Introduction

Microfinance Statistics: Microfinance serves as a transformative financial instrument aimed at empowering marginalised individuals and communities by providing customised services such as micro-savings, microcredit, and micro-insurance.

Its historical development has progressed from informal savings groups to contemporary microfinance institutions. This evolution has led to worldwide acknowledgement, notably through Muhammad Yunus and the Grameen Bank’s receipt of the Nobel Peace Prize.

It acts as a guide for policymakers, financial institutions, and development organisations to assess impact, make informed choices, and promote financial inclusion and poverty alleviation.

Microfinance statistics indicate a thriving global market that offers small loans, savings, and insurance to impoverished individuals, with over 200 million borrowers (predominantly women) served by 2020, thereby advancing financial inclusion, entrepreneurship, and poverty alleviation.

However, significant disparities persist, particularly in developing countries, where it empowers women and stimulates local economies, with India experiencing rapid growth through initiatives such as Self-Help Groups (SHGs).

Essential metrics monitor borrower counts, loan portfolio sizes, gender distribution (mainly female), and market expansion, underscoring its vital role in closing the financial gap for underserved communities.

Editor’s Choice

- In 2023, 25% of microfinance loans were distributed via digital channels, highlighting the swift advancement of digital financial platforms.

- The global microfinance sector achieved a valuation of approximately US$279.22 billion in 2024, signifying the substantial size and established nature of the industry.

- In 2018, approximately 139.9 million people benefited from MFI services, representing a notable increase from the 98 million borrowers recorded in 2009.

- In 2016, a total of 4,506 microloans were sanctioned, amounting to $61.2 million.

- Around 94% of those who qualify for the bank’s loans are women.

- As of the end of March 2021, there were 6,841 micro-credit companies functioning within China.

Historical Facts about Microfinance

- Credit cooperatives and savings banks were established to address the financial requirements of the working-class and rural communities in 19th-century Europe.

- Credit unions and rural banks started providing financial services to individuals in underserved regions in the 20th century.

- The 1970s heralded the advent of modern microfinance, spearheaded by trailblazers such as Muhammad Yunus and the Grameen Bank, which offered small loans to those in poverty.

- During the 1980s and the 1990s, microfinance gained international recognition, with organisations like FINCA and ACCION expanding their outreach.

- In the 2000s, improved scrutiny led to the establishment of regulations and responsible lending practices within the microfinance sector, which also began to include savings, insurance, and remittance services.

- Ultimately, in the 21st century, advancements in digital technology and fintech innovations revolutionised microfinance, empowering broader access to financial services.

General Microfinance Statistics

- In 2023, 25% of microfinance loans were distributed via digital channels, highlighting the swift advancement of digital financial platforms.

- Women account for 70% of all microfinance clients, which underscores the positive impact of loans on the establishment and expansion of over 100 million female entrepreneurs.

- Businesses led by women and supported by MFIs have shown a growth rate that is 12% greater than that of their male counterparts.

- Financial literacy programs have reached over 15 million women and 10 million borrowers globally, leading to improved financial management and empowerment.

- Microfinance lending has the potential to generate over 20 million jobs worldwide, particularly in the most impoverished regions and rural areas.

- Clients aged under 35 years make up 65% of the total client base, indicating a strong engagement of young entrepreneurs in the business sector.

- Half of the borrowing clients reside in rural areas, with 80% of them belonging to the low-income demographic.

- Agricultural loans represent 30% of the total microfinance offerings in the market, thereby aiding the farming community in their fight for sustenance amid the food crisis.

- It is anticipated that digital lending in small amounts will increase by 30% globally by 2024, with Kenya and India being the primary contributors.

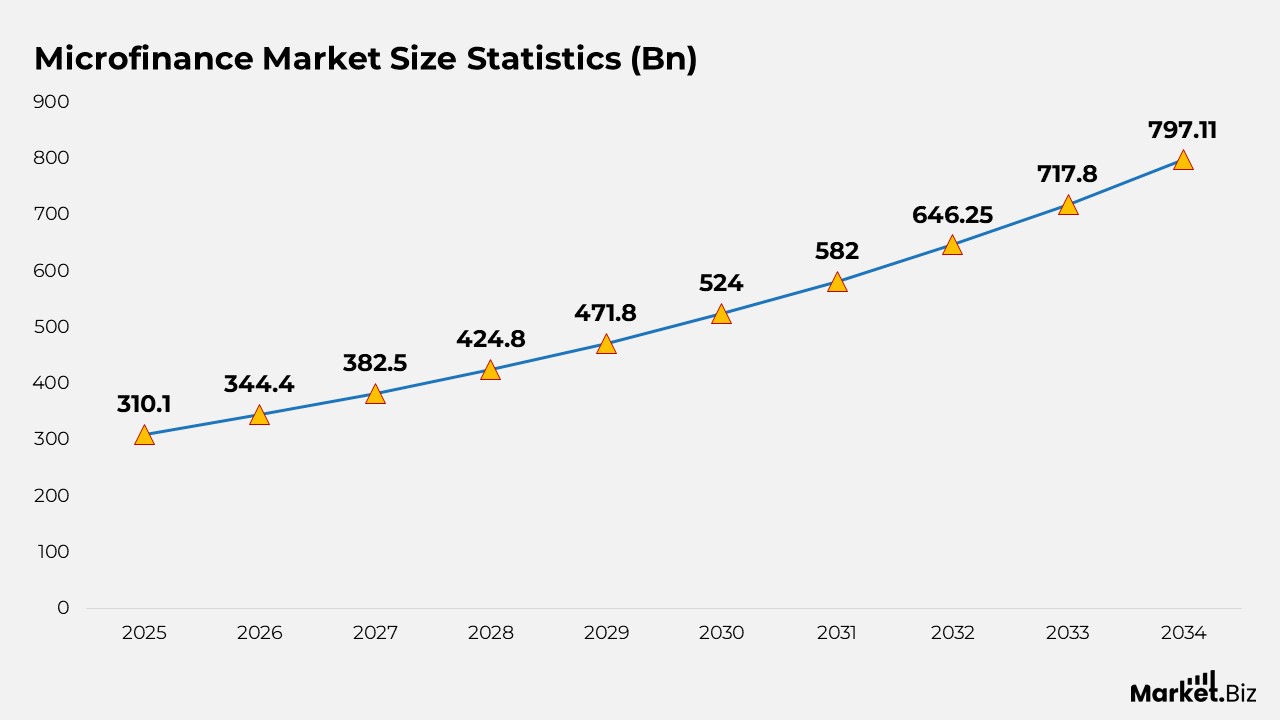

Microfinance Market Size Statistics

- The global microfinance sector achieved a valuation of approximately US$279.22 billion in 2024, signifying the substantial size and established nature of the industry.

- The market is anticipated to grow further to around US$310.10 billion in 2025, reflecting the ongoing demand for small loans and financial inclusion initiatives in developing and emerging economies.

- Conversely, analysts predict a potential market size of US$797.11 billion by 2034, nearly tripling the market’s size within a span of nine years.

- This long-term growth translates to a compound annual growth rate (CAGR) of roughly 11.06% from 2025 to 2034.

- In other words, the market is expected to expand by just over 11% on average each year.

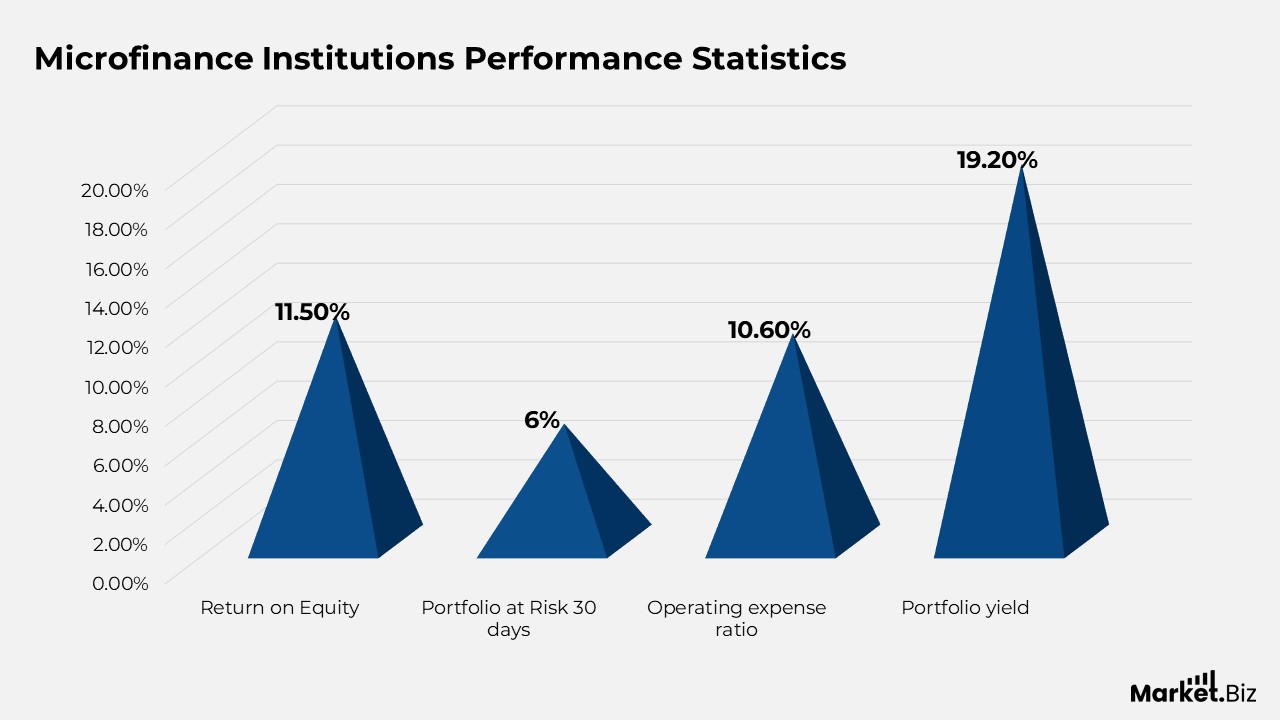

Microfinance Institutions Performance Statistics

- In 2018, approximately 139.9 million people benefited from MFI services, representing a notable increase from the 98 million borrowers recorded in 2009.

- Among these borrowers, 80% are women, and 65% come from rural regions. These figures have remained consistent over the past decade, despite the rising number of borrowers.

- In 2018, MFIs managed a credit portfolio valued at $124.1 billion, indicating another year of growth, with an 8.5% rise compared to 2017.

- Over the last 10 years, MFIs have improved their operational efficiency, even though there has been a significant rise in the cost per defaulter during this time.

- This cost increased from an average of $68.4 in 2009 to $106.7 in 2018, marking a 56% rise. Additionally, there has been a decrease of 2.7% points in the operating expense ratio.

- Moreover, between 2009 and 2018, MFIs have experienced enhancements in their returns on assets, which rose by 1.3% points, and returns on equity, which improved by 2.9% points.

- However, it is important to highlight that there has been a slight deterioration in the quality of the loan portfolio throughout this period. The portfolio at risk (PAR) for over 30 days rose from 6.4% in 2009 to 7% in 2018.

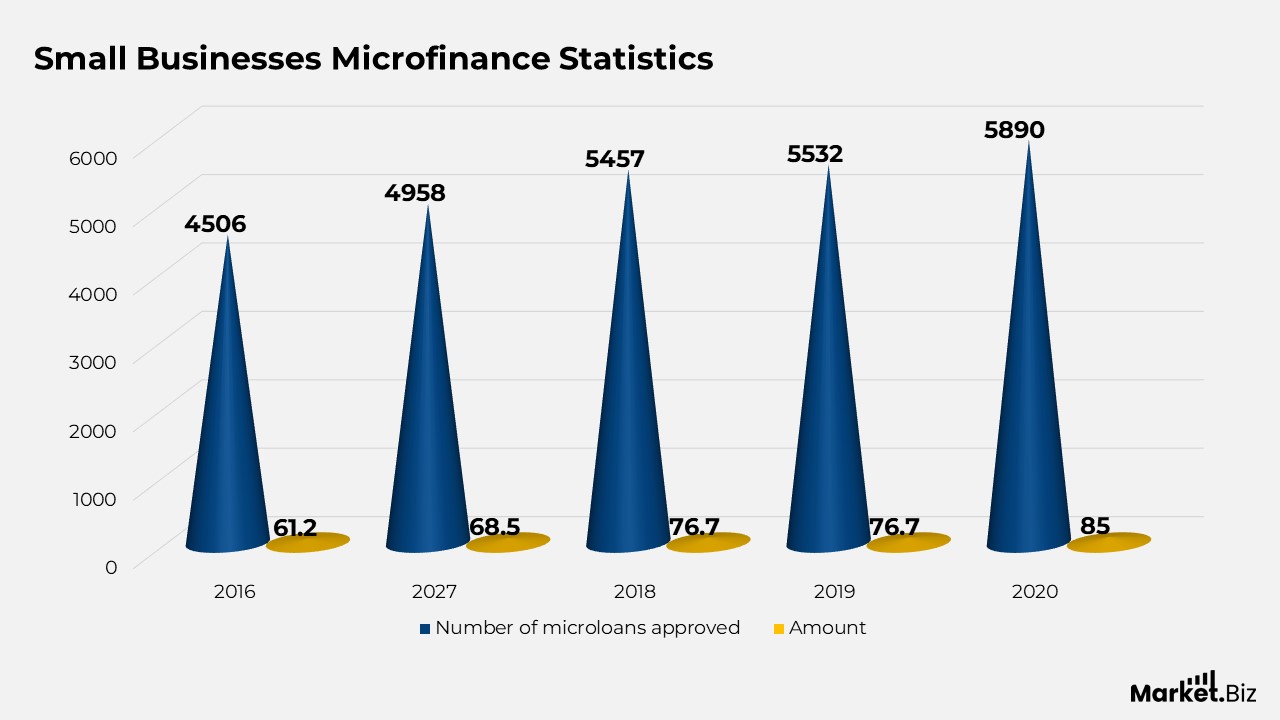

Small Businesses Microfinance Statistics

- In 2016, a total of 4,506 microloans were sanctioned, amounting to $61.2 million.

- This assistance continued to increase annually, with 4,958 microloans sanctioned in 2017, which totaled $68.5 million, and 5,457 loans in 2018, reaching a total of $76.7 million.

- The pattern continued into 2019, with 5,532 microloans approved, amounting to $76.7 million.

- By 2020, the SBA had further enhanced its initiatives, approving 5,890 microloans with a total value of $85 million.

Microfinance Demographics Statistics

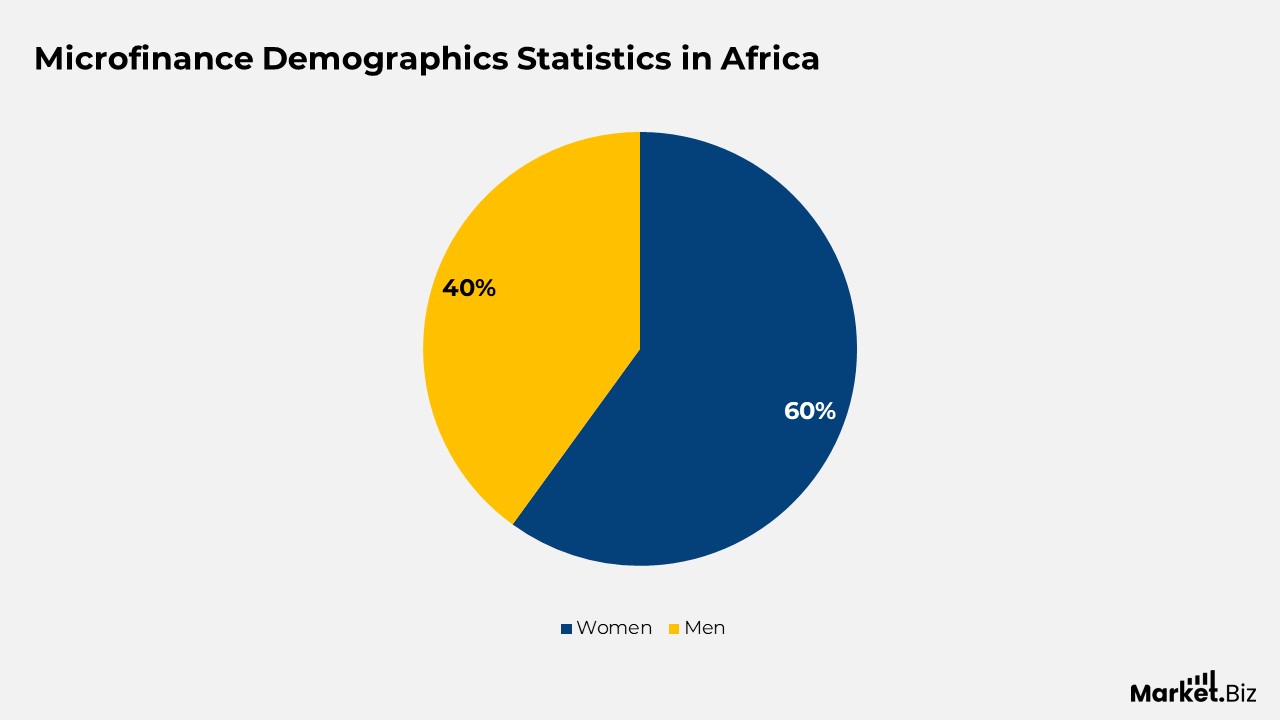

- In Africa, although women make up over 60% of the rural workforce and play a crucial role in food production, contributing as much as 80%, their access to credit remains excessively low, representing less than 10% of the total loans provided to farmers.

- Interestingly, while it may appear that women are the primary beneficiaries, studies reveal that men utilise a significant portion of the loans that women have received and repaid.

- The esteemed Grameen Bank in Bangladesh, which has been widely replicated, primarily extends credit to individuals living in extreme poverty.

- Notably, around 94% of those who qualify for the bank’s loans are women.

- Furthermore, Grameen borrowers exhibit an impressive repayment rate of about 98%. The bank allocates a substantial $30 million each month to support 1.8 million individuals experiencing severe financial difficulties.

- In a different context, nearly 46.6% of all Small Business Administration microloans approved in 2020 were allocated to businesses owned or controlled by women, which accounted for 38% of the total loan amount disbursed.

Microfinance by Country Statistics

United States

- Despite the significant global growth of microfinance, which has exceeded 140 million borrowers worldwide, its development in the United States has been relatively limited.

- Unlike developing countries such as Bangladesh or Peru, where microfinance has thrived, the United States has not witnessed a comparable rapid increase.

- A 2020 survey conducted by the Federal Reserve indicated that 7.1 million individuals, representing 5.4% of U.S. households, were classified as “unbanked,” meaning that no member of their household possessed a bank or credit union account.

- Furthermore, 13% were categorised as “underbanked,” suggesting they had bank accounts but faced challenges in accessing banking services, often turning to alternative options like payday loans.

- Almost 20% of U.S. households were identified as either unbanked or underbanked, with communities of colour and immigrant populations experiencing disproportionately higher rates.

- Significantly, over 40% of African American households and 30% of Latino households fell into these classifications, representing a considerable segment of the microfinance customer base in the nation.

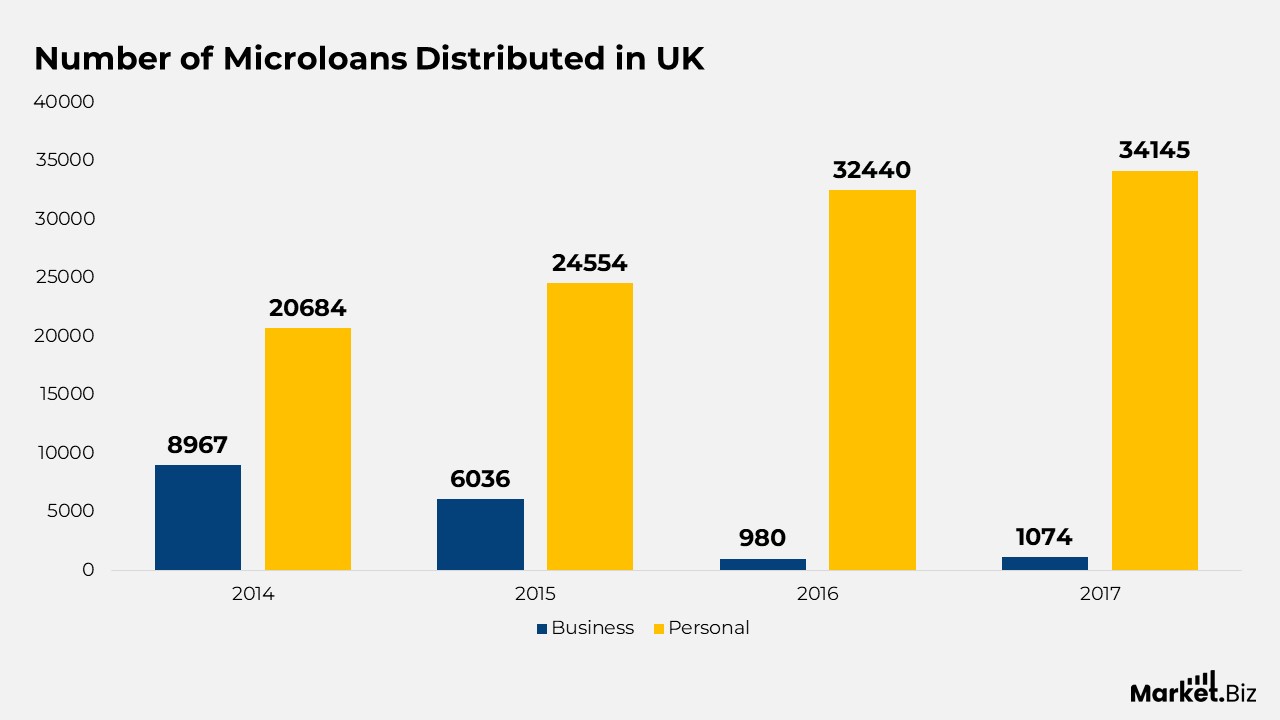

United Kingdom

- In 2014, a total of 8,967 microloans were distributed to businesses, whereas 20,684 were provided to individuals for personal purposes.

- The following year, 2015, saw a slight decrease in business-related microloans, which fell to 6,036, in contrast to an increase in personal microloans that rose to 24,554.

- Nevertheless, a notable change took place in 2016, as business microloans plummeted to 980, while personal microloans experienced a significant increase, reaching 32,440.

- By 2017, there was a slight uptick in business microloans, which rose to 1,074, alongside a continued increase in personal microloans, which reached 34,145.

China

- As of the end of March 2021, there were 6,841 micro-credit companies functioning within China.

- The total outstanding loans from these firms reached RMB865.3 billion, reflecting a reduction of RMB21.2 billion in the first quarter of that year.

- On March 31, 2021, micro-credit companies across China demonstrated a varied presence in different regions, with 6,841 institutions operating throughout the nation.

- These companies employed a workforce of 69,039 and had a total paid-in capital of RMB 78.00 billion.

- The total outstanding loans provided by these organizations amounted to RMB 86.53 billion.

- In terms of regional distribution, Beijing was home to 105 of these institutions, which had a paid-in capital of RMB 1.40 billion and outstanding loans totalling RMB 1.31 billion.

Microfinance Recent Development

- At the beginning of 2023, CreditAccess Grameen successfully acquired Madura Microfinance for a sum of $75 million.

- In late 2022, Bandhan Bank completed its acquisition of Gruh Finance for $3 billion. This merger enhances Bandhan Bank’s microfinance portfolio and broadens its housing finance capabilities.

- In 2023, Accion Microfinance secured $100 million in a funding round aimed at expanding its microfinance operations and creating new financial products for underserved communities.

Microfinance Future Predictions

- By March 2027, Garyali anticipates that the Assets Under Management (AUM) will exceed Rs 10,000 crore. He further mentioned that the existing network comprises 22 states, 1,500 microfinance branches, and 91 MSME branches.

- The Microfinance Market is expected to attain a value of $496.90 billion by the year 2030.

Conclusion

Microfinance statistics indicate that empowering women, who constitute a substantial segment of borrowers, are frequently organised into supportive groups that exhibit high repayment rates. Loans differ significantly, ranging from small amounts ($500) to larger sums, addressing various financial requirements.

The success stories of microfinance underscore its ability to change lives, promote entrepreneurship, and aid in economic development. Although challenges such as over-indebtedness persist, the sector is adapting through digital innovations and initiatives aimed at reaching marginalised communities, making it essential for policymakers and stakeholders to endorse and amplify its influence.

FAQ’s

Microfinance plays a crucial role in promoting financial inclusion by extending financial services to marginalised individuals and communities. It helps them in fulfilling their specific financial requirements, generating income, and improving their overall economic well-being.

Governments can best support microfinance development by maintaining macroeconomic stability, avoiding interest-rate caps, and refraining from unsustainable subsidised loan programs that distort the market.

MFI values integrity, fairness and honesty in all business dealings. Trust is the cornerstone of our business, and it will never be compromised. MFI values diversity and neutrality.