Introduction

Buy Now, Pay Later in E-commerce Statistics: Buy Now Pay Later (BNPL) has emerged as a transformative payment model within the global e-commerce ecosystem, reshaping how consumers finance online purchases by allowing them to split costs into short-term, often interest-free instalments at checkout. Its rapid adoption reflects the expansion of digital commerce, mobile shopping, and embedded finance, alongside shifting consumer preferences toward transparent, low-commitment credit options.

Younger shoppers, particularly millennials and Gen Z, increasingly favour BNPL for its ease of use, predictable repayment terms, and reduced reliance on traditional credit cards. At the same time, merchants adopt it to improve conversion rates, increase average order values, and reduce cart abandonment.

As competition among BNPL providers grows and regulatory oversight increases, BNPL in e-commerce statistics plays a critical role in quantifying adoption trends, transaction volumes, user demographics, and regional penetration, offering a data-driven perspective on how this payment model is influencing consumer behavior, merchant performance, and the evolving structure of digital retail finance.

Editor’s Choice

- Global adoption of Buy Now, Pay Later is expected to exceed 900 million users by 2027, highlighting the rapid expansion of instalment-based digital payments worldwide.

- Gen Z shows a strong preference for Buy Now, Pay Later, with an adoption rate of 36.8 per cent, driven by demand for flexible, transparent payment options.

- Buy Now Pay Later currently ranks 5th among e-commerce payment methods, reflecting its growing acceptance among online shoppers.

- Nearly 47% of Buy Now Pay Later users report using this payment method for most of their online purchases, indicating strong dependence and regular use.

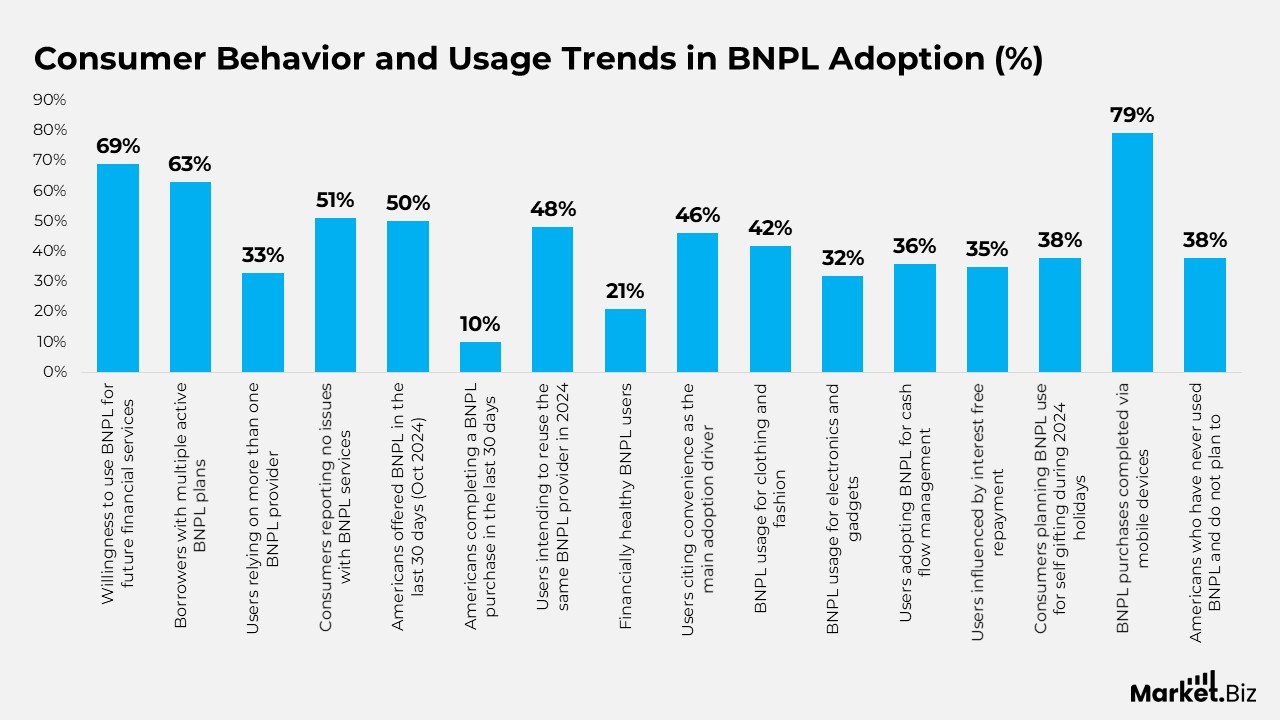

Consumer Behavior and Usage Trends in BNPL Adoption

- Around 69% of consumers indicate a willingness to use Buy Now Pay Later solutions for future financial and payment-related services, signalling long-term confidence in the model.

- Nearly 63% of BNPL borrowers manage multiple active BNPL plans at the same time, while 33% spread their usage across more than one BNPL provider.

- About 51% of US consumers report never having had any issues with Buy Now Pay Later services, indicating stable user experiences.

- An industry survey from October 2024 found that 50% of Americans received a BNPL payment offer in the previous 30 days, and 10% completed a pay-later purchase during that period.

- In 2024, nearly 48% of BNPL users stated that they definitely intended to reuse the same provider for future purchases, indicating strong brand loyalty.

- Financial health analysis shows that 21% of BNPL users fall into the financially healthy category, achieving the highest satisfaction score of 731 out of 1000.

- Convenience remains a major driver, with 46% of users choosing BNPL because it simplifies payments and improves checkout ease.

Moreover

- By category, 42% of consumers used BNPL for clothing and fashion purchases, followed by 32% for electronics and gadgets.

- Cash flow management motivates 36% of BNPL users, who use instalment payments to spread expenses over time.

- Interest-free repayment remains influential, with 35% of users citing protection from interest charges as a key adoption factor.

- During the 2024 holiday season, 38% of consumers planned to use pay-later options specifically for self-gifting purchases.

- Holiday spending data shows that consumers spent 18.2 billion dollars via BNPL in 2024, including a record 991.2 million dollars on Cyber Monday alone.

- Mobile commerce accounted for 79.12% of BNPL purchases during the holiday period.

- Despite growth, 38% of Americans report they have never used BNPL and do not expect to adopt it in the future.

- The adoption of BNPL significantly influenced buying behaviour, increasing purchase likelihood from 17% to 26% among users.

(Source: Digital Silk)

BNPL Providers and Platform Adoption Statistics in the United States

- PayPal accounts for 43.08% of the global market share in payment processing technologies, reflecting its strong presence across payment gateways and Buy Now Pay Later services.

- In the United States, 68.1% of consumers use PayPal’s Buy Now, Pay Later offering, making it one of the most trusted BNPL solutions in the market.

- Klarna is widely adopted across the US digital retail landscape, with 277,534 websites integrating it as their Buy Now Pay Later payment option.

- By the first quarter of 2025, Klarna reported reaching 100 million active users, highlighting its rapid global user base expansion.

- At the beginning of 2025, Klarna generated revenue of $ 701 million, underscoring its strong transaction volumes and merchant adoption.

- Afterpay supports Buy Now Pay Later transactions for 52,330 online retailers across the United States, reflecting its broad merchant penetration.

- Affirm enables BNPL functionality on 18,532 US-based websites, positioning it as a key player in the domestic installment payments market.

- At the start of 2025, Affirm reported 21.9 million active users, supported by steady consumer adoption and repeat usage.

- Affirm recorded a 36% revenue increase in early 2025, reaching $ 783 million, indicating strong growth momentum.

- Sezzle serves as the Buy Now, Pay Later provider for 22,346 online businesses in the United States, reinforcing its role among mid-sized and emerging e-commerce merchants.

(Source: Digital Silk, Statista)

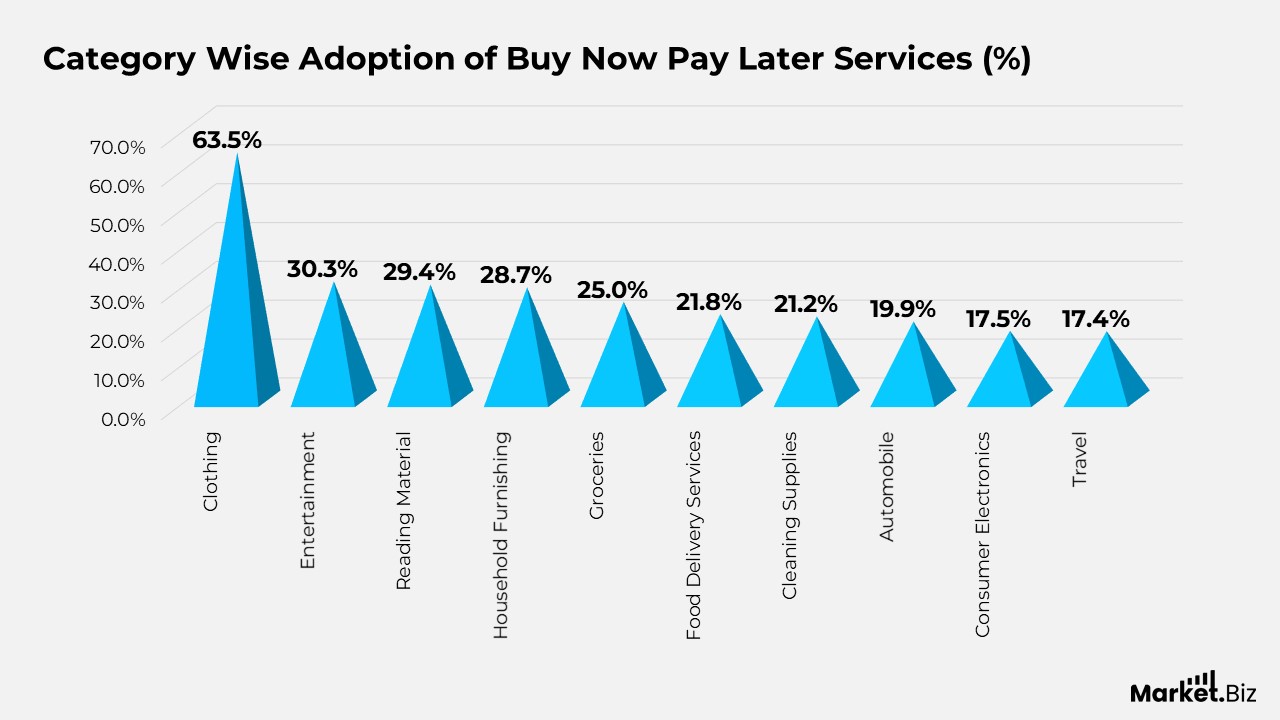

Category-Wise Adoption of Buy Now Pay Later Services

- Clothing accounts for the largest share of Buy Now Pay Later transactions, at 63.5% of total BNPL transactions across consumer categories.

- Entertainment-related purchases follow, with Buy Now Pay Later applied in 30.3% of spending within this segment.

- Reading materials, including books and digital content, capture a BNPL usage share of 29.4%, reflecting steady adoption for low- to mid-value purchases.

- Household furnishing products account for 28.7% of BNPL usage, driven by the need to spread the cost of home-related expenses.

- Groceries show growing acceptance of Buy Now, Pay Later, representing 25.0% of category-level usage.

- Food delivery services account for 21.8% of BNPL transactions, underscoring their expansion into everyday consumption.

- Cleaning supplies record a BNPL usage share of 21.2%, indicating increasing reliance on flexible payments for recurring household needs.

- Automobile-related purchases account for 19.9% of Buy Now Pay Later usage, covering accessories, maintenance, and related services.

- Consumer electronics account for 17.5% of BNPL adoption, reflecting selective use for higher-value discretionary items.

- Travel-related bookings and services account for 17.4% of Buy Now Pay Later usage, underscoring instalment-based payment preferences for experience-driven spending.

(Source: Digital Silk, Statista)

Geographic Distribution of BNPL Market Adoption

- Australia has the strongest Buy Now Pay Later presence, accounting for 15% of the market share among listed countries.

- Belgium and Finland follow closely, each contributing 13% to the overall BNPL market penetration.

- Denmark also represents a significant share, with Buy Now Pay Later adoption reaching 12%.

- The Netherlands records a BNPL market share of 11%, reflecting steady acceptance across online retail platforms.

- New Zealand also holds an 11% share, supported by widespread consumer familiarity with instalment-based payments.

- The United Kingdom reports a comparatively lower share at 7%, indicating more moderate BNPL adoption relative to other developed markets listed.

(Source: Digital Silk, Meetanshi Technologies LLP)

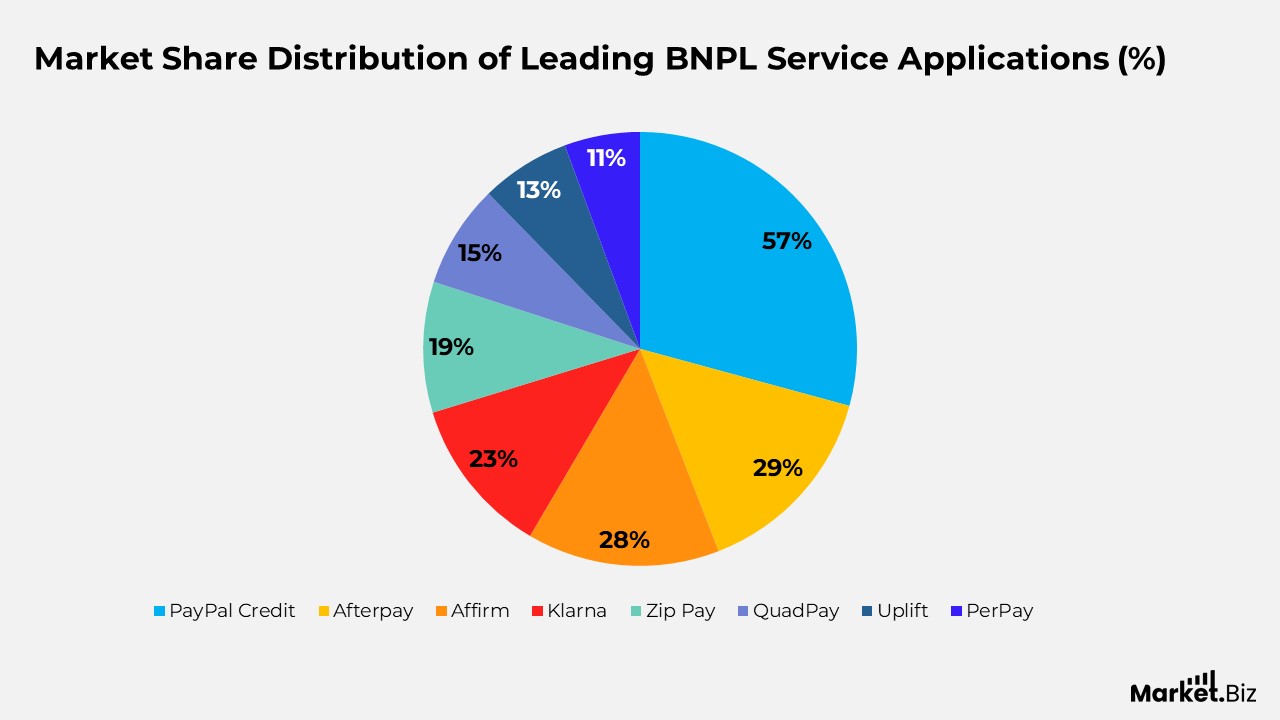

Market Share Distribution of Leading BNPL Service Applications

- PayPal Credit holds the largest share of Buy Now Pay Later app usage, accounting for 57% of total BNPL app usage.

- Afterpay follows as a major player, capturing 29% of the market through strong merchant partnerships and consumer recognition.

- Affirm secures a significant position with a 28% share, supported by its presence in high-value, branded retail purchases.

- Klarna accounts for 23% of BNPL applications, driven by broad adoption across the fashion and lifestyle e-commerce segments.

- Zip Pay accounts for 19% of the BNPL application market, reflecting steady uptake in instalment-based payment transactions.

- QuadPay contributes a 15% share, indicating moderate but consistent consumer engagement.

- Uplift holds a 13% market share, largely supported by travel and experience-focused purchases.

- PerPay captures 11% of BNPL application usage, appealing to consumers seeking structured repayment plans.

(Source: Digital Silk, Meetanshi Technologies LLP)

Global Scale and Consumer Impact of Buy Now Pay Later Adoption

- More than 86 million people in the United States actively use Buy Now, Pay Later, positioning it as a mainstream payment option rather than an alternative.

- Buy Now Pay Later currently supports nearly 1 in 20 e-commerce transactions worldwide, underscoring its growing role in online checkout behaviour.

- Close to 40% of BNPL users missed at least one repayment in the past year, suggesting increasing financial pressure among certain user groups.

- Adoption of Buy Now, Pay Later among older adults in the United Kingdom has doubled, demonstrating that its use now extends well beyond Gen Z consumers.

- By the end of 2025, more than 50% of consumers in the United States are expected to have used Buy Now Pay Later at least once.

- Global BNPL activity exceeded 2 billion transactions in 2023, with transaction volumes continuing to rise rapidly.

- During the 2024 holiday season, Buy Now Pay Later contributed to 18.2 billion in consumer spending, significantly influencing seasonal shopping patterns.

(Source: Digital Silk, Meetanshi Technologies LLP)

Growth of Buy Now Pay Later Usage Across Generations

- Gen Z continues to lead Buy Now Pay Later adoption, with usage rising from 36.8% in 2021 to 46.5% in 2023, and reaching 47.4% by 2025, reflecting a total increase of 10.6 percentage points.

- Millennials show strong growth in BNPL usage, increasing from 30.3% in 2021 to 39.5% in 2023, and further to 40.6% in 2025, representing a 10.3 percentage-point increase over the period.

- Gen X demonstrates accelerating adoption, with BNPL usage expanding from 17.2% in 2021 to 26.3% in 2023, and reaching 30.9% by 2025, marking the highest growth at 13.7 percentage points.

- Baby Boomers show steady but notable growth in BNPL adoption, rising from 6.2% in 2021 to 12% in 2023 and reaching 14.8% by 2025, an increase of 8.6 percentage points.

(Source: Digital Silk, Meetanshi Technologies LLP)

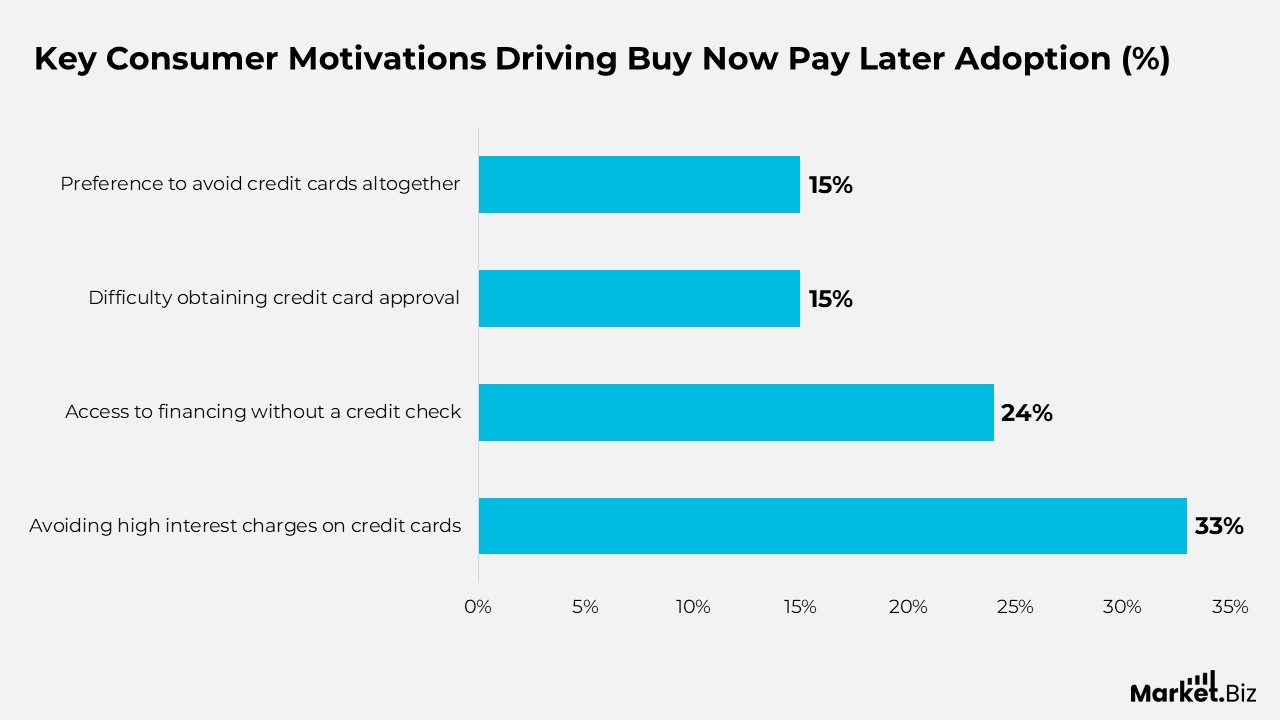

Key Consumer Motivations Driving Buy Now Pay Later Adoption

- About 33% of consumers choose Buy Now, Pay Later to avoid high-interest charges associated with traditional credit cards.

- Nearly 24% of users rely on Buy Now, Pay Later because it provides access to short-term financing without undergoing a formal credit check.

- Around 15% of consumers turn to Buy Now Pay Later due to challenges in securing approval for conventional credit cards.

- Another 15% of users deliberately avoid using credit cards altogether and prefer Buy Now Pay Later as their primary payment alternative.

(Source: Digital Silk, Meetanshi Technologies LLP)

Evolving Consumer Behavior and Usage Patterns in Buy Now Pay Later Services

- The share of consumers using Buy Now Pay Later rose sharply to 38%, up from 37.65% in July 2020, marking close to a 50% increase in adoption within less than a year.

- BNPL usage expanded most rapidly among younger and older age groups, with growth of 62% among consumers aged 18 to 24 and 98% among those aged 55 and above between July 2020 and March 2021.

- Among consumers who have never used BNPL, 53% report that they are at least somewhat likely to try it within the next year, indicating strong future adoption potential.

- Since the pandemic, 41% of BNPL users have increased their use to preserve cash for emergencies, while 25% have turned to BNPL after experiencing income loss.

- Payment risk remains visible, as 31% of BNPL users have missed a payment or paid a late fee, and 36% expect they may fall behind on a payment within the next year.

- Perception data shows 62% of BNPL users believe these services could replace credit cards, although only about 25% actively want that outcome.

Moreover

- PayPal leads provider usage, with 43% of BNPL users reporting they have used PayPal’s pay-later options.

- Budget constraints drive adoption, as 45% of users rely on BNPL to make purchases they could not otherwise afford upfront.

- Electronics remain the most common BNPL purchase category, used by 48% of consumers.

- Usage frequency data shows that 36% of BNPL users use the service at least once per month.

- Consumers aged 18 to 24 are most likely to carry higher BNPL obligations, frequently paying $250 or more per month.

- Consumer awareness continues to improve, with understanding of BNPL increasing by nearly 50% compared to the previous year.

- Preference trends show that 61% of BNPL users prefer payment options offered directly by retailers rather than those provided by third-party providers.

(Source: Digital Silk, Meetanshi Technologies LLP)

Conclusion

Buy Now Pay Later in E-commerce Statistics: In e-commerce highlight the growing importance of instalment-based payment options in the evolution of online retail. The data illustrates how BNPL contributes to higher conversion rates, larger basket sizes, and stronger purchase engagement, particularly among younger, mobile-first consumers.

At the merchant level, statistical trends indicate that BNPL is becoming a key tool for customer acquisition and checkout optimisation in competitive digital marketplaces.

As regulatory oversight strengthens and providers enhance credit controls and disclosure standards, BNPL metrics will be critical for assessing repayment behavior, risk exposure, and long-term viability. Overall, BNPL statistics offer a clear, data-driven understanding of how flexible payment models continue to shape consumer spending patterns and redefine the structure of e-commerce finance.

FAQ’s

BNPL in e-commerce is a payment option that allows online shoppers to split the total purchase value into short-term instalments, often interest-free, at the point of checkout. E-commerce statistics track how frequently this option is used, transaction volumes, repayment behaviour, and its impact on online retail performance.

BNPL statistics help quantify consumer adoption trends, changes in purchasing behaviour, and the impact of instalment payments on conversion rates and average order values. These insights help merchants, platforms, and policymakers understand how BNPL influences digital commerce growth and financial risk.

E-commerce statistics consistently show higher BNPL adoption among millennials and Gen Z consumers, driven by a preference for flexible payments, transparency, and limited reliance on traditional credit. Younger demographics account for a significant share of BNPL transactions in online retail.

Statistical analysis indicates that BNPL contributes to lower cart abandonment, higher checkout completion rates, and increased basket sizes. Merchants use BNPL data to evaluate its effectiveness as a tool for boosting sales and improving customer acquisition.

BNPL statistics suggest partial substitution rather than full replacement of credit cards. While BNPL gains share in certain product categories and price ranges, credit cards remain dominant for larger purchases, rewards-driven spending, and cross-border transactions.