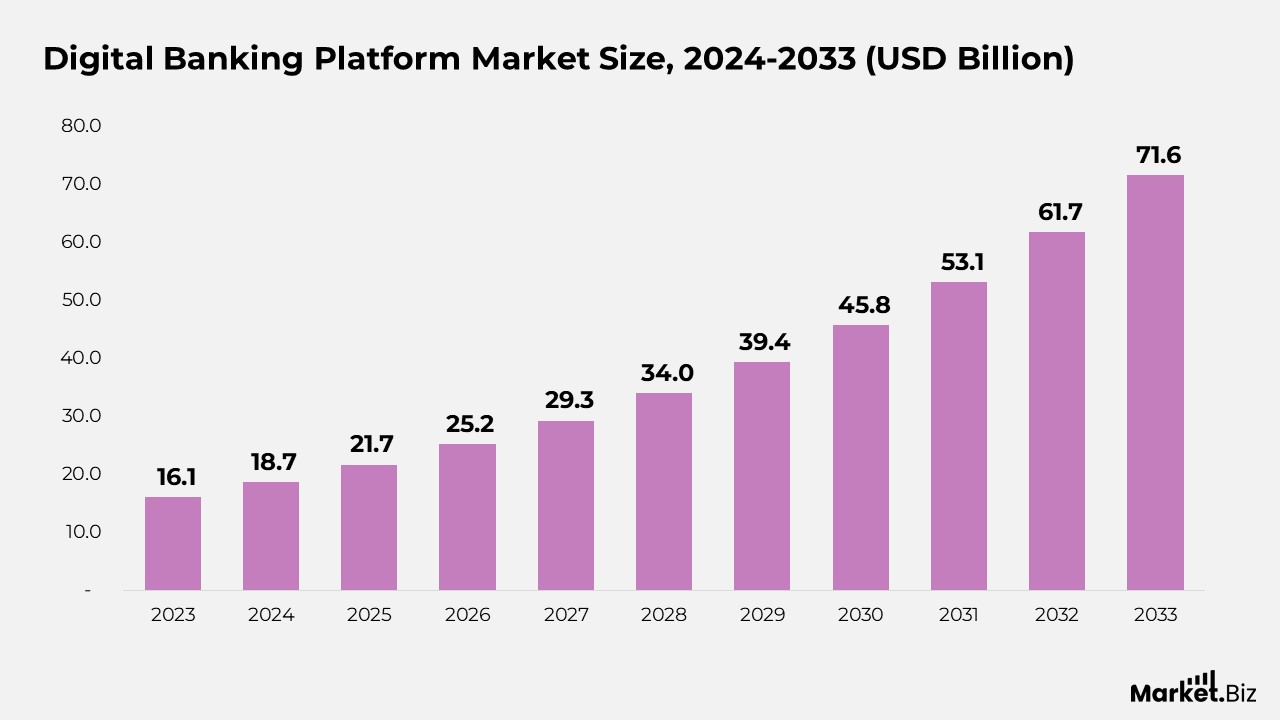

- According to Market.us, the digital banking platform market is expected to rise from $21.7 billion in 2025 to $71.6 billion by 2033, representing a compound annual growth rate (CAGR) of 16.1% from 2024 to 2033.

- The market is fueled by growing demand for personalized banking services and ongoing digital transformation in the financial sector.

- In 2023, Platforms led the by-component segment, capturing more than 58% of the market share, driven by demand for integrated banking solutions.

- In 2023, On-premise solutions dominated the By Deployment segment with 70.3% market share, reflecting the need for enhanced control and security.

- In 2023, Online Banking held the largest share in the by-mode segment, with 78% of the market, due to widespread consumer adoption for convenience.

- In 2023, Investment Banking led the By Type segment with 35% market share, driven by the need for sophisticated digital solutions in global financial markets.

- Asia-Pacific dominated the regional market in 2023, holding 33% of the market share and generating revenues of USD 5.32 billion.

- The Indian Government’s allocation of INR 3,500 crores for the extension of an inducement scheme in FY 2023-24 emphasizes its commitment to promoting digital transactions.

- Of this funding, INR 3,000 crores is dedicated to supporting BHIM-UPI dealings, and INR 500 crores is earmarked for RuPay debit cards, representing a strategic effort to improve digital payment infrastructure and drive wider adoption of digital financial services.

- Additionally, the surge in digital payment transactions, reaching 11,660 crore by December 11, 2023, for FY 2023-24, up from 13,462 crore in the previous fiscal year, year, year demonstrates strong market growth. This trend underscores the increasing consumer dependence on digital banking and highlights the market’s readiness for innovative financial solutions.

(Source: Market.us)

Digital Banking Platform & Services Market Size

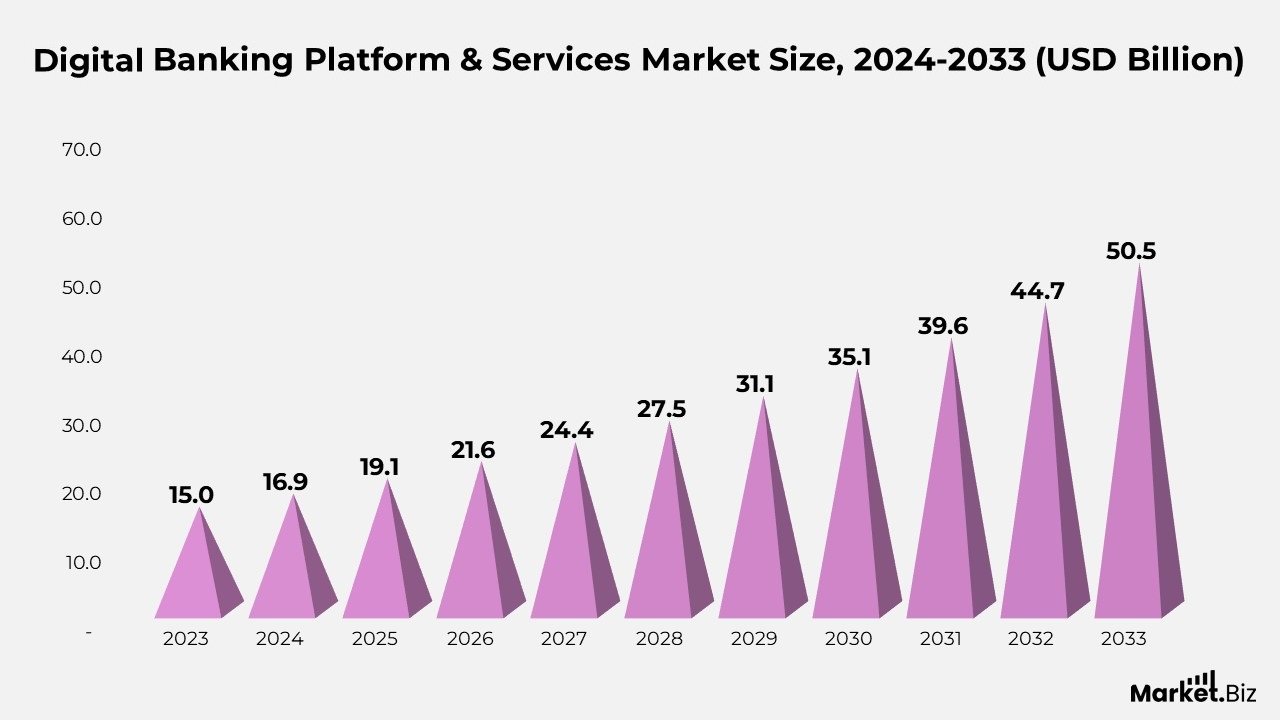

- According to Market.us, the digital banking platform & services market is expected to rise from $16.9 billion in 2024 to $50.5 billion by 2033, representing a compound annual growth rate (CAGR) of 12.9% from 2024 to 2033.

- Market growth is driven by increased smartphone adoption, consumer preference for digital services, and financial institutions’ need for cost-effective customer outreach.

- In 2023, Platforms dominated the Component segment of the Digital Banking Platform & Services Market, capturing more than 62.5% market share, fueled by integrated banking solutions.

- In 2023, on-premises solutions led the Deployment Mode segment, securing more than 68.1% of the market, reflecting financial institutions’ preference for greater control, security, and customization.

- In 2023, Online Banking captured over 77.3% of the Banking Mode segment, reflecting strong consumer preference for secure and robust online solutions.

- In 2023, Retail Banking held the dominant position in the Banking Type segment, with more than 47.0% of the market share, underscoring its role in digital banking transformation for individual consumers.

- Asia-Pacific led the regional market in 2023, accounting for 36.5% of the global market with revenues of USD 5.47 billion, driven by rapid digital transformation and high mobile penetration.

- A recent shift shows that 71% of consumers now prefer managing bank accounts via mobile apps or computers, highlighting the importance of digital interfaces in modern banking.

- Additionally, 97% of consumers rate their mobile and online banking experiences as very good, excellent, or good, indicating high customer satisfaction with these platforms.

(Source: Market.us)

General Digital Banking Statistics

- In 2020, the Far East and China accounted for nearly 800 million digital banking users.

- According to 2021 digital banking data, India leads globally in the volume of real-time online transactions.

- The use of chatbots in customer support could help financial institutions save around $7.3 billion in costs.

- Around 82% of customers report that they haven’t switched banks due to the convenience of digital banking platforms.

- Digital banks offer 1% to 2% higher annual percentage yield (APY) compared to traditional banks.

- By 2025, the United States is expected to have nearly 216.8 million digital banking users.

- 79% of customers agree that digital banking innovations make banking services more accessible.

- Despite the preference for digital banking, 38% of customers still believe that physical bank branches hold importance.

- Among customers without online bank accounts, 46% prefer branch access, and 30% are concerned about security issues.

- As of 2024, approximately 4.5% of people in the U.S. remain unbanked.

- In May 2024, London-based FinTech Revolut announced plans to expand into Asia Pacific, with a focus on Singapore and New Zealand, already serving 600,000 customers in Australia.

- In September 2023, Bank of America launched the “Erica” AI virtual assistant within its mobile app to assist customers.

- In June 2024, First State Bank partnered with Jack Henry to enhance its digital technology and services.

- Digital banking statistics indicate that by 2025, more than 90% of global banking interactions will be conducted through digital channels.

(Source: Kooc Media Ltd, Enterprise Apps Today, Statista G2.com, Inc.)

Online Banking Statistics

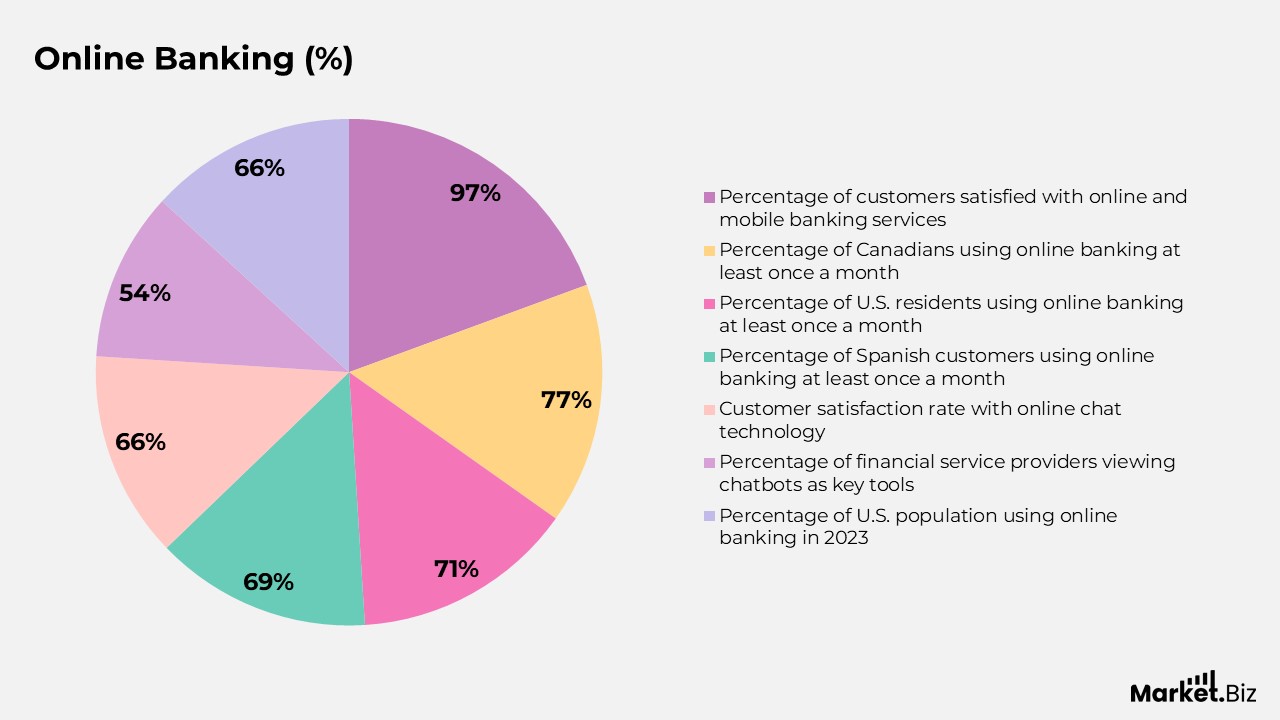

- 97% of customers express satisfaction with their bank’s online and mobile services.

- 77% of Canadians, 71% of U.S. residents, and 69% of Spanish customers use online banking services at least once a month.

- 79% of internet users who lack trust in artificial intelligence (AI) technology are less likely to use online banking, compared to 88% of those who trust AI.

- Online chat technology, which connects customers with human service representatives, boasts a customer satisfaction rate of 66%.

- 54% of financial service providers see chatbots as a key tool to transform the customer experience.

- In 2023, more than 66% of the U.S. population used online banking.

- The use of online banking among older adults grew from 62% in 2018 to 70% in 2022.

(Source: American Bankers Association, Statista)

AI in Banking Statistics

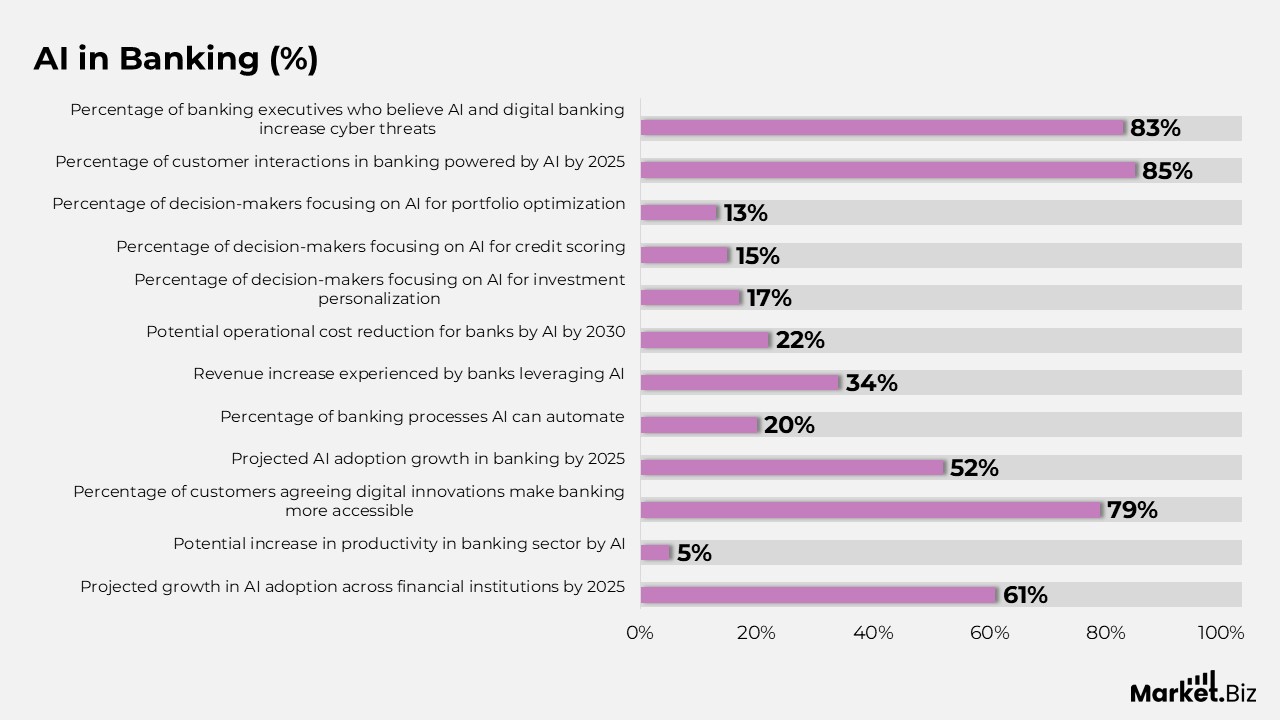

- 61% growth in the adoption of AI across financial institutions is projected by 2025.

- AI has the potential to boost productivity in the banking sector by 5% and reduce global expenditures by up to $300 billion.

- 79% of customers agree that digital innovations are making banking services more accessible and convenient.

- The adoption of AI in banking is expected to grow by 52% by 2025.

- AI is capable of automating 20% of banking and financial processes, significantly enhancing efficiency.

- Banks leveraging AI have experienced a 34% increase in their revenue.

- By 2025, AI could generate up to $140 billion in revenue for the banking industry.

- By 2030, AI has the potential to reduce operational costs for banks by 22%.

- AI-based fraud detection in banking is expected to reach a market size of $68.6 million by 2026.

- 17% of decision-makers are focusing on using AI for investment personalization, 15% for credit scoring, and 13% for portfolio optimization.

- By 2025, 85% of customer interactions in the banking sector are predicted to be powered by AI.

- 83% of banking executives believe that AI and digital banking increase the risk of cyber threats to banks.

(Source: Agile Infoways, Statista, G2.com, Inc.)

Digital Banking Security Statistics

- In 2023, the Reserve Bank of India (RBI) reported bank frauds totaling over 302.5 billion Indian Rupees.

- As digital transactions continue to surge, traditional fraud and scam detection services are struggling to keep pace with the modern cybersecurity challenges faced by banking institutions.

- Merchant losses due to fraud in online payments are projected to exceed $362 billion globally between 2023 and 2028, with losses expected to reach $91 billion by 2028.

- 57% of Americans express trust in financial institutions to safeguard their data.

- 30% of customers without online bank accounts are concerned about security risks associated with digital banking.

- In 2022, individuals reported nearly $8.8 billion in financial fraud losses, reflecting a 30% increase compared to 2021.

- 62% of all new accounts opened by criminals in 2022 were financial accounts, making these new accounts 9.5 times riskier than older, established accounts.

- 67% of victims of Account Takeover (ATO) scams found that their compromised data was used for unapproved purchases.

- 87% of shoppers prioritize accessibility over security when choosing financial services.

- In 2023, U.S. users ranked the ability to detect breaches in their Social Security number as the most valuable feature of mobile banking.

(Source: PYMNTS, Reserve Bank of India, Statista, G2.com, Inc., Identity Theft Resource Center)

Traditional Banking vs. Digital Banking

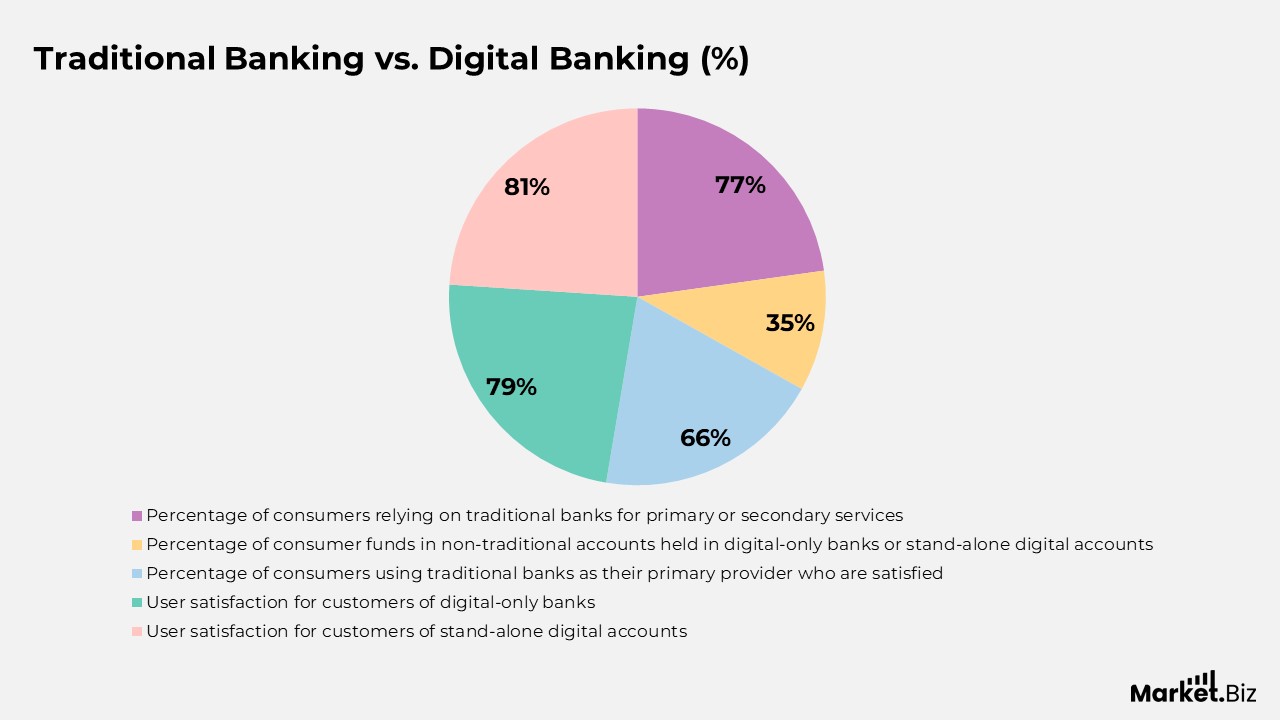

- 77% of consumers rely on traditional banks for their primary or secondary financial services.

- 35% of consumer funds in non-traditional accounts are held in digital-only banks or stand-alone digital accounts, out of the 43% of total consumer funds in such accounts.

- Among the 65% of consumers who use traditional banks as their primary provider, only 66% express satisfaction with their banking experience.

- User satisfaction rises to 79% for customers of digital-only banks (21% of users) and 81% for those with stand-alone digital accounts (7% of users).

(Source: Statista, G2.com, Inc., DemandSage)

Digital Banking User Statistics

- 59% of individuals believe that digital banking should offer easy-to-use tools and resources to help manage finances effectively.

- The global number of digital banking users is expected to reach approximately 3.6 billion by 2024.

- According to 2023 Digital Banking Statistics, the U.S. will have around 208 million digital banking users, projected to grow to 212.8 million by 2024, and 216.8 million by 2025.

- Around 60% of people reported using digital wallets like PayPal or Apple Pay at least once in the past month.

- In 2023, nearly 48% of U.S. consumers primarily relied on mobile banking for their financial transactions.

- 81% of people used a mobile device for banking in the last month, with 90% of users aged 18 to 44 actively engaging with mobile banking.

- By 2024, 59% of individuals will have used their mobile phones to manage bank accounts at least three times in the last month.

- 60% of customers now use mobile apps for money or payment transfers, up from 34% just four years ago.

- The top feature in mobile banking is the ability to lock lost cards (83%), followed by mobile check deposits (79%).

(Source: Statista, G2.com, Inc., Kooc Media Ltd.)

Conclusion

The digital banking sector is rapidly evolving, fueled by technological advancements, shifting consumer expectations, and an increasing demand for convenient, secure, and personalized financial services. As recent statistics reveal, the global adoption of digital banking is on the rise, with billions of users turning to mobile apps, digital wallets, and online platforms to manage their finances.

This transition to digital-first solutions is transforming how consumers interact with financial institutions, creating both challenges and opportunities for banks to innovate and optimize their offerings. With a growing emphasis on convenience and accessibility, banks are focused on improving their digital services, from mobile banking capabilities to AI-powered tools and enhanced security measures.

As digital banking usage and transaction volumes continue to expand, the industry is set for sustained growth. Financial institutions that embrace digital transformation will be well-positioned to meet customers’ evolving needs, lower operational costs, and maintain competitiveness in a rapidly changing financial landscape.

FAQ’s

The increasing consumer desire for convenience largely drives the growth of digital banking, the widespread use of smartphones and internet connectivity, the global trend toward a cashless society, and the financial sector’s need to optimize costs and improve efficiency through digital solutions.

Digital banking trends disrupt traditional banking models by reducing the reliance on physical branches, pushing financial institutions to evolve their services to cater to a tech-savvy, convenience-focused customer base. This transformation requires significant investment in cybersecurity and digital infrastructure to ensure secure online transactions.

Mobile banking is essential because it provides consumers with immediate access to their financial information, enabling real-time transactions, payments, and financial management anytime, anywhere. This shift aligns with the growing consumer demand for on-demand services, making mobile banking a critical tool for banks to stay competitive in a digital-first landscape.

AI is poised to revolutionize digital banking by automating routine processes, enhancing fraud detection, customizing financial products, and improving customer service. By analyzing large volumes of data, AI helps banks deliver more efficient and personalized banking experiences, improving operational efficiency and customer satisfaction.

Consumer trust is crucial for the widespread adoption of digital banking. Trust is built on perceptions of security, reliability, and convenience. When banks invest in secure technologies, user-friendly interfaces, and transparent data protection, they can boost trust, leading to greater adoption. Conversely, concerns about data privacy and cybersecurity may hinder adoption if not adequately addressed.